Managing Interest Rate Risk In Your Bond Investments

by Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer / April 8, 2021

Inflation is becoming a hot topic in economic circles. Three rounds of stimulus checks and economic support are pumping enormous amounts of money into the American economy. In response, long-term interest rates have risen from all-time low levels. This brings up an important topic for investors: How do we manage interest rate risk in bonds?

Understanding how changes in interest rates affect your bond investments is important. Clients look towards their bonds as a source of income and stability. But bond prices can move up and down, just like stocks. Thus, it’s important to understand why bond prices might move up or down.

How do Changes in Interest Rates affect Bonds?

Simply:

- If general levels of interest rates are rising, bond prices will be falling

- If general levels of interest rates are falling, then bond prices will be rising

This can feel counterintuitive, so to understand why this is the case, we’ll look at an example.

Example of How Interest Rates Affect Bond Prices

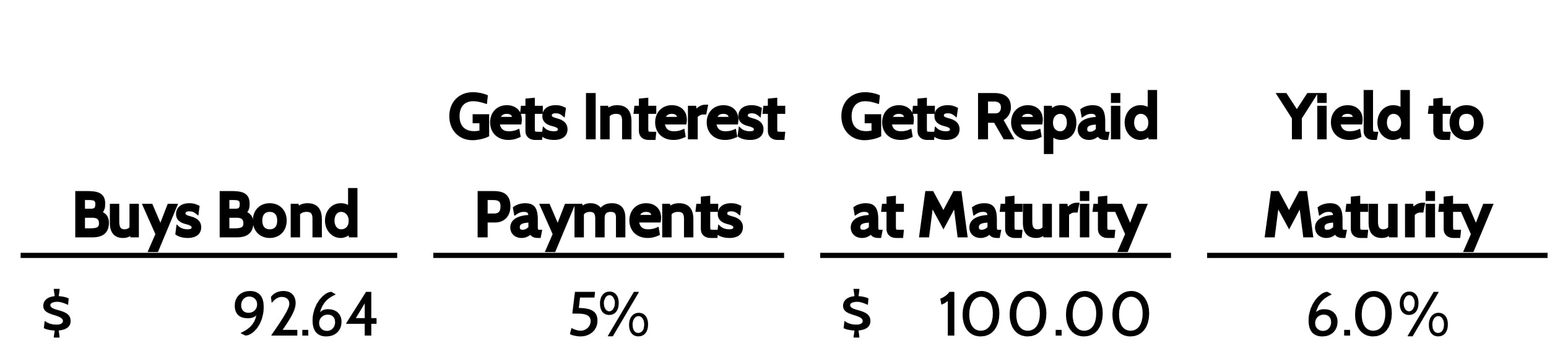

Uncle Charlie calls me up and needs a $100 loan for 10 years. While I love Uncle Charlie, I’m also an investor and know I can get 5% on my money by buying a 10-year bond. So I tell Uncle Charlie, “Sure, I’ll give you $100 as long as you pay me 5% per year.”

The next day, general interest rates rise from 5% to 6%. In my frustration that I could’ve gotten 6% on money I lent to Uncle Charlie at 5%, I call my sister and ask her if she wants to buy Uncle Charlie’s loan. My sister is no fool, and says, “Why would I pay you $100 for a loan that pays 5% when I can lend that same $100 to someone else at 6%??”

Since my sis loves her big brother and wants to help, she comes up with another idea. “I need to earn 6% on my money since that’s what I can get in the market. So if you want to sell me Uncle Charlie’s loan, I’ll give you $92.64 for it to compensate me for the fact that Charlie’s only paying 5% per year in interest.”

The discounted price she’d buy the loan at entitles her to make money above and beyond the 5% interest that Uncle Charlie is paying. In fact, if she buys the loan at that price she’ll end up earning 6%, all in.

Why? Recall that Uncle Charlie is going to give her $100 at the end of the loan term. So my sister would make 5% interest per year PLUS the difference between what she bought the loan for and what she’ll get at the end of 10 years. When you buy a bond for more or less than “par value” (i.e. $100) they call the total return (interest + change in price) the “yield to maturity.”

