How Much Will Healthcare Cost in Retirement?

by Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer / September 16, 2025

The United States is at the peak of what’s called “Peak 65.” 2025 represents the year that the highest number of people will turn 65, nearly 4.2 million people. Based on life expectancies, people who reach age 65 can expect to pay $165,000 in Medicare premiums over their remaining lifetime. Then there are out-of-pocket costs for deductibles and copays, which add even more costs. Financial advisors encourage retirement savers to think about all the vacations they’ll be able to take when they’re retired. But there is too little attention paid to how much healthcare will cost in retirement, and more importantly, how to prepare for those costs. This article will look at the healthcare challenges retirees face and ways anticipate future expenses.

Contents:

- Challenge 1: Have Medicare Part B Premiums Risen Faster Than Inflation?

- Challenge 2: Does High Income Lead to Higher Medicare Premiums?

- Challenge 3: How Much Does Long-term Care Cost in Retirement?

- Implementing a Plan to Cover the High Cost of Healthcare in Retirement

If you are looking to learn more about funding your healthcare, we’ve written a helpful article titled, “How to manage the high cost of healthcare in retirement.” Keep reading to learn about the expected costs!

Challenge 1: Have Medicare Part B Premiums Risen Faster Than Inflation?

Since Medicare was established in 1966, almost all Medicare recipients have paid a monthly premium for Medicare Part B. This monthly premium started at $3/month in 1966 but has risen to $185/month in 2025. Since 2000, Medicare Part B premiums have risen by nearly 6% each year.

General inflation has risen 2-3%, on average, over the last several decades. Increases in Medicare Part B premiums have been twice as fast. Medicare Part B premiums are automatically taken out of Social Security checks, so many retirees don’t even notice these increases are happening. At the current Part B premium of $185/month, Medicare costs can reduce a retiree’s Social Security check by 5-10% or more.

Challenge 2: Does High Income Lead to Higher Medicare Premiums?

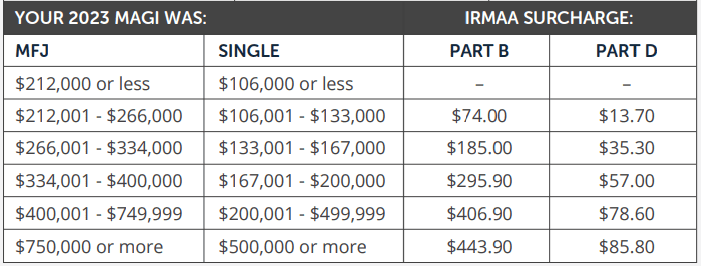

Another increasing cost of healthcare in retirement is the Medicare Part B income-related surcharge the government imposes on high-income earners. In 2025, the Income-related Monthly Adjustment Amount (“IRMAA”) starts imposing higher Medicare Part B premiums on married couples with more than $212,000 of income or $106,000 for single taxpayers. These premium surcharges range from $74.00-$443.90/month. This can add a significant amount to the monthly cost of Medicare. Note that “income” is defined as Modified Adjusted Gross Income (“MAGI”), which takes your Adjusted Gross Income and adds back tax-exempt income.

Here are some common causes of retirees paying an IRMAA:

- Pension income from corporate or public sector pension plans

- Significant investment income from large, non-retirement investment accounts

- Large Required Minimum Distributions from pre-tax retirement accounts

Pro Tip: If there was an unusual, one-time circumstance that caused your income to increase that subjected you to IRMAA charges, you can appeal by filling out the Social Security Administration form SSA-44.

Pro Tip: Roth Conversions in early years of retirement can reduce future required minimum distributions, and help keep income below IRMAA levels.

In their 2024 Annual Report, the Federal Hospital Insurance Trustees estimated that 7% of Medicare recipients currently pay a combined $13 billion of IRMAA surcharges. Their projections for the next 10 years show that the number of people paying IRMAA surcharges will increase by +53% and that the total surcharges collected will surge to $34 billion. For high-earning corporate executives coming up on retirement, this means having to prepare for the possibility of even higher Medicare costs.

