FDS Comment on Silicon Valley Bank Failure

by Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer / March 16, 2023

[Originally sent to clients on March 11, 2023]

If you’re reading the news today, you’re no doubt encountering stories about the second largest bank failure in US history that happened yesterday (Friday.) As is always the case at FDS, we want to let you know what’s going on and how it affects you, if at all.

To skip to the one thing you likely want to know, “is my money safe in my bank,” the answer is YES, with the caveat that you’re not carrying more than $250,000 of cash in a single bank account. FDIC insurance covers all bank account balances under $250,000. And the FDIC has never failed to make depositors whole since 1934. Even if you have cash over $250,000 in a single account, the chances of you having a problem are near-zero. But we’d want to get you under the FDIC Insurance minimum all the same.

Who is Silicon Valley Bank?

Silicon Valley Bank, or “SVB” for short, was a bank based in the Bay Area of California. Throughout its history, it has catered to the technology startup sector, hence the name “Silicon Valley” Bank.

SVB was not like the banks we all see on street corners around us. They catered specifically to venture capitalists and other tech investors. Meaning, as tech companies would raise money on the open markets through IPOs, or get funding from venture capitalists, they would bank with SVB given their “expertise” in serving this clientele.

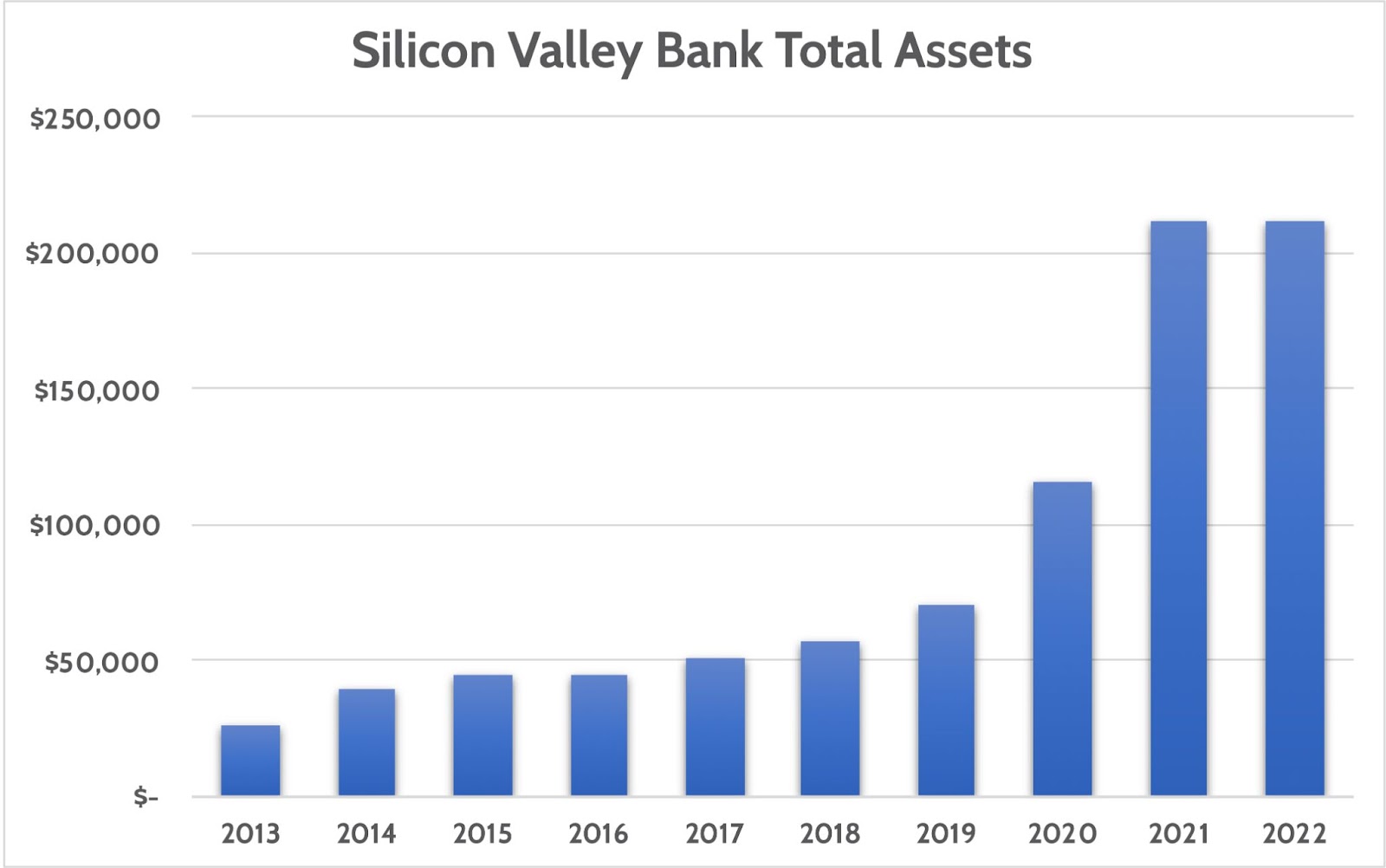

The 2020-2021 tech mania, which launched many unprofitable tech company valuations to ridiculous heights, opened the door to a flood of growth at SVB. As companies went public, they deposited funds into SVB until they could invest them back into the business. Asset growth at SVB exploded as a result, as you can see here.

One thing I learned very early in my career as an analyst of banks is that fast growth is a BAD thing for financial companies. Normally we think of growth as always being good. Not the case for banks and other finance companies. Historically, rapid growth at a financial has almost always ended in ruin, as it’s hard to manage risk when you’re growing rapidly. That was strike 1.

Strike 2 is that SVB didn’t cater to stable, mom & pop retail customers; they catered to the fast-moving tech sector. 93% of all the deposits at SVB were in accounts greater than the FDIC insurance limit of $250,000. That’s way outside the norm in the banking sector. For most large retail & commercial banks, FDIC insurance covers around 50% of their total deposits.

That factor led to their eventual downfall.

Why did Silicon Valley Bank Fail?

