Cash Out Refis Making a Comeback

by Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer / February 25, 2021

Banks and consumers have a long history of having short memories. Financial mistakes made by one generation of bankers and consumers are inevitably repeated by following generations. In the housing market, we’re watching a trend that contributed to the housing crisis 15 years ago: Cash out refis are making a comeback.

What is a Cash Out Refi?

With mortgage rates dropping significantly in the last 12 months, many people have rightly taken advantage of this to refinance their mortgage. By locking in a lower rate, you can save tens of thousands of dollars in interest over the life of your loan and even shorten the term for little extra cost. It’s a win-win that frees up monthly cash flow for other purposes, such as saving for a child’s college education.

We’ve noted in previous posts how the collapse in mortgage rates has boosted home prices. Rising home prices have unfortunately offset most of the benefit from lower mortgage rates, as many current home buyers are finding out.

But for people who are refinancing a mortgage and staying in their home, the rise in home prices has opened up opportunities to “cash out” some of those gains. Here’s how it works.

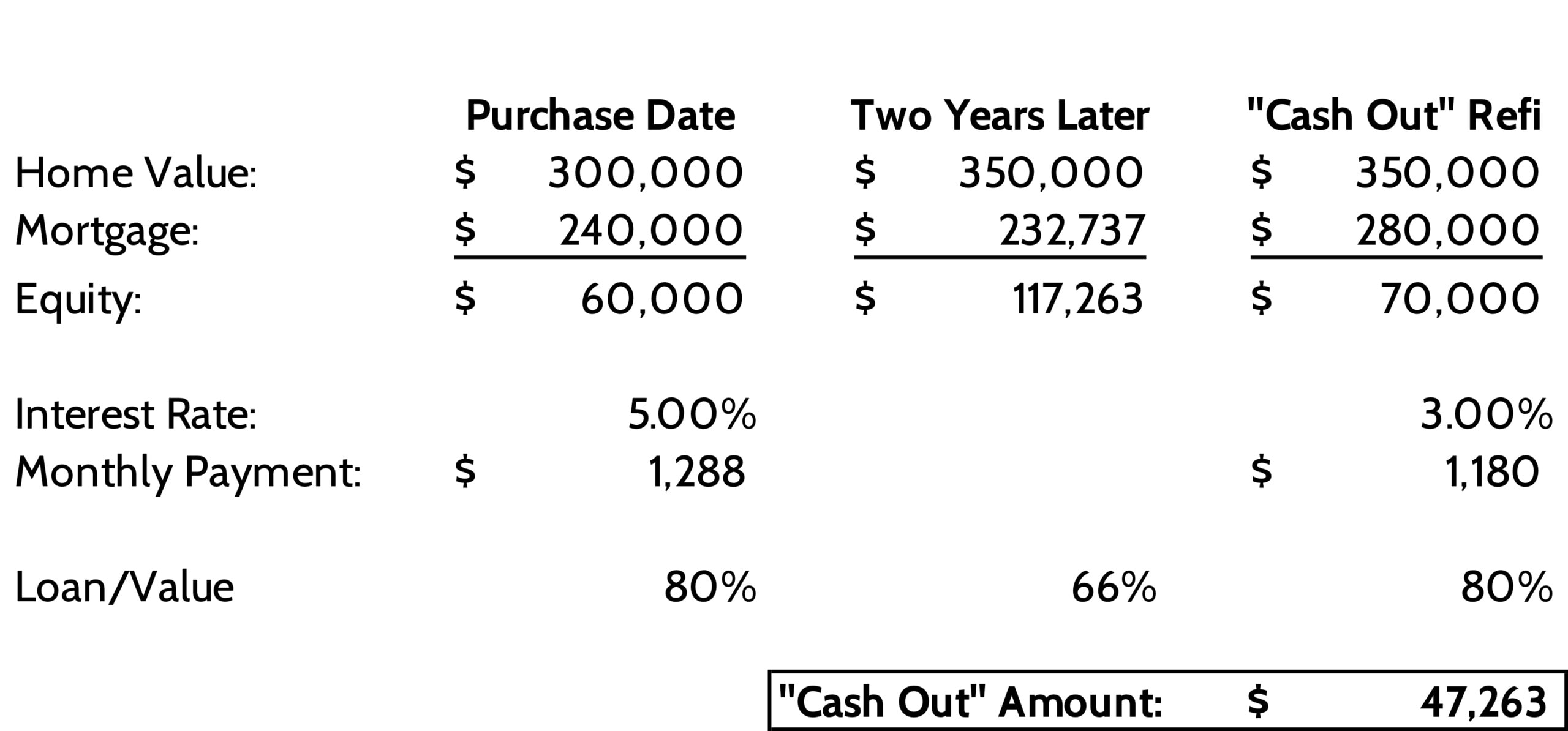

In this hypothetical example, this family bought a house and put down 20% of the purchase. Two years later mortgage rates have dropped from 5.00% to 3.00% and they’re thinking of refinancing. After speaking with their banker, they’re given two choices:

- Refinance their current mortgage balance of $232,737 into a new 30-year mortgage at 3.00%. Doing so would cut their monthly mortgage payment by $300, from $1,288/mo to just $981/mo

- Take advantage of the fact their home price has increased by $50,000 and do a cash-out refi, keeping the loan/value at 80% and receiving the difference of $47,263 in cash

We’re all human and when presented with an opportunity to get a sizeable chunk of cash, most of us are gonna take it. This family was still able to reduce their monthly mortgage payment by $100, and they get cash to boot! What’s not to like?!?