How Much Savings are Needed to Cover Lifetime Medicare Costs?

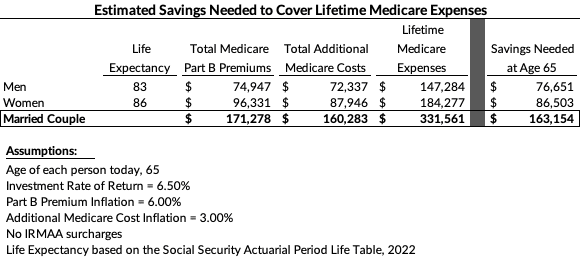

The costs referenced above only apply to the base Medicare Part B premiums, which nearly everyone has to pay when they apply for Medicare. But beyond this, there are costs for additional Medicare coverage, whether that comes from Medicare Advantage plans or a Medigap plan. And the additional coverage purchased may or may not include Part D coverage for prescriptions.

These costs on top of Part B premiums will vary based on each person and where they live. When we are building retirement plans for clients, we assume each person will incur $240/month of these additional costs. That is $2,880 of additional coverage per year on top of 2025 Part B premiums of $2,220, for a total cost of $5,100 for Medicare, per person, per year, with those numbers increasing for inflation.

To see the total potential cost of Medicare coverage in retirement, we can use these numbers above with estimated life expectancy for men and women who reach age 65.

As the table above shows, the costs and expected savings needed to cover each person’s expected Medicare costs are significant. A married couple would need more than $160,000 in retirement savings stashed away at age 65 just to cover these costs.

If you are looking to learn more about funding your healthcare, we’ve written a helpful article titled, “How to manage the high cost of healthcare in retirement.”

Challenge 3: How Much Does Long-term Care Cost in Retirement?

Beyond the day-to-day costs of being on Medicare, retirees face the prospect of needing long-term care at some point. A 2022 study from the Department of Health & Human Services estimates that up to 56% of retirees will need some form of long-term services and support. The fact it’s nearly a 50-50 shot of needing long-term care makes planning for this potential expense very difficult.

These are all the factors that make estimating long-term care expenses difficult:

- Will I need long-term care? Studies suggest 56% of people will need some form of long-term care.

- How long is someone normally in long-term care? The 2022 HHS study referenced above estimates that if someone needs long-term care, they will need it for 3.1 years before they ultimately pass away. But a significant 22% of people would need long-term care for 5 years or more.

- What level of long-term care would I need, and what is the cost difference? Genworth, a major player in long-term care insurance, says that the average cost for assisted living is $6,129/month. The same Genworth study estimates that a memory care facility costs an average of $7,785/month.

- Does the cost of long-term care depend on the state I live in? Yes. Monthly memory care costs range from $5,550/month in low-cost states to over $10,000/month in high-cost states.

- Should I get long term care insurance? This is a question clients ask us often, and we actually answer this in our video: “Should I get long term care insurance?” Watch it to learn more about your long term care options and how to pay for each.

Given these factors, we work carefully with clients to stress their retirement plans for potential long-term care needs. Here is an example of how we might estimate long-term care costs for a client in 2025, assuming they are 65 years old today and expected to live into their mid-80s.

Again, we see that the potential cost of long-term care in retirement could be high. We understand that the uncertainty of future long-term care needs can be stressful, not only emotionally but financially. Therefore, we help corporate executive clients build these potential costs into their plan while they’re still saving for retirement.

If we add this potential cost to the estimated total cost of Medicare in retirement, we find that the total savings needed in 2025 if someone is age 65 is nearly $200,000 per person. The estimates here look at the potential costs for women, who live longer. To put this into perspective, if a retiree is going into retirement with $1,000,000 of retirement savings, healthcare expenses may eat up over 20% of those savings. It’s why we build these costs into retirement plans while clients are still working, so they can adjust the amount they’re saving for retirement, if needed.

How Can Health Savings Accounts Pay for the High Cost of Healthcare in Retirement?

