Life Insurance Video Series

by Michelle Smalenberger, CFP® / June 28, 2017MICHELLE SMALENBERGER, CFP®

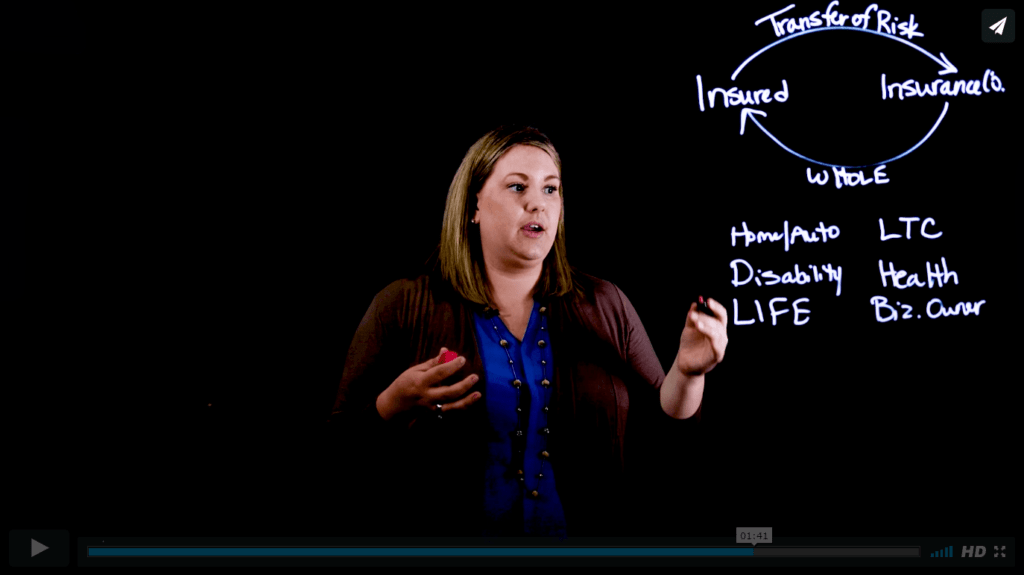

I’d like to talk about one area of financial planning that seems to be misunderstood. Or maybe there’s just a lack of knowledge about this topic, and that’s insurance. When you’re considering getting any type of insurance, you the insured are looking to transfer the risk to someone else. So really what’s happening here is that there is a transfer of risk that you’re saying you don’t want to take on, but when something happens you want to be sure that you are going to be made whole.

With different types of insurance, and in most cases, you are made whole. Let’s just talk about a few. For home and auto, we have a home and we have a car, and we need to be able to function. So, the goal of this is to be able to continue using those things.

With different types of insurance, and in most cases, you are made whole. Let’s just talk about a few. For home and auto, we have a home and we have a car, and we need to be able to function. So, the goal of this is to be able to continue using those things.

Disability is one type of insurance that actually doesn’t make you whole. Typically, you can get insurance up to 60% of your income, which is going to fill most of your needs. However, it’s not 100% so it’s not making you completely whole.

Another is life insurance, and we’ll talk through that. Some others might be long term care. When you can’t do two activities of daily living that you normally do, now you need help. You need some type of insurance to help supplement that. But again, it’s not meant to completely cover you. Others that we think of commonly are health insurance, or maybe a business owner insurance.

So, these are just the types of insurance. Typically when you think of getting them you’re really trying to transfer the risk from yourself so that if you have a loss, you’re going to be made whole and you’re going to be able to function, because you have insurance to cover these times where you do have a loss.

One area of insurance that I think is hard to define a value for is life insurance. So, I really want to dig into that a little bit to help you come up with or to make a little simpler that process of what is the amount of life insurance that I need? When we contrast this with a home or an auto insurance, it’s really easy to find a willing buyer who wants to buy those things, and so there’s a price that they’re willing to pay you. That really sets a value of what we need to be insuring that property for.

The life insurance is very different because this is really dependent on you, on someone else, on who is surviving you, so it’s really looking forward and saying what do I want to make sure is taken care of? When we just look at life insurance in general, there are some common ways that people typically look at this, and these are just really simple calculations.

For example, one may just be income replacement. Where we’re really just looking at your salary, today, times the number of years that we know you need to work to fill those goals, or fulfill everything you’re wanting to do for your family. Second, is an acronym D.I.M.E. So really wanting to make sure we’re covering our debt, our income, a mortgage, or education if you have children. These are some simple ways we could start with.