Going back to the chart above, we see that SVB’s assets tripled from $70 billion at the end of 2019 to $211 billion by the end of 2021. Massive growth.

When a bank gets a deposit, they have two choices for what to do with the money:

1) Lend it out by originating loans (business loans, mortgages, auto loans, etc)

2) Invest extra cash in (mainly) bond markets

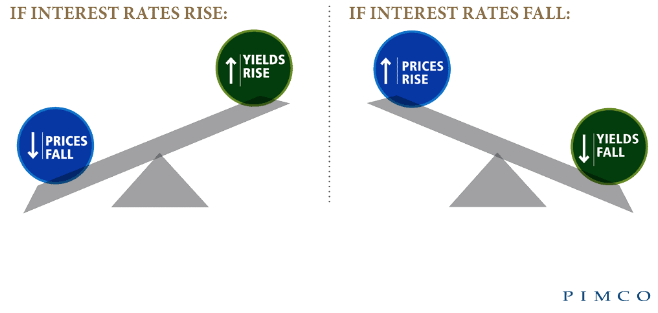

The scale of growth at SVB was so large, they didn’t have enough people to lend to. So they invested most of the new deposits they got into US Treasury bonds and mortgage-related securities. During that growth spurt, interest rates were at extremely low levels, as seen here.

Two years ago we wrote a blog about managing interest rate risk in your portfolio, which included this handy chart.

What we learned in that piece is that the price of bonds FALL as interest rates RISE. Look at where interest rates were during 2020 and 2021, and compare them to where we are today. Huge rises!

Now, imagine SVB plowing tens of billions of dollars into Treasury and Mortgage-related bonds during 2020 and 2021. What do you think has happened to the price of the bonds they bought? Yes, they’ve gone down.

Under normal circumstances that’s not a big issue for investors. US Treasury bonds and government-backed mortgage bonds are risk free. Meaning, if you hold them to maturity, you’re guaranteed to get paid 100 cents on the dollar.

But a bank faces a different type of risk: depositor risk. Remember, SVB bought those bonds using the surge of deposits that came in their doors. And what depositors giveth, they can taketh away as well. And that’s what had been happening at SVB the last few months as tech IPOs dried up and tech companies burned cash.

As of December 31, 2022, SVB had unrealized bond losses of $17.6 billion. To pay for deposit outflows, they’d have to sell some of those securities and take some losses.

After the market closed on Wednesday, March 8, SVB announced they had sold $21 billion of securities at a loss of $1.8 billion. To replace the lost capital, they announced that they’d sell shares of stock and bonds worth $1.7 billion.

We call this “balance sheet repositioning” and it’s not an uncommon practice, although we haven’t seen it much since the mid-2000s. Normally these things go smoothly: take the loss, raise the capital, and get on with life.

But because SVB’s depositor base was heavily concentrated in one client type, tech companies collectively got spooked and tried to pull their money out quickly. So quick, in fact, that they pulled 25% of deposits out on Thursday alone, an amount that far exceeds historical “bank runs.”