We’ve seen how expensive healthcare in retirement can be and the amount of savings needed to cover those costs. When we do financial plans for clients – regardless of their age – we are building these future costs right into their plan so they can prepare for them.

One strategy we may recommend for a client is to open and fund a Health Savings Account, or “HSA.” These accounts act much like the IRAs and 401(k)s we’re familiar with saving for retirement, except they’re designed to handle medical expenses. We have an in-depth article that describes the benefits of HSAs, but here are the key things to know about HSAs.

Pros of Health Savings Accounts (“HSAs”)

- Tax-deductible contributions;

- Tax-free growth of HSA investments; you are not taxed for investment income nor capital gains as long as the investments stay in the HSA;

- Tax-free withdrawals for Qualified Medical Expenses, as defined by the IRS;

- HSAs can cover COBRA medical expenses, which can be a helpful tool for early retirees;

- Medicare Part B premiums are a Qualified Medical Expense and can be paid for from an HSA;

- There is no time limit for when savings in HSAs need to be used.

Cons of Health Savings Accounts (“HSAs”)

- Requires being on a High Deductible Health Plan, which may be cost-prohibitive for individuals and families with high annual healthcare needs;

- For those younger than age 65, withdrawals from an HSA for expenses not considered a Qualified Medical Expenses are taxed at ordinary income tax rates plus a 20% penalty;

- For those age 65 or older, withdrawals for non-medical expenses are taxed at ordinary income tax rates, but the 20% penalty is waived;

HSAs work best for healthy individuals and families who’ve already maxed out their 401(k)s. HSAs act as a pool of savings dedicated to paying for future healthcare expenses, either before or during retirement.

What Changed for Medicare in 2025 & 2026?

The Inflation Reduction Act of 2022 changed Medicare rules with the goal of limiting costs for retirees. The most significant change was implementing an annual out-of-pocket cap for Medicare Part D prescription costs to $2,000 in 2025. Previously, this cap was as high as $8,000. However, this out-of-pocket cap is indexed with inflation and will rise to $2,100 in 2026.

To learn about what parts of Medicare you may need in retirement, watch our video: “What Kind of Medicare Coverage Do You Actually Need?”

Implementing a Plan

Financial Design Studio creates tailored financial plans for corporate executives and retirees. In these plans, we provide specific advice about how much the client should save for needs like healthcare costs in retirement. Here are a few examples of suggestions we might make:

- For working clients, we may recommend maxing out an HSA. For 2025, a single taxpayer can contribute up to $4,300/year to an HSA while a married couple can contribute up to $8,550. In both instances, an additional $1,000 can be contributed to the HSA if the taxpayer is age 55 or older.

- For retirees, we update their retirement plan projections each year to make sure their savings remain sufficient to cover future needs. As part of these annual updates, we may run stress-tests on the plan for a long-term care event.

Regardless of age, we recommend raising awareness of the high cost of healthcare in retirement. These are actual costs that will have to be funded from retirement savings and Social Security income.

Next Steps for High Cost of Healthcare in Retirement

If you’re worrying about future healthcare costs, you don’t have to sit with that uncertainty. Healthcare is just one piece of your retirement plan. Internet searches can never give you the answers that will resolve your worries. Your retirement planning questions need personalized answers. That’s where our team of planning specialists would love to step in.

If you want expert answers to the questions you don’t even know to ask, reach out! Click the yellow “Get Started” button below or the top-right corner of our website. Our team would love to give you confidence for your retirement.

Bonus: Retirement Planning Guide

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

Should I Retire Early? The Pros, Cons, and Hidden Costs [Video]

In this video, we explore the financial pros and costs, as well as the hidden costs we see as financial advisors when clients retire early.

Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer

Rob has over 20 years of experience in the financial services industry. Prior to joining Financial Design Studio in Deer Park, he spent nearly 20 years as an investment analyst serving large institutional clients, such as pension funds and endowments. He had also started his own financial planning firm in Barrington which was eventually merged into FDS.