One third way that I want to suggest to you, is really looking at what are your goals. We’re going to dig into this a little more. And the nice thing about this is this really becomes a discussion between you and your financial advisor, or an insurance agent so you feel like you’re a part of coming up with how much insurance you need instead of someone else saying this is the amount you need and now having this shock of not knowing where that number came from, or feeling like it’s unreasonable.

So, let’s talk through what some of these goals might be to get us to the value of life insurance we both feel like we might need. For example, we’re of course going to need some of the things that are used in some of these other equations. So basically, income loss. It is really important that if there is a loss of income from one of the spouses that we’re replacing that. And one note on this that I really want to stress is even if there’s a spouse who stays home with your children, or really helps to keep the household in order, it’s really important to have life insurance for that individual. Because the cost of replacing that person, the childcare, cleaning, things like this, that person is really supporting the ability for the other people in the household to go to school and work. So, it’s really important to consider both people who are supporting the household and the income that is coming in. We don’t want to forget about that.

Of course, the next is debt, whether that’s a mortgage, auto, or maybe a student loan. And then we start to get into some goals that may not have been defined in some of these others formulas, like maybe a wedding. You want to be sure to support your kids if you know or think there’s going to be a wedding in the future.

Some others that we may typically not think of, are if your estate is large enough, you may actually have estate taxes, whether that’s federal or state. And you want your beneficiaries to actually receive those assets, you don’t necessarily want them to have to pay taxes first and then get what is left.

And then lastly is inheritance. For example, if you don’t want to worry about spending all your assets down, but you want to ensure that your beneficiaries are going to receive a set amount after you pass away, you can use life insurance to make sure that that happens.

I hope this is helpful to really just come up with another way to look at and solve for the amount of life insurance that you need, but also to include you in that conversation so you feel like you’re a part of coming up with the value you need, instead of just getting a number from someone and you don’t know how it’s made up.

