Outlook for Interest Rates and the Budget Deficit

by Financial Design Studio, Inc. / June 24, 2026

Two years ago, we wrote an article on the federal budget deficit and the implications the deficit might have on interest rates. A lot has happened since then, with the 2024 election, April 2025 tariff announcement, a new Federal Reserve chair, and Iran war. At the start of 2026, I was actually feeling a bit more optimistic about the deficit’s trajectory and potential to avoid a negative “fiscal dominance” scenario. But things have changed, and it’s a good time to revisit this topic, as it’s an important one for the stock and bond markets. The two principal topics of this article will be the outlook for interest rates and the budget deficit, which are inextricably linked.

Who is the current Federal Reserve Chair and what is his policy stance?

Former Federal Chair Jerome Powell had two contentious terms in office. He was first nominated by President Trump in Trump’s first term in office, but turned into the President’s punching bag for not cutting rates aggressively at the start of Trump’s second term. Powell also saw his renomination as Fed Chair held up by President Biden in 2021 because of unhappiness with inflation, leading to Powell earning an embarrassing “Chair Pro Tempore” title in early 2022 because of delays in the renomination process.

When President Trump took office in 2025, he was clear that he would not nominate Powell for a third term. Instead, he picked Kevin Warsh to lead the Fed, presumably because he would be more dovish in reducing interest rates. Warsh was confirmed as Fed chair in May 2026.

We don’t have a strong view of Warsh as Fed chair, but the worry in the market is that he’s a threat to the Federal Reserve’s historical independence from political meddling. There may be some truth to that, but if you’ve read any of our articles on the Fed over the years, you know I’ve had a lot of criticism for how the Fed has operated the last 25+ years. That institution could use a little “scaring straight” in terms of increased public accountability, as I’d argue the Fed is the primary cause of many social ills, such as wealth inequality.

What is the 2026 outlook for short-term interest rates?

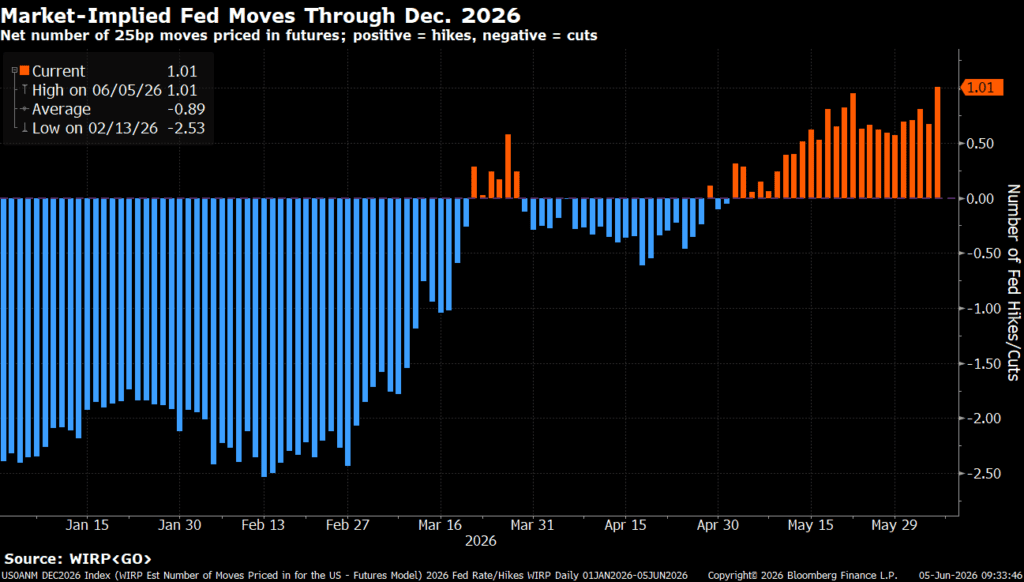

The biggest question on everyone’s mind as Warsh takes the big chair is what will he do with the Fed’s interest rate policy. As mentioned earlier, the market assumes Warsh was brought on to bring a “dovish” approach to rate policy. And if we look at the market’s anticipated interest rate outlook at the start of 2026, that was certainly the base case. However, the Iran War has completely flipped the script on the rate outlook, and the market is now pricing in rate HIKES for later this year.

