Federal Reserve is Boxing Itself Into a Corner

by Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer / June 17, 2021

Eight times a year the Federal Reserve holds a meeting to determine current monetary policy. These events are always a big deal for markets, but some meetings take on greater importance for investors. The meeting this week was one of those “big” meetings given the recent rise in inflation. While there was no major change in policy for right now, we believe the Federal Reserve’s Policy is boxing them into a corner by signaling future rate hikes starting in 2023.

Summary of This Week’s Fed Decision

Since the onset of the COVID crisis, the Fed has been clear that they’ll be very slow in raising interest rates again. They want to allow the economy to fully recover, even if that means hotter inflation over the medium-term.

With that in mind, it wasn’t a surprise to see the Fed stand pat, leaving interest rates where they are near 0%. Nor did they reduce how much government and mortgage securities they’ve been buying. This is currently running at $120 billion a month.

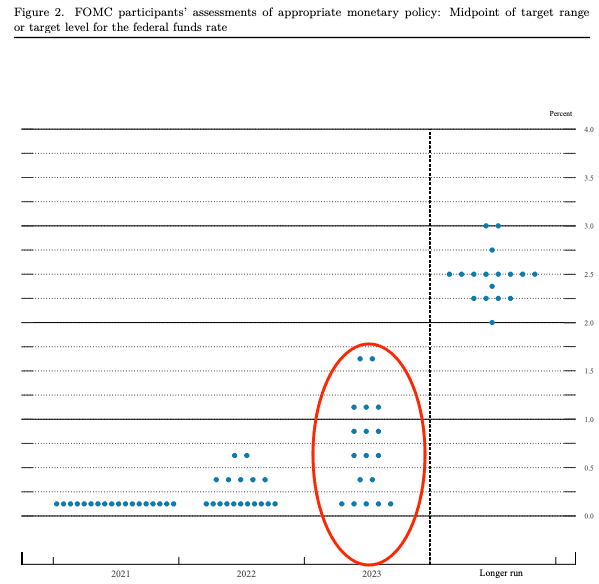

But there was one important shift. Every other meeting the Fed publishes how each Federal Reserve Board member expects future monetary policy to play out. This is known as the “Fed dot plot” for a reason that becomes obvious as you look at the chart below.

Here’s how to read the dot plot. Each “dot” is where each of the Fed members expects interest rates to be by the end of each year. For 2021, you can see all the dots are flat near 0%, which is the current policy. No change expected there.

For 2022, seven members (dots) expect one or two interest rate hikes, but it’s 2023 that drew investors’ attention. There are now 13 Fed members expecting higher rates by 2023. This is double the number of members expecting that to happen since their last update in March.

Essentially what the Fed is saying is that rate hikes – which they’ve insisted are far off in the future – are being pulled forward. This is a big deal for stocks, which are hooked on Fed stimulus like morphine.

Will the Recent Rise in Inflation Be “Transitory”?

Back in mid-February we wrote about the potential for higher inflation in 2021. The argument was simple: prices collapsed in the early months of the COVID crisis and we were now lapping those price drops.

In that post we warned, “…you can bet that headlines about higher inflation will be screaming this Spring. Given how sensitive the Fed is to controlling its narrative, these headlines will no doubt cause consternation within the Fed.” This is what’s happening with the Federal Reserve’s policy now.

The million dollar question the Fed and investors are grappling with is whether this surge in inflation is temporary. There are plenty of reasons that support the idea that inflation will be transitory.

- Energy prices have risen from extremely low levels in 2020, which won’t repeat as we move forward.

- Global chip shortages will be eased at some point, increasing supply of everything from cars to major appliances.

- Inventories of consumer goods will be replenished, easing shortages.

We don’t expect the big inflation numbers we’ve seen the last two months to continue. They’ll start coming back down the rest of 2021 as the “base effects” we discussed in February run their course.