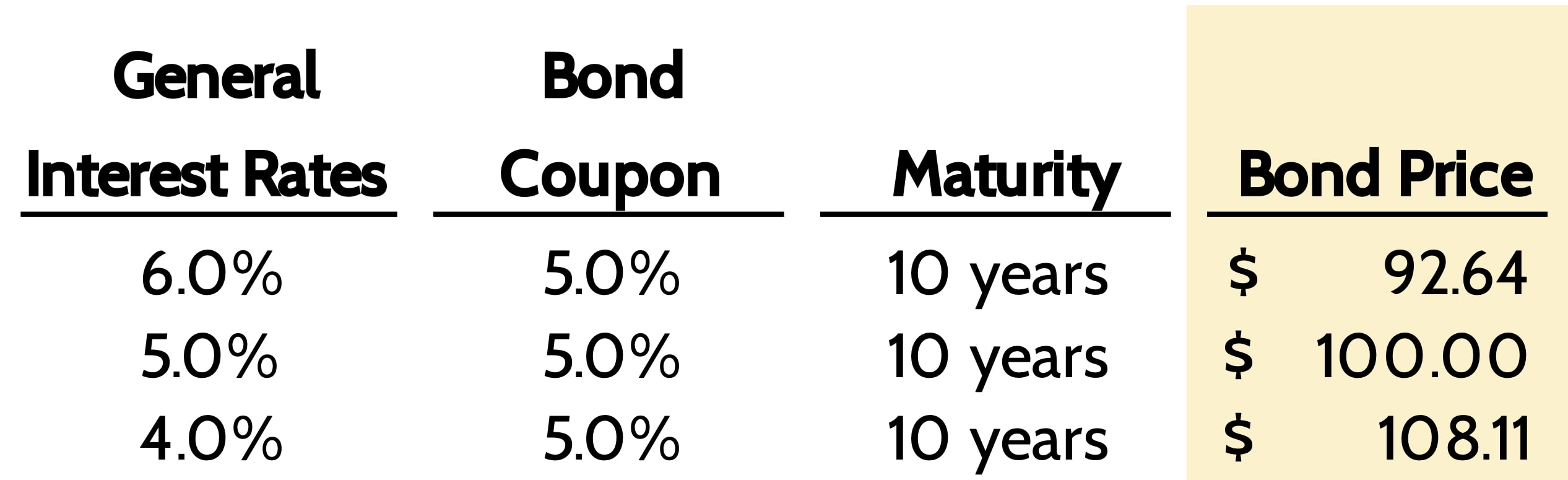

This example shows how changes in interest rates lead to changes in bond prices. Back to Uncle Charlie’s 5% loan. Any time general interest rates change, the price of his loan would change as seen below.

This dynamic is important to understand. It means that the value of the bonds in your portfolio – even ultra-safe U.S. Government bonds – can rise or decline in value before they mature. You might be guaranteed to get $100 at maturity, but that doesn’t mean the price of the bond will always be $100. While bond prices are more stable and move less than stock prices, they will move. This explains how there is interest rate risk in bonds.

Measuring Interest Rate Risk in Bonds With Bond Duration

We avoid financial jargon as much as possible in these newsletters. It’s like getting surgery. You want the doctor to explain to you what they’re going to do in enough detail, but you don’t need all the technicals that go along with it. “Just give it to me straight, doc!”

At the risk of breaking the “no jargon” rule, I want to introduce a term that’s key to understanding how interest rates affect bond prices: Duration. Bond duration is a measure of how much a bond’s price will change for a given change in interest rates. So if interest rates go up 1%, the bond’s price is expected to change X%.

If a bond had high duration, that means its price will be very sensitive to changes in the general level of interest rates, regardless of whether rates go up or down. Conversely, a bond with a lower duration will not see its price move as much when interest rates change.

The key drivers of a bond’s duration are:

- The interest rate the bond pays

- The maturity of the bond (i.e. how many more years until it matures)

For example, a 100-year bond will have a very high duration, while a 6-month bond will have a very short duration. A rise in interest rates will hurt the 100-year bond a lot more than the 6-month bond.

Why Does Bond Duration Matter to You?