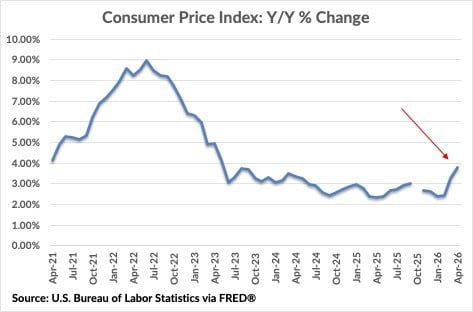

The day before the Iran War, the market was building in 2-3 rate cuts by December 2026 (blue bars, above.) We felt that was a reasonable outlook given that core inflation was cooling off early in 2026. But we’ve seen inflation readings run “hot” recently, with higher energy prices because of the War.

We believe inflation will cool down again once there is a resolution to the War. However, the War has dragged on far longer than people expected, which increases the risk of “sticky” inflation. As seen in the market expectations for interest rates (red bars, above,) Fed Chair Warsh immediately finds himself in a bind. President Trump presumably brought him in to cut rates, but is now “boxed in” by higher inflation because of the President’s decision to attack Iran. I do not think we will see rate hikes this year, but certainly the scope for rate cuts is off the table.

What’s the Outlook for Long-term Interest Rates?

While the Federal Reserve strongly influences short-term interest rates (0-2 years), it has less impact on long-term interest rates. Rates for longer maturities are determined by market participants, such as retirees, pensions, and life insurance companies. These investors look at several factors to determine how much they’re willing to pay for a bond that doesn’t mature for 5, 10, or 30 years. Those factors determine long-term interest rates.

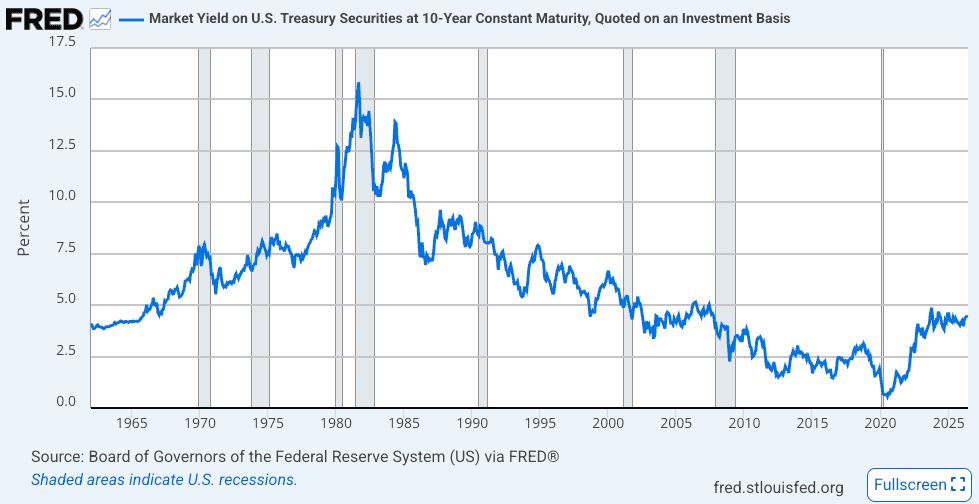

Looking at a long history of interest rates below, it’s hard to say what the “right” number is for normal long-term rates. They’ve been as high as 16% and as low as 0.3%. Making it even harder, we notice that there have been long interest rate cycles, with higher rates from the mid-1960s to early 1980s, followed by lower rates from the 1980s to early 2020s. So what’s the right number?

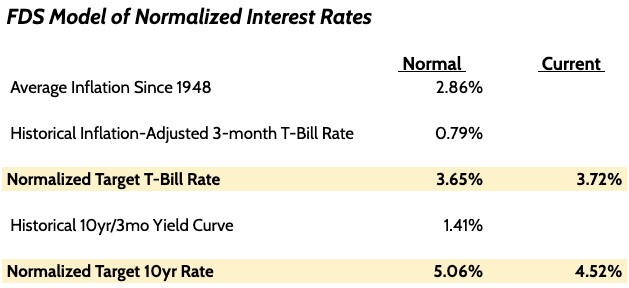

Given the importance of long-term interest rates for stock and bond markets, we created our own model several years ago trying to figure out what the “right number” is. This exercise is not meant to predict where rates are headed in the next several weeks and months, but gives us an anchor to judge how current rates compare to our estimate of normal.

What Are Normal Interest Rates?

Looking at where rates are today, we find that short-term rates are almost exactly in line with our estimate of normal. So when we say (above) that we don’t see any Fed rate hikes or rate cuts in 2026, it’s because we think we’re already at a good, sustainable level.