But the inflation story isn’t over by a long shot. We continue to believe the U.S. economy is entering a period of higher inflation. Political pressure on the Federal Reserve is too high for them to do anything about until inflation becomes a political issue.

Why Will Inflation Persist? Modern Monetary Theory and Current Labor Shortages

I’m sure we’ve all heard anecdotes of the labor shortage currently afflicting many businesses. You certainly have to be more patient waiting for food at restaurants as many don’t have enough servers and cooks on staff!

The current labor shortages are being blamed on overly generous pandemic unemployment benefits. Policymakers have gotten a straightforward answer to the question, “Will people work or stay home if they can earn as much on unemployment as they do working?” They’ll stay home!!

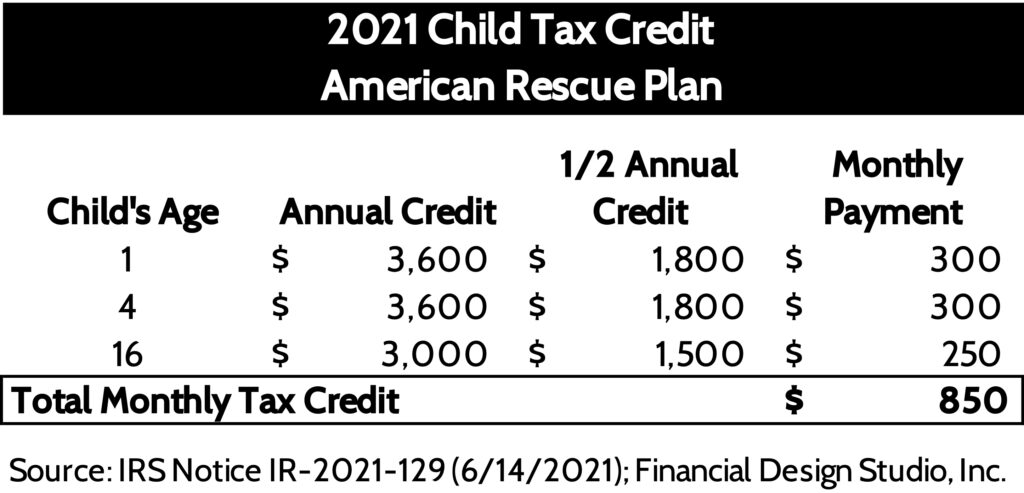

Consensus expects the labor shortage to resolve itself when excess unemployment benefits end in September, but we’re not so sure. The reason? Advance Child Tax Credits.

You can refer to our post last week about the Advance Child Tax Credit but it’s going to send a lot of money to families with kids. We gave an example of what a family of 5 will get each month from July through December. For a $100,000 household, this is the equivalent to a 15% raise in monthly cash flow!

Advance Child Tax Credits are a key policy for supporters of Modern Monetary Theory. They help reduce childhood poverty and reduce income inequality. Expanded child tax credits have bipartisan support. Back in February, Republican Senator Mitt Romney (Utah) floated an even more generous monthly tax credit for families. This was a part of his Family Security Act.

Our view is that these types of monthly payments are going to be with us well-beyond the COVID pandemic. Whether this is through an extension of Child Tax Credits or some other form of Universal Basic Income. And given what we know about worker propensity to stay home and collect checks vs. going to work, it means the current labor shortage will continue. Which means higher prices which means higher inflation.

Why has the Federal Reserve’s Policy Boxed Them Into a Corner? It Can’t Raise Unemployment

When the U.S. last dealt with high inflation in the 1970s and early 80s, then-Fed Chairman Paul Volcker had a solution: slow the economy down. By slowing the economy, it allowed supply and demand to come back into balance, easing price pressures.

The way he slowed the economy down was to hike interest rates to very high levels, to over 18%! This slowed the economy so much that the economy suffered two recessions. In the early 80s the unemployment rate surged to over 10%.