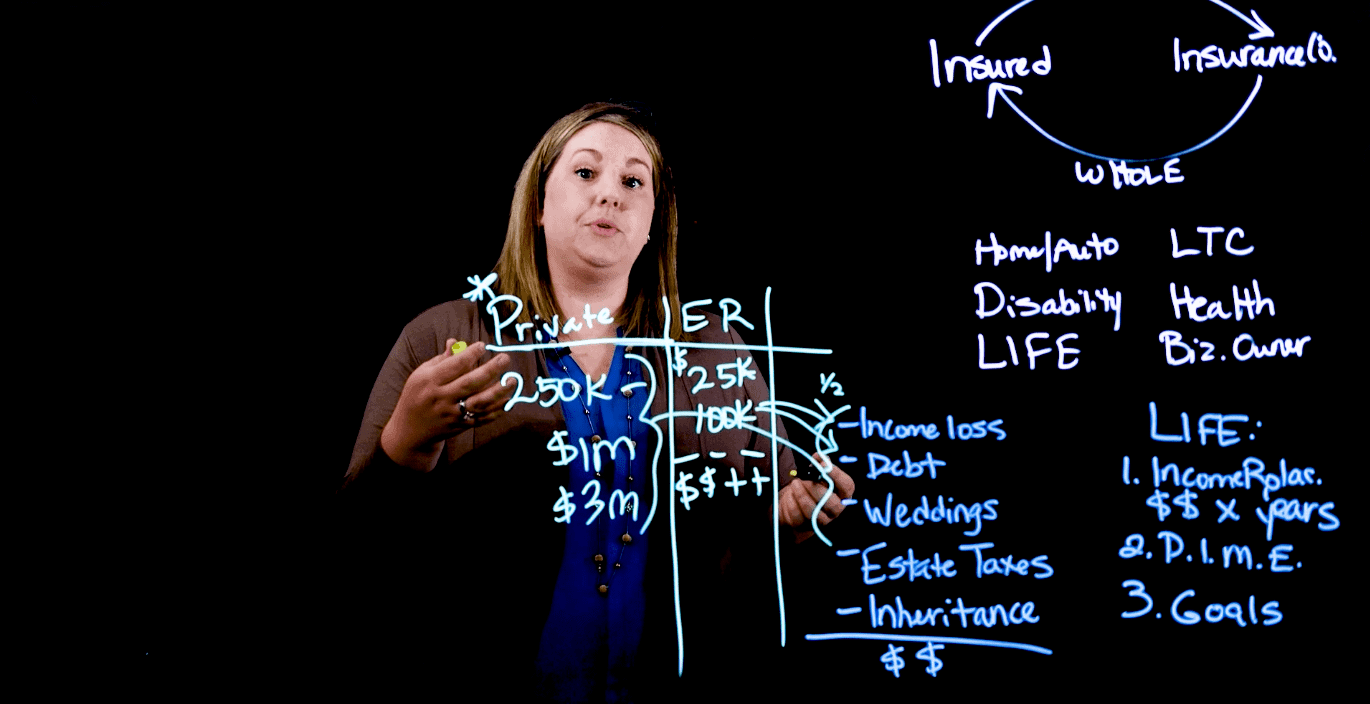

So now that we know the amount of life insurance that we agree that we need, we really want to look to where the sources of that insurance are going to be. It’s very common that someone who works for an employer or for a company may get a benefit that’s just standard. you may get 25 or 50 thousand, maybe a 100 thousand of life insurance. and so now you at least have some base benefit that maybe you’re paying something for, or you may also have the ability to buy more. So, the nice thing about getting insurance through your employer is typically you can get it at a discounted rate. It’s a larger group policy so maybe there’s some type of discount so it’s a little cheaper than otherwise.

But what I also want to suggest to you is to consider getting a private insurance policy. And really what this means is that you’re going to go out and get a life insurance policy for yourself. And the reason that you would want to do this is because when you are working for your employer, you have this insurance. But if you leave that employer, now you have nothing if you don’t have any private insurance. Or you’re dependent on the next company when you get that job to have insurance and the amount that you need that we’ve already decided we need.

So, with a private insurance policy, we may be looking at getting more like 250 thousand in insurance, maybe up to a million, maybe even 3 million. This is really dependent on what we’ve said are our goals, and what we want to cover. The difference between these two is if I only have my employer provided insurance, maybe now I can only cover a portion of that income loss, maybe I can only cover one of those debts that I have. So, by adding this additional layer of private insurance, we’re really saying that between all of this, now I can cover a variety, or a larger amount of these needs and the goals that I am trying to reach.

So, with a private insurance policy, we may be looking at getting more like 250 thousand in insurance, maybe up to a million, maybe even 3 million. This is really dependent on what we’ve said are our goals, and what we want to cover. The difference between these two is if I only have my employer provided insurance, maybe now I can only cover a portion of that income loss, maybe I can only cover one of those debts that I have. So, by adding this additional layer of private insurance, we’re really saying that between all of this, now I can cover a variety, or a larger amount of these needs and the goals that I am trying to reach.

So, I want to encourage you to go back and look at the amount of life insurance that you currently have, and where you have that insurance. If it’s through your employer, can you get more? Do you have a private insurance policy? Maybe consider adding this in case you do think that you may switch jobs in the next 5-10 years, or you may be doing more than what you are currently doing at your employer. This just gives you flexibility, but also you won’t be without insurance in case something happens, and that’s really what we’re trying to make sure we have in place.

