Investors Are Piling Into Stocks at a Record Pace

by Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer / July 8, 2021

The first half of 2021 is over (already!?!?) and data about investor activity is coming in. Of all the charts and graphs we’ve seen in the past week, the ones sticking out the most deal with how investors are piling into stocks at a record pace. If there were any doubts that investors’ fears about COVID are gone, these charts should erase them!

From Net Sellers of Stocks to Net Buyers

The last decade has seen a major demographic shift. Baby Boomers are reaching their retirement years and are using some of the retirement savings they had stashed away. Others are shifting their stock & bond allocations from aggressive strategies to more conservative ones to preserve what they’ve saved. All of this has led to net selling of stocks in recent years.

It seems odd that investors have been net sellers of stocks during one of the biggest bull markets in history. But as we always remind clients, “Some day you’re actually going to use/spend your retirement savings.” That’s what appears to be happening today.

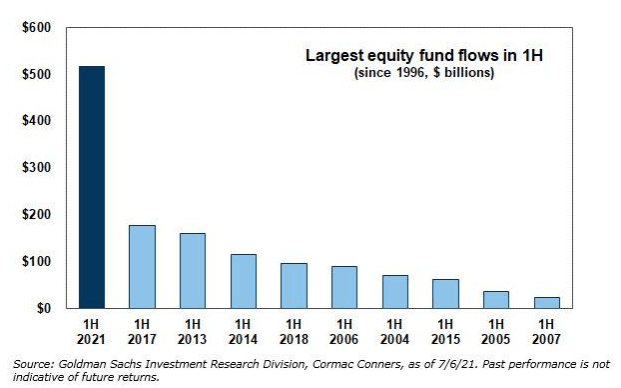

Record Stock Buying in First Half of 2021

With these demographics as a backdrop, it’s even more surprising to see what’s happened in the first half of 2021. Investors poured more money into stocks – by two-and-a-half times! – than any year in the last 25 years.

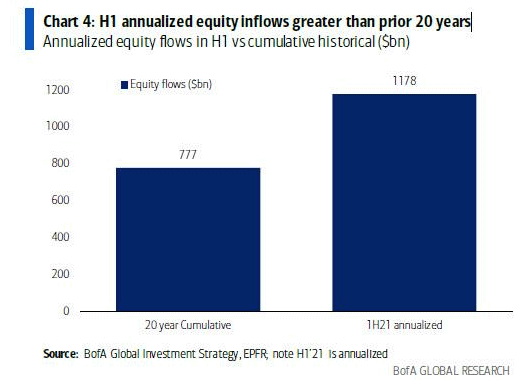

To put the scale of these inflows into context, Bank of America published a chart looking at these flows (annualized) compared to what’s come into the stock market over the last 20 years. While it’s unlikely the pace recent inflows will continue, what’s happened in early 2021 is remarkable.

Where is all this money coming from? There’s a passionate debate in the industry. Clearly, some of this money is coming from the three rounds of stimulus checks that were sent to consumers. After paying down debt with these checks last Spring, more people have been investing the December and March stimulus checks.

Another reason for these record inflows is that the Federal Reserve continues to flood the financial system with money. Despite rapid improvement in the economy, they’re still buying $120 billion of government and mortgage bonds per month. Plus, record low interest rates has encouraged investors to take out leverage to buy stocks, as we’ve noted recently.

Are Investors Getting Too Aggressive in Stocks?

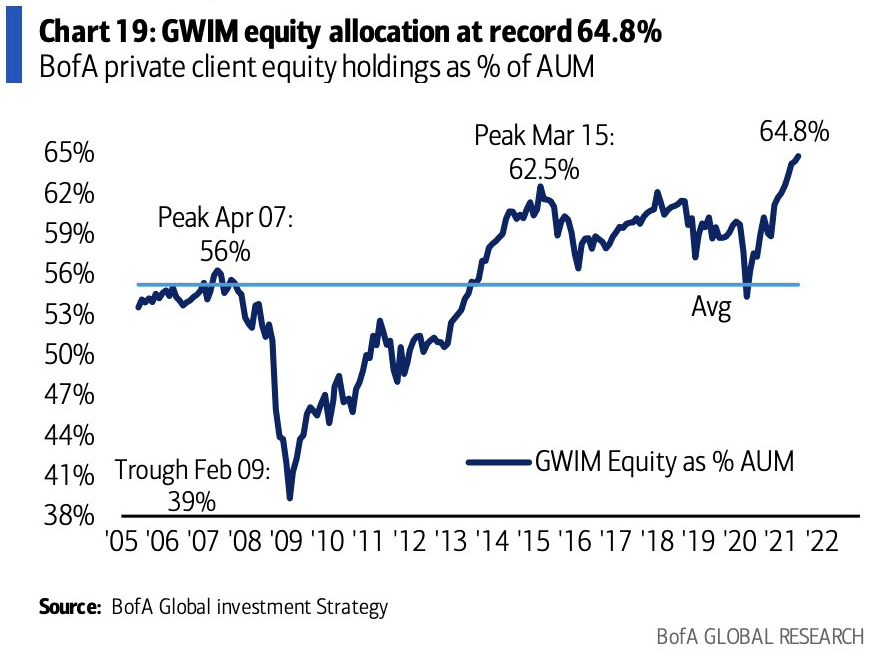

One of the most interesting charts we’ve seen of late is from Bank of America’s private client group. Here, they take a historical look at how much of their client’s assets were invested in stocks.