It’s extremely rare for the public to support any government policy that specifically RAISES the unemployment rate. So how were Volcker and President Reagan able to pull this off? Because inflation was BY FAR the biggest economic problem, and a key reason Reagan was elected in 1980.

Fast-forward to 2021. Modern Monetary Adherents view any level of unemployment as unacceptable. The current Treasury Secretary and former Fed Chair, Janet Yellen, has made it clear that her priority is to attack income inequality. And inflation barely registers as a problem in public polls.

How much political cover does the Fed have to raise interest rates – raising unemployment – if inflation gains a foothold? Our view: None. Any mention of rate hikes that risks raising unemployment are going to be met with howls from the public and politicians.

Federal Reserve Boxed Into a Corner: America is Drowning in Debt

The other big issue that’s going to make it difficult for the Fed to raise interest rates is debt. Abnormally low interest rates engineered by the Fed in dealing with past crises has led to an explosion in government and corporate debt alike.

Government Debt

In response to the COVID crisis, government debt has increased by $5 trillion since the end of 2019. Total debt is now more than $28 trillion!

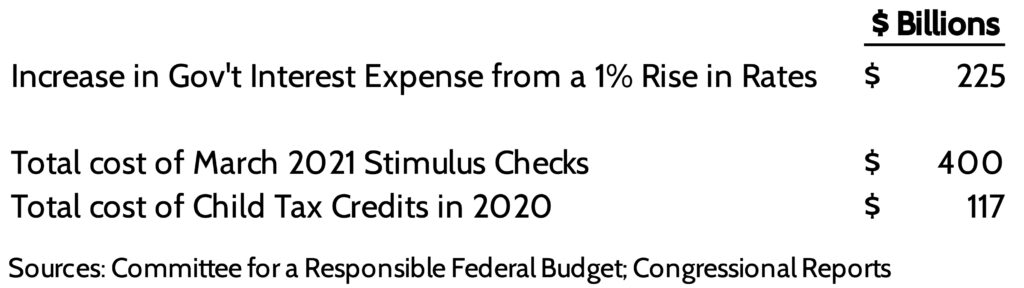

According to the bipartisan Committee for a Responsible Federal Budget, a mere 1.0% rise in interest rates would increase annual interest on government debt by a whopping $225 billion. To put this into context, $117 billion of Child Tax Credits were claimed in 2020 and the cost of the $1,400 stimulus checks sent in March totaled $400 billion. How much can the Fed raise rates to combat inflation without imperiling U.S. finances?

Corporate Debt

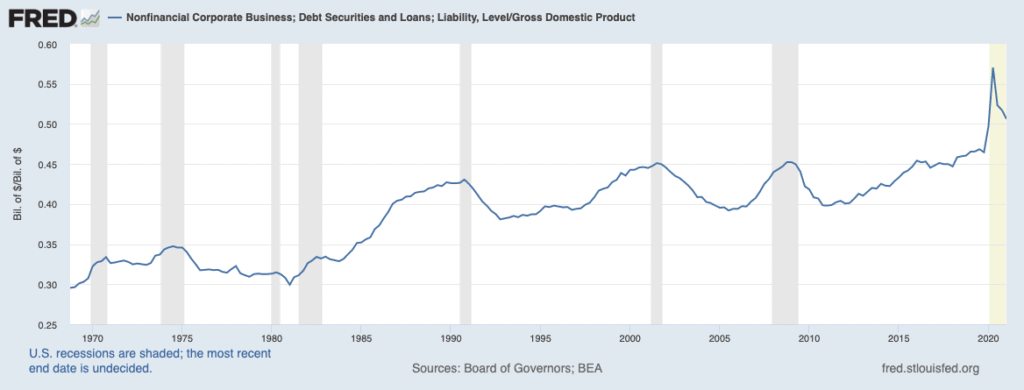

Not to be outdone, Corporate America has also gorged on cheap debt. Normally, when the economy goes through recession, businesses react by reducing debt. You can see this clearly in the graph below, which shows the relative size of non-bank corporate debt outstanding compared to the size of the U.S. economy (Gross Domestic Product).

