Do I Own Too Much Company Stock?

by Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer / February 5, 2025

Corporate executives are receiving more stock as part of their compensation than they did 20 years ago. Boards and management prefer stock-based compensation because it helps align employee interests with those of the company’s shareholders. While receiving company stock can be a fantastic way to build wealth, it can also come with risks. Overconcentration of wealth in your employer can be problematic if the company underperforms, or worse, encounters financial difficulties. We will look at the ways executives receive stock in their employer, the risks of owning too much company stock, and how executives can avoid the nagging question, “Do I own too much company stock?”

Key Takeaways

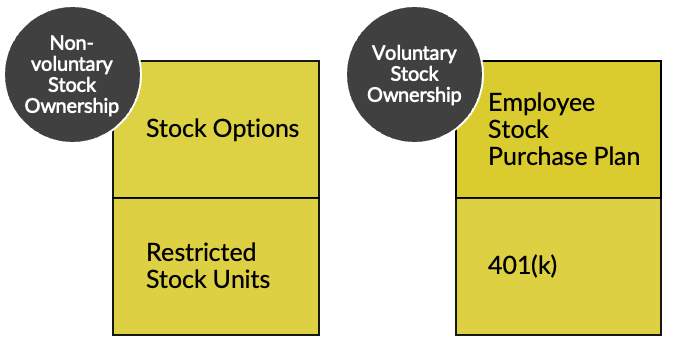

- There are four principal ways you can accumulate stock in your company. Two are involuntary payments of stock as part of a compensation plan. But the other two methods are entirely in the employee’s control.

- The value of company stock you own should only include what you actually own today, not the potential value of unvested stock options and restricted stock units.

- No more than 10% of the total value of your investments should be in company stock. Anything above this level risks jeopardizing your future retirement plans.

- Setting strict limits on the size of company stock protects you from getting overconfident in your company’s prospects. History is littered with examples of formerly dominant companies that subsequently lost a lot of value.

- You should consult with a financial advisor before attempting to reduce exposure to company stock, to avoid any tax surprises. Further, many companies restrict your ability to sell company stock once you own it.

Four Ways Executives Accumulate Company Stock

Stock ownership in an executive’s employer has become prevalent. Several years ago, stock ownership used to be reserved for upper management. But these days, companies give stock to employees as part of their compensation package. They also offer other ways for employees to purchase stock on their own. Here are the four most common ways executives accumulate company stock.

Stock Option Grants: Companies may grant employees stock options to purchase company stock after a vesting period. Once the options have vested, it is then up to the employee whether to exercise those options to purchase stock at a pre-determined price.

Restricted Stock Units: Also known as “RSUs,” grants of restricted stock are often happen annually with vesting periods up to four years. Unlike stock options, once an employee’s RSUs vest, they immediately become shareholders in the company, less any tax withholdings. The employee then has to decide whether to keep or sell the stock they receive.

Employee Stock Purchase Plans (“ESPPs”): This is a voluntary program that allows employees to buy stock regularly and at a discount to the prevailing stock price.

401(k)s: Many companies, but not all of them, allow employees to buy stock in the company using contributions into their 401(k). Like ESPP, buying stock in one’s 401(k) is completely voluntary.

By understanding how each of these methods work, an employee can better manage the size of their stock exposure to their employer. But how much stock is too much?

How Much of My Wealth is in Company Stock?

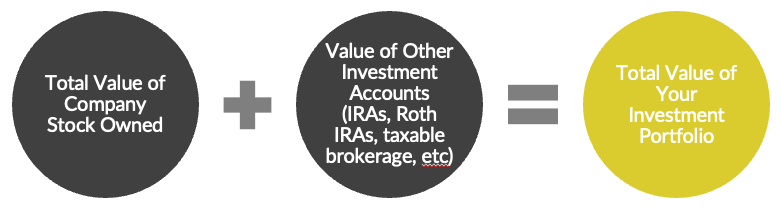

The first step to answering the question, “Do I own too much company stock?” is to understand exactly how much you own! It might seem like a straightforward question but can be tricky to figure out when you go to do it. The graphic below gives us an overview of all the information we need.

What’s Included:

- Direct stock ownership in brokerage accounts and RSU accounts. Stock you own in brokerage accounts might be stock you bought yourself on the open market. But we also want to include any direct stock holdings that are in the account that hold your RSUs. When RSUs vest, your company will automatically put the vested shares (net of taxes) in this RSU-managed account.

- Total value of stock that’s your 401(k) holds, if any.

- Value of all stock you’ve accumulated in an ESPP. Like stock received from vested RSUs, the stock you purchase via ESPP is likely in its own account. This is is provided to you by your company.

- Vested stock option value. These are stock options that, A) have value, as the current stock price is above the option’s strike price, and B) has vested and is available for you to exercise at your discretion.

What’s Not Included:

- Unvested value of RSUs. On your RSU statement, you will often see a value published for all your unvested RSUs. But we do not want to include this because technically, you don’t own the shares until they fully vest.

- Unvested value of stock options. Similar to RSUs, unvested options may appear to have value to them based on where the stock price is relative to the option’s strike price. But until they have become vested and exercisable, they don’t technically count as stock you own.

Once you know the total value of the stock you own in your company, you can then compare that to the value of ALL your investments, including company stock.

The proper way to assess the size of your company stock exposure is to express it as a percentage of your total investments. Here, you’d take “Total Value of Company Stock Owned” divided by “Total Value of Your Investment Portfolio.”

Do I Have Concentration Risk in my Employer’s Stock?