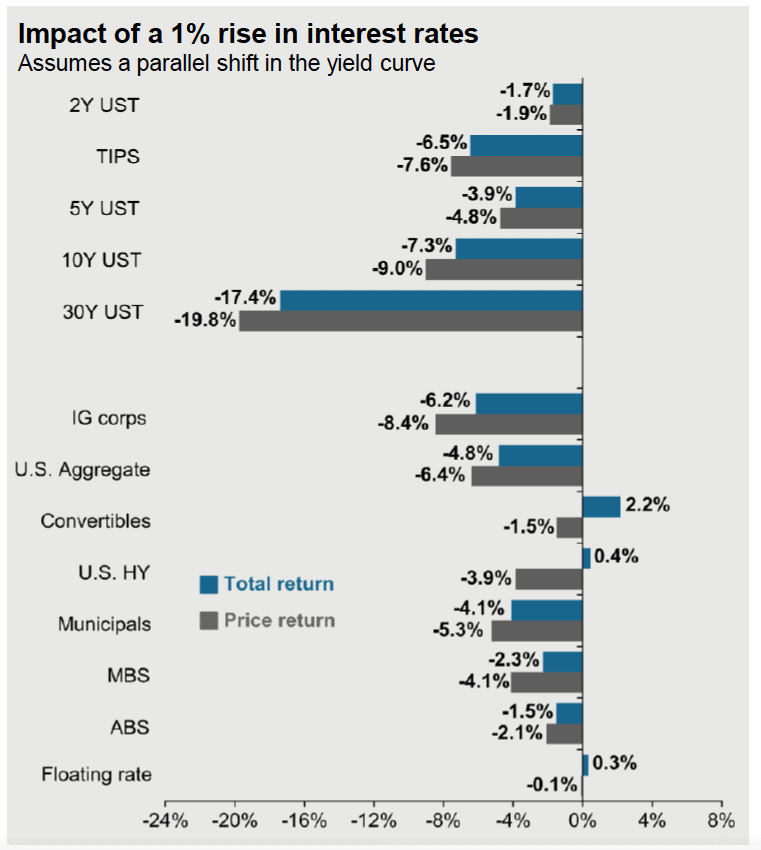

The reason it’s important to have a basic understanding of bond duration is because it has a real impact on the value of your bond investments. JPMorgan Asset Management just published a handy chart looking at the estimated change in value for various types of bonds if interest rates rose +1.0%.

Look at the example of U.S. Treasury Bonds (USTs). Those that mature in 2 years would only decline in value by -1.9% if interest rates rose 1.0%. But for a 30-year UST, the price would decline by -19.8%! This is because 30-year bonds have a much higher duration than 2-year bonds.

The other thing to notice is that an increase (decrease) in interest rates hurts (helps) the value of most types of bonds. Therefore, it’s important for bond investors to have diversified exposure to different types of bonds, just as we recommend for stock investors.

The last 10 years have witnessed extremely low interest rates compared to history. Even with the recent rise in interest rates, they’re as low as they’ve been since 1912.

So why does Bond Duration matter to you? Ask yourself a question: “Based on the last 100 years of history, is it more likely we’ll see higher interest rates or lower interest rates?”

If you answered “higher interest rates” then you can refer back to the seesaw graph at the beginning of this piece. From that, we know bond prices will go down as interest rates go up.

So how can we protect you – the FDS client – from higher interest rates or interest rate risk in bonds?

Answer: By owning bonds with a shorter duration. Lower duration = less sensitivity to changes in interest rates.

The Problem with Passive Bond Index Funds

Passive index investing has become very popular over the last 25 years. Mutual funds and exchange-traded funds (ETFs) that track an index are much cheaper and more tax efficient. It’s been a win-win for many investors.

The problem with passive investing is that you’re beholden to how an index is constructed. And while investing in a “total bond market” fund might sound like the best and easiest way to invest in bonds, it can also expose you to risks you may not be aware of.