By Friday morning, SVB had run out of cash to pay depositors and by noon, the FDIC announced they had seized the bank. This is why the Silicon Valley Bank failure happened.

Insured depositors will get 100% of their money starting Monday. But uninsured depositors face an uncertain future. Their best hope is that a larger bank buys the carcass of SVB for $1 and makes good on all the deposits. Worst case, they’ll have their money tied until the FDIC fully winds SVB down and has money to give back to these uninsured depositors.

Is This 2008 All Over Again?

The natural question on everyone’s mind is, “Is this 2008 all over again?” My answer to that is an emphatic, NO. The differences between now and 2008 couldn’t be more stark. Let me explain why.

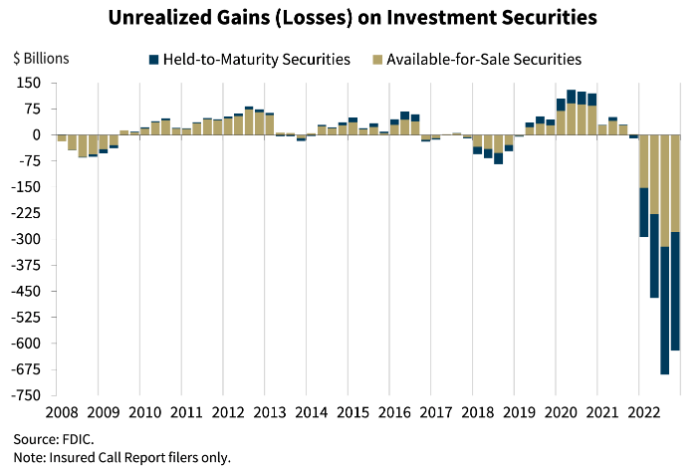

First, we acknowledge that higher interest rates have created unrealized bond losses for all banks, large and small. This chart is from the FDIC, showing total unrealized losses for the US banking system of around $600 billion. Which is a lot, but isn’t massive in the context of $24 trillion total assets in the banking system.

The difference between the “losses” the banking system faces today versus those of 2008 could not be more different. In 2008, banks faced hundreds of billions of losses on subprime mortgages and other esoteric securities that in reality had zero economic value. They faced real losses that would never be recovered because there was no value to them in the first place.

This time around, all the losses we see are being driven solely by lower bond prices because of higher interest rates. But the bonds we’re talking about are US Treasury bonds and government-backed mortgage bonds. There’s ZERO question as to the value of these bonds at maturity: they will pay 100 cents on the dollar. Today’s “losses” are thus a temporary phenomenon that will correct with time.

Second, regulators completely revamped bank capital and liquidity standards after 2008. The bank sector is very well-capitalized. And the largest banks in the U.S. (JP Morgan, Bank of America, Wells Fargo, Charles Schwab Bank, and others) are held to extremely high standards. Not only do these large banks have to carry extra capital buffers, but regulators monitor their liquidity daily. That was not the case for the Silicon Valley Bank failure.

What Happens Next?

There will be a lot of news flow over the coming days on the Silicon Valley Bank failure. The biggest uncertainty is what happens to the uninsured depositors. Will a bigger bank rescue them buying out SVB, or will they face losses and an extended period of litigation?

I could be wrong but I suspect a larger bank will in fact swoop in to buy the remaining assets of SVB. Getting a foothold in Silicon Valley is a lucrative business for investment banks. SVB was a competitor, of sorts. A bank swooping in and saving very nervous uninsured depositors is likely to gain new, loyal, clients for life.

If there isn’t a buyer and uninsured depositors are left holding the bag, then things get more uncertain. No doubt depositors large and small will ask questions about where they bank, and it could cause other banks to experience stress.

If that were the case, then I’d expect the Fed to deploy tools to help banks maintain liquidity. They can open their discount window to banks, providing large amounts of cash to banks that need it.

But the one tool the Fed has to “solve” the problem of unrealized losses on bank bond holdings is to cut interest rates. Remember, banks have these unrealized losses because interest rates have gone up a lot. It works the other way: if rates are cut significantly, then the value of these bonds will explode higher and the losses will largely disappear. Problem solved.

The issue with cutting rates is that the Fed is in the middle of an inflation battle. If they cut rates and pump liquidity into the economy, inflation will only get worse.

How FDS Has Taken Steps to Protect Your Capital

Every client that has gotten a comprehensive financial plan from us has had their cash balances reviewed. You can review the “Cash Management” section of your plan and see plain verbiage on FDIC insurance limits. And if you were a client with more than $250,000 in a single bank account, you’ll find a recommendation to spread that out.

