Third Round of Stimulus Checks

by Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer / March 11, 2021

“Hey Daddy, am I going to get a stimmy this time?” It’s a question that any parent of a Gen Z college student is asking. “What’s a stimmy,” you might ask? It’s Gen Z’s slang for a stimulus check. Yet another round of COVID pandemic relief is coming. This bill is the third round of stimulus checks to go out to consumers and also includes other items. How will consumers use their stimmy this time around?

What’s in the March 2021 Stimulus Bill?

Like previous relief bills, there are several support programs included. Here’s a short list of the key provisions that affect most families.

- Stimulus checks: $1,400 per taxpayer and any dependents claimed on their tax return. For example, a family with a middle school child and another child who’s in college will get $5,600 ($1,400 x 4) if they claim both children as dependents. Taxpayers who claim older parents as dependents will also get a payment for them.

- Child Tax Credit: They have expanded these tax credits to $3,600 for each child Age 5 & under and $3,000 for children Age 17 & under. These credits are fully refundable and can even be paid in advance, starting in July under certain conditions.

- Unemployment Assistance: Self-employed workers can continue to file for unemployment through September 6, 2021. The $300 per week Federal Pandemic Unemployment boost is also extended to the same date.

- Taxability of Unemployment Received in 2020: Normally you pay income taxes on unemployment checks you receive. But this bill makes up to $10,200 of unemployment benefits received in 2020 tax-free. If you already filed your 2020 taxes and received unemployment benefits, you’ll have to re-file your 2020 taxes to get this benefit.

- Student Loans: Any borrowers who have Federal or Private Student loans forgiven from 2021 to 2025 will NOT have to pay taxes on the amount that was forgiven. Normally, you’re taxed on any discharged debts, but that won’t be the case for student loan borrowers who have debt forgiven during those years.

There are a lot of income phase-outs that apply to the above benefits. And in Congress’ wisdom, these phase-outs are different depending on the benefit! We won’t go into all of them but want to focus on the phase-outs for stimulus checks.

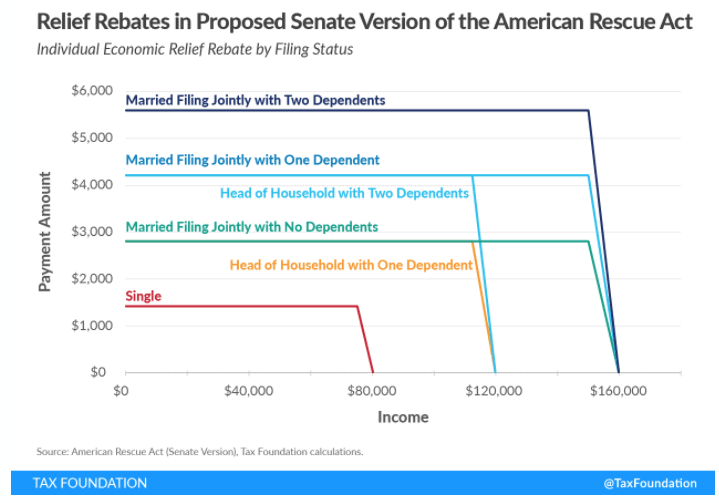

What’s the Income Phaseout for Stimulus Checks?

The original stimulus checks issued in Spring 2020 had wide income phase-outs. For example, if you were a single filer, you received a full stimulus check as long as you earned less than $75,000. But they allowed you to get a reduced stimulus check up to $100,000 of income.

The March 2021 bill has much narrower income phase-outs. This may lead to a situation where a small increase in your taxable income phases you out of getting a stimulus check completely!

In this version of the stimulus bill, that same single filer gets a full stimulus check up to $75,000 of income. But if they make just $5,001 more, they get nothing!

Married couples can get full stimulus checks for themselves and their dependents as long as their income is $150,000 or below. But if their income is just $10,001 higher, they get no checks at all.