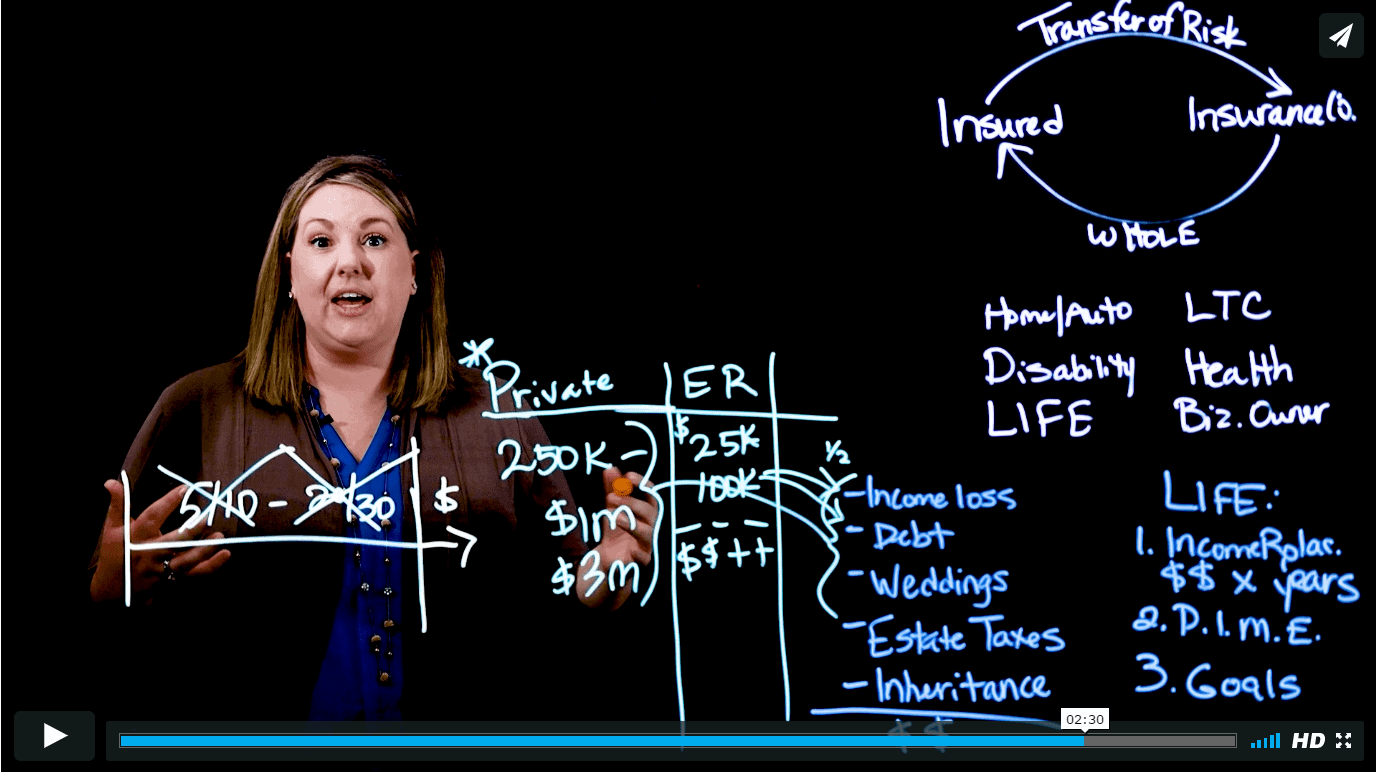

The last part I really want to talk you through is the term, or how long we typically have life insurance. When you’re buying a policy, especially maybe this private policy, it may be that you have it for 5 to 10 years, or 20 to 30 years. And really, the purpose of life insurance is to insure the income that we’re planning to earn until we retire, to be able to save money so that when we’re at retirement, really when we match it up to when we’re assuming we’re going to retire after this, we already have the money that we need.

So now when this policy expires, this can go away. We don’t really need it anymore, because now I have the money I need to be able to fulfill all of those needs or goals in retirement. Maybe your mortgage is paid off, your student loans, your auto loans that you may have had 20-30 years ago are done. Your children are grown, maybe they’ve already had weddings, maybe not. But these are some of the things that now you’re saying I’m able to self-insure for the cost, or other things that may come up.

I really want you to think about some of the times that life insurance becomes important, is really before something happens. So, if you’re having a child, if you know you’re going to be having a child coming up, it’s really important to think through. Okay, now that I have someone else I need to support in my family, I need to be adding more insurance to what I have now for myself and my spouse. So, it’s things like that. Am I buying a house? Am I going to be buying a business, or starting a business? These are times, changes in our lives, where we need to be changing or adjusting this amount of life insurance, or at least reviewing to see if we need to be changing it.

I really want you to think about some of the times that life insurance becomes important, is really before something happens. So, if you’re having a child, if you know you’re going to be having a child coming up, it’s really important to think through. Okay, now that I have someone else I need to support in my family, I need to be adding more insurance to what I have now for myself and my spouse. So, it’s things like that. Am I buying a house? Am I going to be buying a business, or starting a business? These are times, changes in our lives, where we need to be changing or adjusting this amount of life insurance, or at least reviewing to see if we need to be changing it.

So, I really want you to be thoughtful of the life insurance that you have, go back and review, see if changes need made. But I also want to just explain one of the ways that when you have these things in place, it really allows you to live life in a different way. When you have life insurance set in place, when you have the proper amount, it allows you to live in such a way that you don’t have to worry if something happened to you. You don’t have to worry that your family wouldn’t be taken care of, that anyone surviving you wouldn’t be supported. So, I really want you to understand that having things in place, it allows you to live life differently. This is really the goal of planning ahead and really having these conversions now. Even though we don’t enjoy them, or if it’s a topic you may not want to talk about, this is the goal of really talking through and planning these things ahead of time.

Don’t have 10 Minutes? Watch the Series in Short Sections:

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

Getting the Right Life Insurance Coverage [Video]

Watch this video to learn more about the ways you can use your life insurance coverage, no matter what life stage you are in.

Insurance Webinar

Our insurance webinar walks you through the basic insurance policies, what you may be missing, and an audience Q&A session.

Michelle Smalenberger, CFP®

I have a passion for helping others develop a path to financial success! Through different lenses on your financial picture, I want to help create solutions with you that are thoughtful of today and the future. I have seen in my life the power of having a financial plan while making slight changes of direction from time to time. I believe you can experience freedom from anxiety and even excitement when you know your finances are on track.