For these clients, there’s clearly been a big shift into stocks in the last 12 months. Some of this is because of the recovery in the stock market, but the rest of the gains would be driven by additional money being put to work in the stock market. To us, this is a yellow flag that investors may get too confident in stocks continuing to go up.

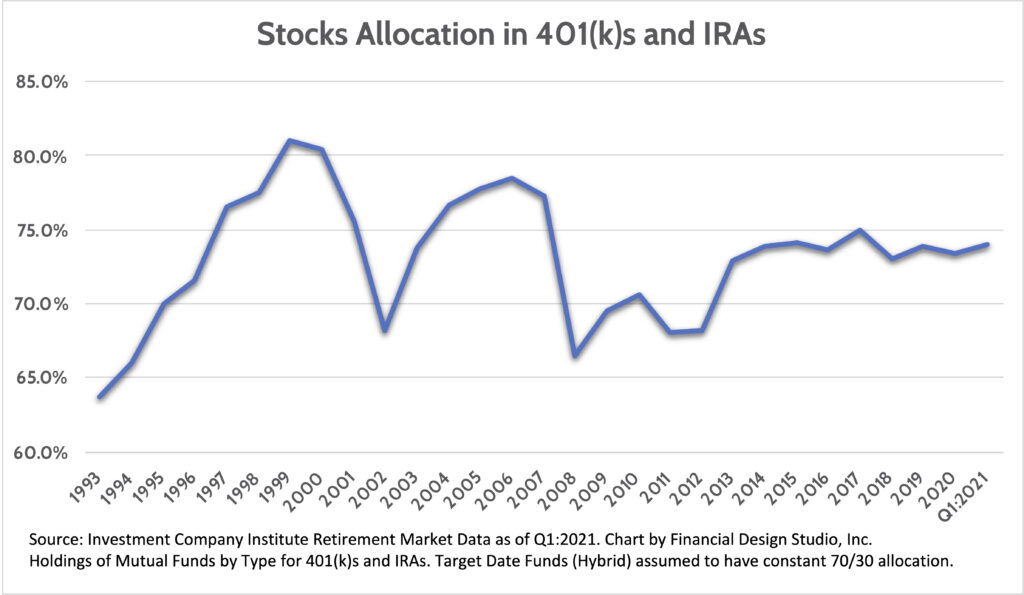

The good news is that this behavior is not translating into more aggressive behavior with people’s retirement assets. The chart below looks at the percentage of retirement assets currently in stocks, which is holding steady at 74%.

It’s noteworthy that Baby Boomer assets make up a disproportionate of retirement assets. Our interpretation of this chart is that Baby Boomers are wary of chasing stocks. They were burned chasing stocks in the 90s Tech Bubble, and again in the Housing Bubble of 2005-2006. No reason to make the same mistake a third time.

So what causes the disconnect between the BofA chart and this one? It’s likely that a class of newer, younger investors have started investing in the last year. We’ve previously written about the surge in activity in penny stocks, which is classic late-cycle behavior by investors. Our fear is that these younger investors are going to learn the same, hard lessons their parents did in the 90s and mid-2000s.

Resist the Urge to Chase Stocks and Stick to Your Plan

We’ve been impressed with the resiliency of our clients sticking to their plans over the last 18 months. There was little sign of panic as the market gave up over 30% at the onset of the COVID crisis. And so far, there’s scant evidence of people getting caught up in the current stock market frenzy.

When we work with clients, we’re careful to come up with the right investment allocation at the outset of the relationship. This allocation between stocks and bonds helps people reach their long-term goals within their own tolerance for risk.

As markets go through bull markets and bear markets, we’re there to remind clients to stick to their plans. This means rebalancing their portfolios when their allocation moves too far away from their target mix.

Sometimes this rebalancing process can be hard for investors to stomach. Last Spring, when stocks were collapsing, we were rebalancing clients back to target by buying stocks. It takes a lot of intestinal fortitude to be buying stocks when it seems like the world is ending, as it appeared in the early days of COVID.

It’s just as hard to rebalance when the stock market is rallying to new highs, selling stocks into these rallies. The temptation to stay at the party can overwhelm many investors. But as we saw in 1999 and 2006, the party doesn’t last forever, even if it seems like it will.

What We Do for You

Our job as your advisor is to keep you focused on your plan and long-term goals, and to coach you through these occasional periods of fear and greed. In fact, it’s times like this when our advice becomes more valuable.

If we can help you avoid selling at the bottom (fear) or piling into stocks at the top (greed), then we’re saving you a lot of regret later. Making a mistake at the top or bottom of markets can cause lasting damage to your long-term goals.

Are you in need of that kind of advice and coaching? You’ve done the hard work of diligently stashing money away for retirement. Protecting those savings by working with someone like Financial Design Studio might be the best investment you can make.

Ready to take the next step?

Schedule a quick call with our financial advisors.