Is the Comeback in Cash Out Refis a Sign of a Housing Bubble?

Cash-out refis are a relatively recent phenomenon in the world of personal finance. They became quite popular starting in the late 1990s and early 2000s as home prices rose and mortgage rates dropped.

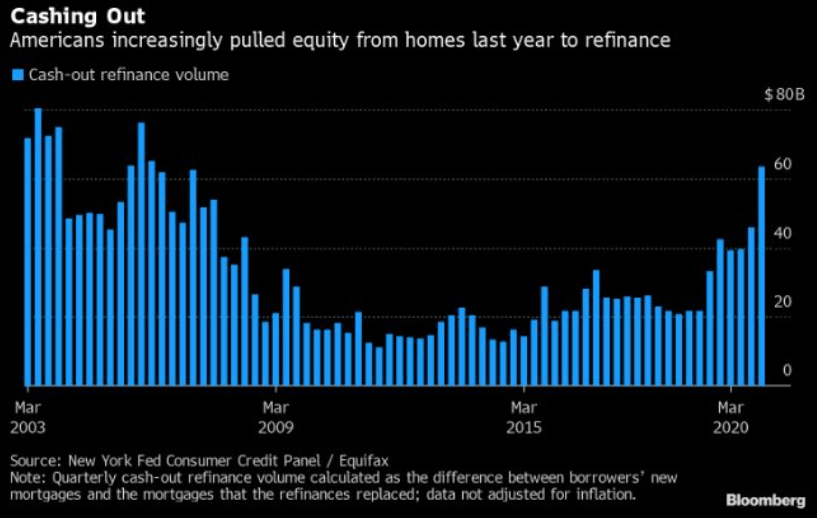

There isn’t a lot of long-term data on the total size of cash-out refis in the U.S., but the New York Federal Reserve and Equifax have attempted to quantify this in the chart below:

Cash-out refis were very popular in the wake of the Fed’s move to slash interest rates in response to the tech bubble and 9/11. At the time, the universal belief with consumers and banks was that nationwide home prices never went down.

As mortgage rates dropped to historic lows and home prices rose further, mortgage lenders offered a great deal to consumers: “You can cut your mortgage payment by refinancing at a lower rate, and cash out some of your home price gains at the same time!” Consumers took the bait. It became such a popular thing to do that many people treated their rising home values as an ATM to draw on whenever they had the urge to spend.

Most of us who lived through that bubble know what happened: it crashed. Home prices dropped in 2007 and we had the deepest home price recession since the Great Depression: exactly what every expert assumed couldn’t happen.

The problem for consumers that took out cash-out refis is they now held much larger mortgage balances on a home worth much less. At its worst point, 1 in 4 Americans were “underwater” on their mortgages. Meaning, they owed more than their home was worth. People walked away, foreclosures skyrocketed, as did personal bankruptcies.

Should I Pay Down the Mortgage or Invest The Rest?

One of the biggest debates in personal finance is this: “Is it better to pay down your mortgage and become debt free, or take out a mortgage at low interest rates and invest the rest at higher returns?” Mathematically, borrowing at 3% and earning 7-8% is going to make sense. The problem is that “tail” events like the Tech Bubble or 9/11 or the Housing Bubble blow this math up in a hurry.

And this is the point we always make with people. You can do this and it might work 99.9% of the time, but if that 0.1% tail event hits, you can find yourself wiped out. Think about Auto & Home insurance. It makes mathematical sense NOT to buy insurance because the reality is most of us will never have a big enough claim to offset the premiums we’ve paid. But we do it because we can’t stand the thought of being uninsured in the event our house burned down.

From 2000 to 2006, banks and consumers had an unshakable faith that home prices would never go down until they did in 2007-2009. “Unprecedented,” they said. But life is full of unpredictable events, and if you’re living on the financial edge, it’s just a matter of time until the “tail” wags wide enough to hit you.

As we saw with our hypothetical family above, they prudently paid on their mortgage for two years, reducing the amount they owed by over $7,000. But then they did a cash-out refi and found themselves with $40,000 MORE in debt. In other words, they increased their financial risk in the one asset they’d hate to lose if something went wrong: their home. Running hard, but not getting ahead.

Cash Out Refis a Sign That Consumers Are Taking on More Risk

It’s with this backdrop that we’re concerned with what we see in the above chart. Consumers and banks are back at the same game, tapping their home equity. Obviously, everyone’s situation is unique and there can be logical reasons to do a cash-out refi. But taken as a whole, the increasing popularity of cash-out refis should be a warning sign that the housing market is once again getting frothy, which is amazing given we’re just a dozen years removed from a horrible housing bust that scarred many people.

I’ve been writing a lot about signs of bubbles we’re seeing in the stock market, but we’re now seeing signs of this spreading to consumer behavior. As I noted in this month’s newsletter about investing, a “tortoise” approach to investing your money might be boring, but it allows you to ride out those tail events without getting wiped out.

We’re already through the first two months of 2021 – time flies by quickly! When are you scheduled to get your mortgage paid off? Before retirement? In your 70s? Ever?? Getting your mortgage paid off before retirement is usually a good idea, so you’re not burdened by making debt payments on a fixed income.

Keep this question in mind if you go to refinance and your mortgage banker waves a wad of “cash-out refi” cash in front of you. The joy of a short-term spending spree might come back to bite you if a “tail” event happens in the future!

Ready to take the next step?

Schedule a quick call with our financial advisors.