This makes tax planning important. The IRS is going to look at the last tax return you filed to determine your income for these phase-outs. For most folks that would be their 2019 return, before the negative impact of the pandemic hit their wallets. If your 2020 income was less than 2019, then you can either hurry and file your 2020 taxes before they send checks out, or ask the IRS to send you a check after you file your 2020 taxes.

The procedures for this aren’t 100% clear given that the bill isn’t even officially law yet. But that’s close to how it’ll probably work.

How are Consumers Going to Use Their Third Round of Stimulus Checks?

Stimulus checks are being issued in the belief that Americans continue to suffer from the pandemic. Certainly, those that work in travel and entertainment have indeed suffered a lot from states and businesses being closed down.

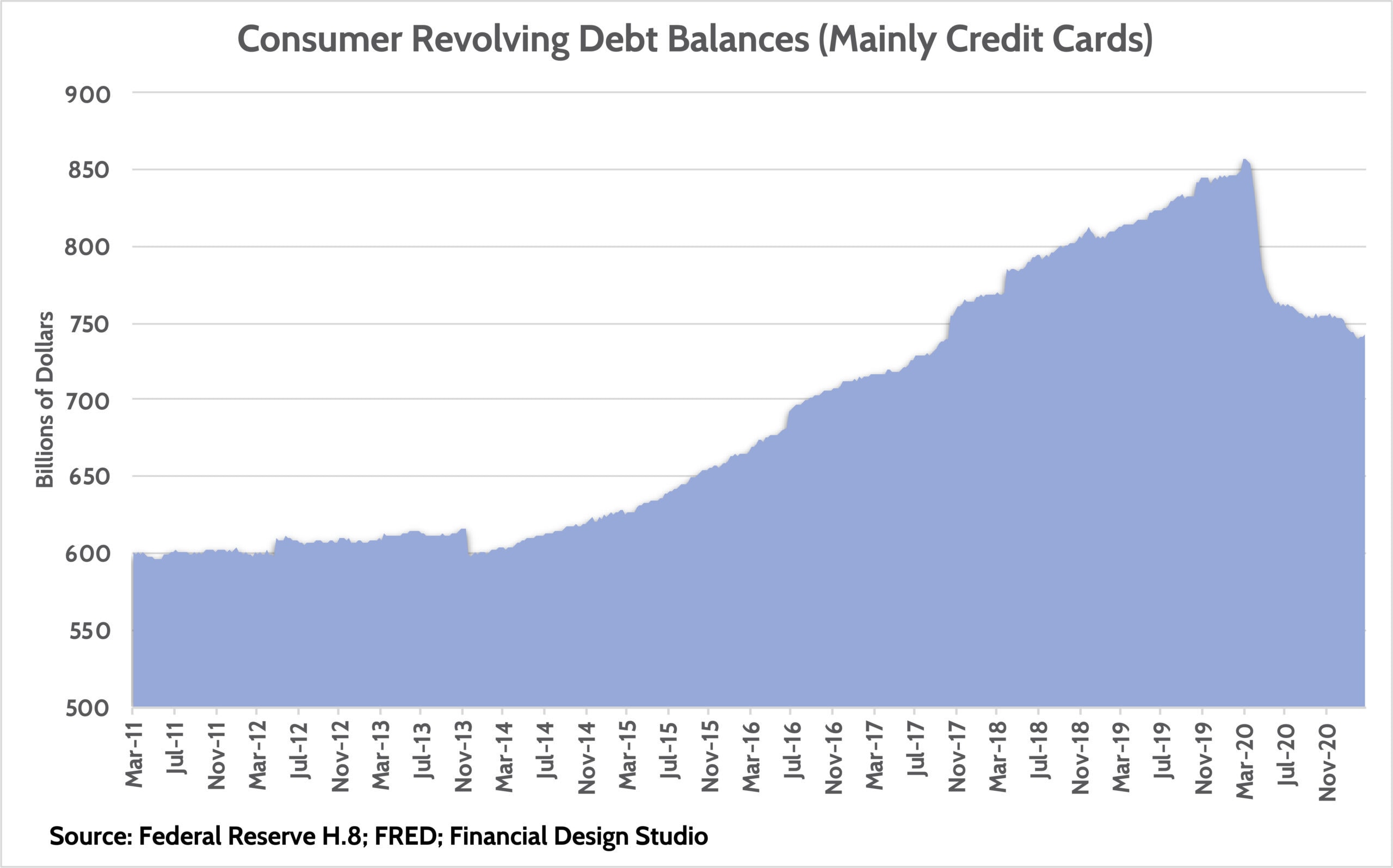

When the first round of checks was issued last Spring, consumers used about 1/3 of the money to pay down debt. This led to a $110 billion decrease in the amount of credit card debt outstanding.

We assume many consumers will continue to use stimulus checks to reduce debt. But with vaccines being rolled out and states reopening their economies, it’s quite possible we’ll see a surge in consumer spending as well.

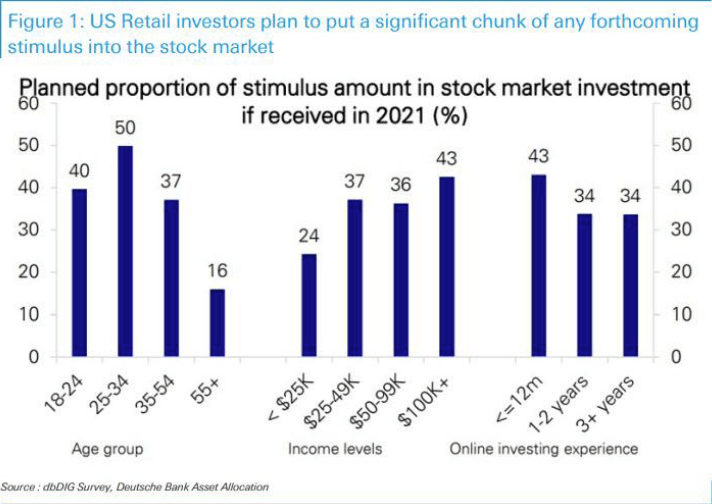

Interestingly, the German investment bank, Deutsche Bank, conducted a survey of consumers to see how they expect to use their upcoming stimulus checks. Surprisingly, about one-third of consumers say they’ll invest their checks in the stock market. For Gen Z and Millennials, nearly 50% are going to put their “stimmy” in the stock market!

We recently wrote about how a frenzy in the stock of Gamestop was a sign of bubble behavior by retail investors. That so many people are talking about gambling their stimulus checks in the stock market is yet another feather in the “bubble” cap.