There’s more uncertainty with long-term rates, as we are roughly 0.50% below our FDS normal. I’d judge this by saying we’re pretty close to normal with a slight upward bias. Meaning, I wouldn’t be surprised or concerned if long-term rates get to 5%.

This model has been a significant factor in changes we’ve made over the years in Client bond investments. In mid-February 2026, 10-year interest rates fell to 4.00%. This was far enough below our estimate of normal that we made changes in client portfolios to reduce sensitivity to rates, ahead of the most recent increase in rates. I don’t have a strong view of where long-term rates go from here, which is why we are “neutral” interest rate risk in our bond investments.

Why Do Interest Rates Matter for the Deficit?

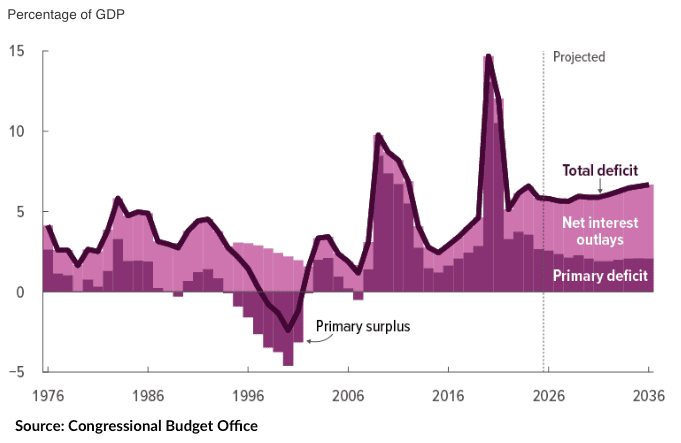

Talk about the deficit ebbs and flows with Congressional debt ceiling debates. But it’s definitely a hot topic because we are experiencing levels of debt and deficit spending that our country hasn’t seen since World War II. For most of the last 50 years, the total deficit has been around 3% of economic output, as measured by Gross Domestic Product (“GDP”.)

Not only are we seeing elevated levels of deficit spending – about 6.5% of GDP – but Net Interest Outlays have become a key driver of the deficit. During much of the 2008-2020 period, the Federal reserve held short-term rates close to 0%. Because of that, long-term interest rates were also abnormally low. This allowed the government to issue a lot of debt with little impact on the deficit because interest costs were so low.

It is encouraging that the “core” part of the budget, called the Primary Deficit, is returning to normal. That’s the part of the budget that Congress can control. Ironically, higher tariff revenues are a component of the improvement. But the question of Net Interest Outlays is a concern that doesn’t have an obvious solution.

What Would Interest Costs be Using Current Interest Rates?

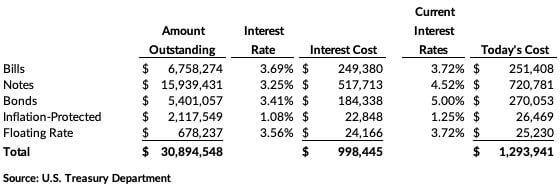

As we see above, the total deficit is over 6.5%. But that doesn’t tell the complete story. Remember, the government issued a lot of debt prior to COVID, when interest rates were abnormally low. With the current debt outstanding and the interest rates on those debts, the projected interest cost this year is $998 billion.

Eventually, however, that low-cost debt will mature and be replaced by debt issued at current interest rates. Because long-term interest rates are higher, we estimate that if we “marked-to-market” the current debt to today’s interest rates, the actual interest cost would be just under $1.3 trillion, almost 30% higher than it is today.

If we then add that potential cost increase into the deficit, we find that today’s already-high deficit of 6.5% GDP would rise to a very high 7.4%. That is an unprecedented level of deficit spending outside of wartime periods.

When we talk about “fiscal dominance,” where the U.S. Treasury and Federal Reserve are painted into a corner, this is what we’re talking about. IF inflation goes up, the natural response is to increase interest rates. But if they do, these debt dynamics worsen, market participants get more worried, and demand higher and higher interest rates as compensation.

What Can the Government Do to Create Sustainable Debt?

There are some ways the government can address high deficits and its relation to the economy’s size, GDP. One way is to cut the primary deficit, as those are Congress directly controls those purse-strings. The problem is much of the primary deficit relates to defense, Social Security, and Medicare spending. Talk of cutting any of these areas are “third rail” issues for politicians.

We’ve already seen that the Federal Reserve doesn’t have a lot of control over long-term interest costs. But there is a tool they have called “yield curve control” whereby they “set” long-term interest rates and simply buy enough bonds to keep rates where they want them. That strategy is fraught with risk, however, as holding interest rates artificially low for extended periods of time creates economic distortions and significantly increases the chances of runaway inflation.