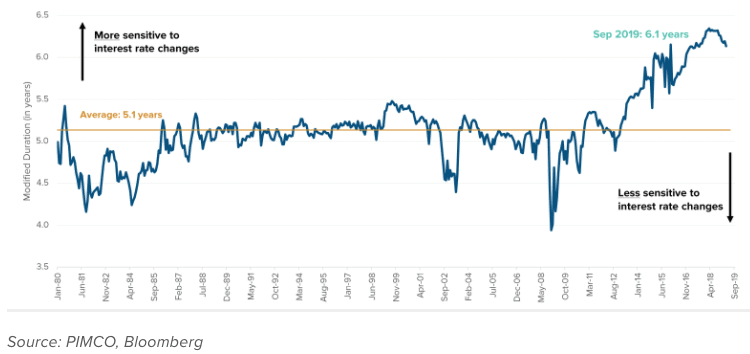

The most popular bond market index is the Barclays U.S. Aggregate Bond Index. Almost every passive “total bond market” fund you find is invested in this index.

From 1980 to the Global Financial Crisis of 2008, the average duration of this Aggregate Bond index was 5.1 years. Since then, the duration (i.e. interest rate risk) of this index has increased significantly.

As of April 2021, the average duration of the Aggregate Bond Index is 6.39 years, near the highest level on record.

The reason duration has increased is that companies and governments have taken advantage of low interest rates to borrow long-term debt. For example, Apple recently borrowed $1.75 billion that won’t be due until 2061 – 40 years from now! The interest rate they’ll pay is just 2.8%. They don’t need the cash, but decided it was worth borrowing money at those low rates!

The rise in overall bond duration over the last 12 years is significant. How significant is this change? At the current level, the overall bond market has 25% more interest rate risk than it has had historically.

Let’s put the pieces together. Current interest rates are the lowest they’ve been in 100 years, meaning the next logical move in rates is higher. Yet the bond market has never had as much interest rate risk (duration) as it does now. Higher rates with High duration = potentially difficult returns for bond investors in the years ahead.

Structuring Bond Investments for a Rising Rate Environment

If we face a backdrop of higher future inflation and eventually higher interest rates, how can we protect against that? One of the key strategies is to make sure you control the duration of your bond investments.

When building stock portfolios, we’re careful to choose investments that are well-diversified. We know we can’t avoid seeing the value of stocks go down in a bear market. But having a well-diversified portfolio of stocks can limit the downside to those events.

It’s the same thought process with Bonds. We know if rates move higher, that will act as a headwind to all bonds. Yet we can control for this risk by constructing a portfolio of bonds with lower duration that mitigates some of this risk.

The goal of constructing a bond portfolio with lower duration is to limit price declines if interest rates increase. The offsetting benefit from this temporary price decline is that the bonds in these funds will mature faster and be replaced with higher-yielding bonds. This will help the yield on your bond portfolio increase in a shorter amount of time.

Nothing’s for free, and there are two tradeoffs with a lower-duration bond strategy. First, the bond yield you get today will be lower than what you’d get on a high duration bond strategy. Second, you wouldn’t benefit as much if interest rates ended up declining instead of increasing.

What We’re Doing to Protect Client Bond Portfolios From This Interest Rate Risk in Bonds

As we step back and look at the big picture, here’s what we see:

- Interest rates are at 100-year lows.

- The government has abandoned any semblance of fiscal restraint in the belief that high debt levels don’t matter.

- The Federal Reserve is explicitly targeting higher inflation.

When we add things up this suggests higher inflation and eventually, higher interest rates to combat said inflation. With that backdrop, it seems prudent to us to be careful with the interest rate risk in bonds in client bond portfolios, even if there are tradeoffs to that strategy. And that’s exactly what we’re doing.

This doesn’t mean targeting a bond duration of zero. That would be akin to stuffing money in a mattress and earning 0% on it. Instead, we’re talking about shifting a portion of bond investments to shorter-duration bond funds, so we stay close to the long-term average duration for the bond market. This is like what we did for clients last Fall when we moved a portion of their bond exposure to inflation-protected bonds.

Investor attention often gravitates towards what’s going on in stocks. Hopefully, this piece helps you understand what’s going on with the “safe” side of your investment ledger – Bonds. You don’t have to be an expert in investing – that’s what you’ve hired us to do for you. But by being informed, you’re empowering yourself to stick with your plan through all sorts of market cycles.

Ready to take the next step?

Schedule a quick call with our financial advisors.