This is what we call “risk management.” It’s not sexy, and most people gloss over that section. But good risk management is a critical part of every financial plan. If you have over $250,000 in a bank account that we’re not aware of, please don’t panic. It’s an easy fix and the odds of you having any issues are near zero. But we’d want to help you get full FDIC insurance all the same.

In your investment accounts, you’re likely aware that we’ve taken 20% of your Stocks allocation and moved it to cash. But we didn’t leave that money sitting in the bank, so to speak. We invested that cash in a government money market fund. These funds aren’t FDIC insured, but they only invest in very short-term, risk-free U.S. government bonds. They’re as safe as it gets.

From an overall investment perspective, we like where our models are invested. Moves made over the last 24 months to reduce interest rate risk, credit risk, and concentration risk remain applicable.

As always, our entire team is here to serve you and answer questions you have, no matter what they are. Please reach out to us if you have questions about the Silicon Valley Bank failure or anything else!

Updated Comments Sent on March 12, 2023

As a follow-up to our email yesterday about the Silicon Valley Bank failure, we wanted to update you with the latest news, which is good news.

The Federal Reserve, Treasury Department, and FDIC jointly announced that Silicon Valley Bank is indeed in receivership (i.e. failed) and that another bank, Signature Bank – a $110 billion asset bank out of New York – was also placed in receivership.

Important are these two key moves to contain the situation:

1) Both FDIC-insured depositors AND uninsured depositors will have access to 100% of their funds starting tomorrow, Monday March 13. Meaning, no depositors are going to lose money from these failures.

2) Starting tomorrow, the Federal Reserve will open a liquidity program for banks to exchange US Treasury bonds and mortgage-backed securities for cash at par. Translation: even if a bank holds a bond that has lost value, they can pledge that bond to the Fed and receive a cash amount as if the bond has zero loss.

The effect of these moves is that in our opinion, the weekend crisis is OVER. Depositors have no reason to worry that contagion will spread to their bank and prevent them from taking money out. Banks now have ready access to cash from the Fed, so the bond losses are a moot point, at least for the next 12 months that this special program is in place.

The Good News

Despite this good news, there’s a lot to digest from what happened since Thursday.

First, while US taxpayers are not “bailing out” uninsured depositors at these two banks, they are effectively getting bailed out by the FDIC, with the cost of such bailout falling to healthy banks. Since the Crash of ’87, the gov’t has routinely bent its rules to protect people that frankly, should have known better. These bailouts have been a direct contributor to where we are today, where bad actors take unnecessary risks with the expectation that they won’t have to suffer the consequences if things don’t go their way.

Second, the speed at which Signature Bank and Silicon Valley Bank failure happened was astounding. As mentioned yesterday, 25% of SVB’s deposits left the bank in less than 24 hours. While depositors had reason to worry, the amount of fear-mongering on social media clearly made what should have been a manageable situation turn into a circus.

We encountered dozens and dozens of flat-out misinformation and false claims of bank insolvencies, largely driven by bad actors who lurk in the shadows waiting to take advantage of “crises” for their own, selfish gain. It’s important we all understand that much of what we see and read on social media is driven by people with an agenda for their own benefit, not ours.

Third, we have the next Federal Reserve interest rate policy meeting on March 21-22. Before this weekend’s crisis, the market was increasingly pricing in a 0.50% increase to short-term rates, as perceptions that the Fed is once again behind the inflation curve mounted. It’s likely they’ll “just” do a 0.25% increase given what just happened.

What about Inflation?

But the reason why we got to where we are is because inflation is not going away. Labor markets are extremely tight and wages continue to grow at uncomfortably high levels (at least for inflation hawks!) The Fed is indeed painted into a corner of their own making. Fight inflation, and stuff starts to break (bank failures); don’t fight inflation and it gets entrenched to the detriment of everyone.

All this means that we continue to be in an environment of elevated risks. Stocks will no doubt rally tomorrow, but we’re far from an “all clear” that would cause us to redeploy cash back into stocks.

At some point, the intersection of our bailout culture, broken political system, and inflation is going to come to a head. The prudent continue to pay the price for bailing out the imprudent.

Where Do We Go from the Silicon Valley Bank Failure?

The Silicon Valley Bank failure was sudden and unexpected. But as financial advisors, it’s our job to look out for these types of issues so we can protect clients. If you have additional question, email our team! We want to make sure we address all of your concerns. However, if you don’t work with us and want this kind of confidence, reach out! We would love to discuss how our services can bring you clarity.

Ready to take the next step?

Schedule a quick call with our financial advisors.