Other Ways to Use Your Stimulus Checks

Given that we’ve all been locked in our homes for a year, splurging on a vacation or additional home improvement projects isn’t a bad way to use your stimulus checks. But before you click that “Buy” button online, here are some other ideas for how to use it.

- Are you behind on retirement savings? Maybe put that check in a Traditional or Roth IRA to get the ball rolling.

- Do you have kids going to college at some point? Funding a 529 college savings plan would be a great way to cover what will be a big expense when they turn 18.

- Give it away. Many non-profits have suffered major funding shortfalls because of the pandemic. Giving some portion of your stimulus checks to these organizations can really help them out.

Regardless of how you use your checks, it’s important to think ahead. With hundreds of thousands of people getting vaccinated each day, the pandemic is going to be over before we know it. That means this might be the last “pandemic relief” bill we see. Whether you’ve needed these three rounds of stimulus checks or not, the party is going to quickly come to an end. Be thoughtful with this last round of checks coming our way as it may be our last!

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

How Will AI Affect the Jobs Market?

White collar workers are wondering how AI will affect the jobs market, and their career. This article shares what's noise and what's real.

Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer

Rob has over 20 years of experience in the financial services industry. Prior to joining Financial Design Studio in Deer Park, he spent nearly 20 years as an investment analyst serving large institutional clients, such as pension funds and endowments. He had also started his own financial planning firm in Barrington which was eventually merged into FDS.