Now, we get to the million dollar question: “Do I own too much company stock?” First, some bad news. There is no hard-set rule on how much is ‘too much.’ If you peruse the internet, you’ll see people say that 5% is too much. Others say you can have up to 20% of your portfolio in your company’s stock and be fine. Our view is that you don’t want to have over 10% of your total investments in company stock. Why 10%?

We have to remember what these long-term investments are for: funding your future expense needs. Most often, we think of retirement as being the main long-term goal. And when you’re retired, all the savings in your 401(k)s, IRAs, and company stock will need to be enough to sustain your basic living needs and goals in retirement. Including,

- Covering remaining mortgage payments and future property taxes

- Meet basic living needs, such as food, gas, and insurance

- Health-related expenses in retirement, including the possibility of needing long-term care

- Funding retirement goals, such as an annual travel budget

Investing involves risk of investment loss, whether it’s because of a short-term market correction or a permanent impairment of a specific investment.

From working with clients and their retirement plans, we believe that most retirees can sustain a permanent loss of investments on the order of 10% and still be in good shape for their retirement. Yes, it would take some minor adjustments here or there, but a 10% loss will not make or break the bank.

Having single-stock exposure like an employer’s stock significantly increases the risk of seeing that investment go to zero. Even if it’s a tiny probability event. By recommending that clients keep their total exposure to company stock at 10% or less, we acknowledge the value in holding that stock. But we also know there’s a ton of value in knowing your retirement savings are well-diversified.

Holding over 10% of your investments in employers stock increases the risk that you may have to “reboot” your long-term retirement goals if something goes wrong at the company. And there’s precedent for that happening.

Enron Employees Nearly Lost it All in 2001

In the late 1990s, a company called Enron was revolutionizing energy markets. For the first time, traders could bet on electricity prices and other energy goods on the open market. The company grew quickly, and its stock did well.

As late as March 2001, the stock was still riding high at $75 despite the overall market dropping in the bursting of the Internet Bubble. However, during the Summer of 2001, allegations of wrongdoing were reported. Those concerns accelerated throughout Summer and into Fall.

Eventually, it was reported that there was massive fraud at Enron. And by December 31 of 2001, the stock price had plunged all the way to $0.57 and the company eventually went bankrupt.

During the boom years, Enron gave employees lavish amounts of Enron stock as part of their compensation. Worse, the company had encouraged employees to buy Enron stock in their 401(k), to where Enron stock made up over 60% of the total value of all investments in Enron’s 401(k) plan!

In less than 12 months, employees had gone from thinking they worked for a great, fast-growing company, to having it wiped out. Employees ended up losing:

- Jobs and salaries, which they depended on to pay their mortgages and buy groceries;

- Health insurance benefits

- Nearly 100% of all stock options and RSUs they had accumulated

- Over 60% of the value of their 401(k)s

This is an extreme example, but it’s a reminder that you have several “risks” related to your employer. Not only the value of stock, but your job, income, and valuable benefits!

How Can I Diversify Portfolio Exposure to Company Stock?

You may think, “Shoot, I have a lot more than 10% of my investments in company stock…what do I do?!?” This is where careful financial planning comes in; exactly the work we do for corporate executive clients at FDS. The ideas below are not recommendations, nor should you act on them until you’ve consulted with a financial advisor, such as FDS.

Restricted Stock Units: The best way to control the size of your company stock holdings if you get RSU grants is to sell some or all of that stock when it vests. There’s nothing disloyal about selling down company stock when the goal is to diversify those investments, protecting their value. However, before you sell any shares, make sure you understand WHEN you’re able to sell stock. Companies will often prohibit employees from buying or selling company stock outside of trading windows.

Stock Options: Options that have vested and have value are trickier to deal with. This is mainly due to potentially sizable taxes that come with any sale. But like RSUs, there’s a standard strategy called “exercise and sell” that realizes the value of the options but sells them right away. You can invest the proceeds in a diversified portfolio.

Employee Stock Purchase Plans: If you’re holding too much company stock and take part in an ESPP program, the first step might be to stop taking part in ESPP. Yes, you lose the benefit of purchasing stock at a discounted price. But remember that you’re trying to control the risk to your overall portfolio.

Stock held in a 401(k): If you’ve been buying company stock in your 401(k), the first logical step would be to stop buying stock with future contributions. But if you already own a lot of company stock in your 401(k), it is NOT recommended to immediately sell out of it. If the value of the stock has gone up a lot, you may take advantage of an attractive tax strategy called Net Unrealized Appreciation.

It’s very important to get advice if you find yourself with too much company stock that you want to reduce. We work with clients regularly on reducing company stock in a way that’s tax-friendly and consistent with your long-term goals. Please hit “Get Started With Us” if you find yourself in this situation!

Do You Own Too Much Company Stock?

If you’re a corporate executive, having too much stock exposure in your company qualifies as a “hidden” risk. And even if it’s not an issue today, it’s likely that yearly stock-based compensation will add up to a significant amount of wealth.

Helping you understand your investments and any associated risks is what we do. Our in-house tax planning can also help you reduce over-exposure to company stock in a thoughtful, tax-friendly way.

Stock-based compensation is a powerful wealth-building tool. We can help you, the corporate executive, determine how best to take advantage of this important benefit. Your career is important, but we also know there may be spouses and children you’re planning for as well. We at Financial Design Studio will help you make sense of all the complicated benefits you’re entitled to. This helps you build a future financial plan that fills you with confidence about your future.

Bonus: Our Retirement Planning Guide

Ready to take the next step?

Schedule a quick call with our financial advisors.