The last arrow in the quiver is economic growth, and this is clearly the path the Administration is choosing to solve the debt and deficit problem. If economic policies lead to higher real gross domestic product growth (“real” means after inflation), then in theory we can grow our way out of the debt and deficit problem.

Can Domestic Growth Beat Inflation?

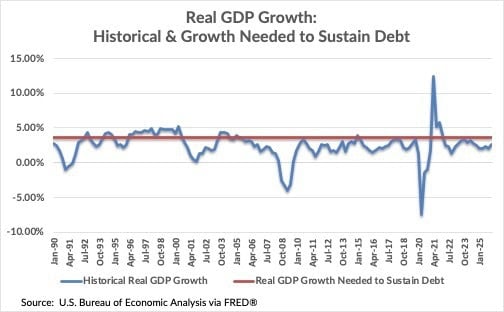

This, however, isn’t guaranteed. To get ahead of the deficit problem, America would have to see nominal GDP growth (“nominal” means real growth plus inflation) of at least 6.5%. In our discussion on normalized interest rates I show that average inflation since 1948 is 2.86%. If we use that inflation rate, the implication is that we’d need to see real GDP growth of at least 3.64% to keep debt from rising more than it is today, as a percentage of GDP. Looking back over the last 35 years, we see few periods where actual real GDP growth (blue line) exceeded the theoretical 3.64% level needed to sustain debt levels.

Normally I’d quickly brush off the idea of accelerated GDP growth. An ageing society and slowing population growth put a governor on potential GDP growth. However, we are in the early innings of what could be a transformative period with Artificial Intelligence (“AI”.) Can AI unlock growth potential that we can’t see today? I think it’s possible, but certainly not guaranteed. But as we think about debt dynamics, this is what everyone is hinging their hopes on, whether or not they admit it.

Outlook for Interest Rates and the Budget Deficit

News flow around the Iran War is dominating headlines, but we think the emerging issue for markets is the outlook for interest rates and the budget deficit. Based on what we know today, we don’t think the Federal Reserve will do much with short-term interest rates. Inflation is high but not spiraling, and economic growth is strong. Hence, the Fed isn’t in a position where they have to make a move on rates.

Longer-term interest rates are below our estimate of normalized interest rates, but not too far off. But what happens with long-term interest rates has a significant impact on federal deficit dynamics. We’ve seen that neither Congress nor the Fed have many tools in the toolbox to deal with higher long-term rates. But this interplay between the deficit and interest rates remains the biggest risk we see to the markets and the economy.

Managing FDS Client Portfolios

Most importantly for clients is how we manage investments in relation to these risks and opportunities. Moves in inflation and interest rates have a significant impact on portfolios. For stocks, this means what type of stocks do best – value versus growth, domestic versus international, large company stocks or small company stocks. Not to mention the weight in commodities that we carry in the portfolio as an inflation hedge.

These dynamics also affect what bonds we own in client portfolios. Do we want more sensitivity to moves in interest rates, or less? Do we want higher quality bonds, or is the environment favorable to riskier, but higher-yielding bonds?

We are constantly considering these questions in relation to fast-moving markets and abrupt economic changes. You, the client, are paying us to be your “feet on the street” making sure your hard-earned savings are A) protected, and B) put in position to grow. It’s a balancing act that requires diligence and attention. To hear our thoughts on this situation further, watch our June 2026 Investment Update.

If you are nearing retirement and you don’t want the pressure of “getting it right,” we would love to work with you. Our team specializes in retirement planning for professionals who have executive compensation, and who want tax efficient investment management. Schedule a 30 minute introduction call to see if we are a fit.

Bonus Resource: Our Retirement Planning Guide!

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

Leaving a Legacy by Thinking Two Generations Deep

With your finances, you have the opportunity to impact generations after you. In this article, we discuss the strategies for leaving a legacy!

Tax Law Changes From the One Big Beautiful Bill Act (OBBBA)

The One Big Beautiful Bill simplifies tax planning with low tax rates and other benefits for retirees and business owners.

Financial Design Studio, Inc.

We are financial advisors in Deer Park and Barrington, IL. A team with a passion for helping others design a path to financial success — whatever success means for you. Each of our unique insights fit together to create broad expertise, complete roadmaps, and creative solutions. We have seen the power of having a financial plan, and adjusting that plan to life. The result? Freedom from worrying about the future so you can enjoy today.