The COVID crisis turned this normal pattern of deleveraging on its head. In response to the crisis, the Federal Reserve started buying corporate debt for the first time to “support” that market. Instead of reducing debt, this policy encouraged companies to load up on even more debt: over $800 billion of new debt since the end of 2019.

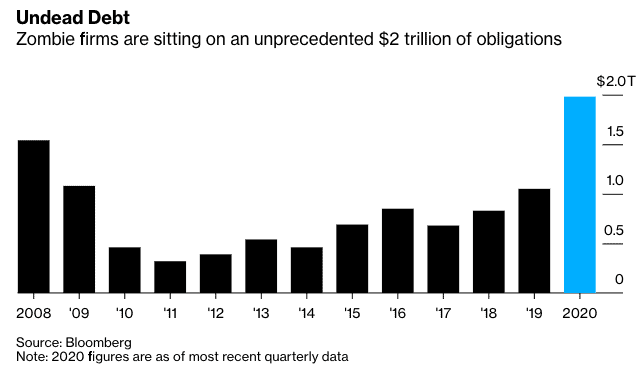

The issue with this corporate debt is that it’s being issued by very weak companies, often called “Zombies.” These zombies don’t even make enough profit to cover the interest cost on their debt. But they’ve been able to rack up more and more debt because of the Fed’s direct support, repeatedly kicking the can down the road.

Effectively, companies that should’ve gone bust in previous economic downturns are being strung along on life support because of the Federal Reserve’s policy. Again, the Fed is “boxed in” from being able to raise rates at the risk of pushing these companies into insolvency, which obviously means higher unemployment for American workers.

Fed Is Cornered and Inflation Genie is Out of the Bottle

Since last summer we’ve had the view that the seeds of a new inflation regime were being sown. We continue to believe this to be the case.

The issue now is that the inflation genie is out of the bottle. The press is talking about it. Consumers are seeing it with gas, food, rents, car prices… almost everything. Some of this inflation will prove transitory, yes.

But the predicament we see is that the Fed has no politically palatable solution to fight inflation should it persist. If they try to raise rates:

- The MMT crowd and those fighting against ever-increasing income inequality (most of society) would howl at the negative effect higher rates would have on unemployment levels.

- The cost of U.S. government debt would rise dramatically, sending deficits even higher than where they are today.

- Higher rates would likely lead to the bankruptcy of many corporate Zombies, putting further pressure on unemployment.

Our Response to the Federal Reserve’s Policy

So in our view, the Federal Reserve’s policy has totally boxed them into a corner. Which is why we expect inflation to prove much stickier than what consensus believes. The combination of extremely low interest rates and money being shoveled at consumers makes this environment different from the low-growth, low-inflation environment that existed before the COVID crisis.

Inflation is the key risk that investors face in coming years. That the Fed is “boxed in” makes the forward path more treacherous if inflation does in fact pan out. Investors (and their advisors!) will have to be nimble to trade around this theme as it plays out.

Over the last year we’ve taken steps to hedge client portfolios against these inflation risks. We’ve shortened bond durations, and have added inflation-protected bonds and commodity exposure.

Investors and advisors alike will have to grapple with this inflation risk. In our view, the days of being able to get away with buying passive ‘total stock market’ and ‘total bond market’ funds are gone. Advisors especially need to think long and hard about constructing portfolios these days, in ways they haven’t had to think about in a long time. Is your advisor doing that?

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

How Will AI Affect the Jobs Market?

White collar workers are wondering how AI will affect the jobs market, and their career. This article shares what's noise and what's real.

Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer

Rob has over 20 years of experience in the financial services industry. Prior to joining Financial Design Studio in Deer Park, he spent nearly 20 years as an investment analyst serving large institutional clients, such as pension funds and endowments. He had also started his own financial planning firm in Barrington which was eventually merged into FDS.