CARES Act For Businesses: Employee Retention Credit

by Michelle Smalenberger, CFP® / March 31, 2020

CARES Act For Businesses: Employee Retention Credit

If you do not receive a loan from SBA as a result of the other portions of this law, you may be able to claim a very favorable tax credit. This is a refundable credit that goes against the businesses’ share of Social Security taxes, typically 6.2%.

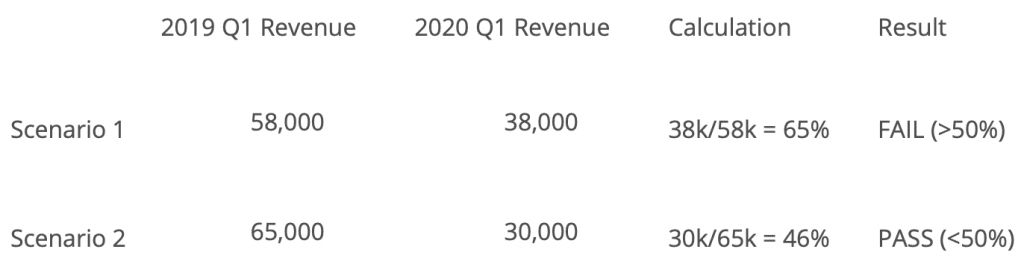

First hurdle: Compare Quarterly Revenue for 2020 to that same quarter in 2019. If 2020 is less than 50% of 2019, you pass.

If your business has had this experience and you qualify, then what’s next? Well your business will continue to qualify for this credit until the earlier of the following events:

- End of the Year

- Revenue reaches 80% of gross revenue from the same quarter in 2019.

In other words, the credit is only available for 2020. But if your business recovers significantly before the end of the year and revenues are back at 80% or more as compared to 2019, you’ll no longer qualify.

Okay, great, but how do you calculate the credit? Thankfully, for small businesses, the credit is fairly easy to calculate. It’s simply 50% of eligible wages up to $10,000/quarter. In essence, a maximum of $5,000 per quarter per employee.

A few examples with various employee quarterly compensation below:

|

Quarterly Compensation |

Calculation |

Quarterly Credit Amount |

|

| Employee A: Sally |

$25,000 |

Only first 10k is covered at 50% |

5,000 |

| Employee B: John |

$19,000 |

Only first 10k is covered at 50% |

5,000 |

| Employee C: Michael |

$4,000 |

50% of 4,000 = 2,000 |

2,000 |

| Employee D: Rebecca |

Q2: $6,000 Q3: $12,000 |

Q2: 50% of 6,000k = 3,000 Q3: Only first 10k is covered at 50% |

Q2: 3,000 Q3: 5,000 |

So if you had both John and Rebecca on your payroll, you’d receive a credit of $8,000 for Q2 and $10,000 for Q3 for the rest of the year so long as your business met the initial criteria of 50% drop in revenue, hasn’t recovered to 80% of revenue compared to same quarter 2019, AND isn’t taking a covered loan from SBA as outlined.

Interested in the other areas of the CARES Act? We are breaking down these details by section in the following resource. You can click to the particular section you’re interested in directly below if you’d like to read the specifics of those first. We do encourage you to look through all of the sections that could potentially impact you since this is a very generous bill aimed at keeping our country’s economy strong during and after this pandemic.

Financial Design Studio CARES Act Summary

Like any benefit that becomes available to you it is critical to see if it makes sense to use the provisions allowed. While a benefit might make your temporary financial situation better, it might not be beneficial in the long term. However, those who need these provisions were created for are likely in immediate need to use the benefits until employment returns to normal.

Individuals:

Coronavirus-Related Retirement Distributions

Enhanced loans from employer retirement plans

Required Minimum Distributions waived for 2020

Qualified Charitable Contributions – NEW Above the line deduction

AGI Limit for Cash Charitable Contributions Limit Temporary Repealed

Miscellaneous Healthcare Benefits

Business Owners:

Paycheck Protection Program & Forgivable Loans

Wondering how this affects your future finances? Schedule a call with Financial Design Studio, financial advisors in Deer Park, to discuss your portfolio today.

VIEW MORE FROM FINANCIAL ADVISORS IN DEER PARK

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

![Fee Only Financial advisor Deer Park Barrington Chicago [Video] Financial Market Update- The Recovery Continues](https://financialdesignstudio.com/wp-content/uploads/2020/05/Fee-Only-Financial-advisor-Deer-Park-Barrington-Chicago-Video-Financial-Market-Update-The-Recovery-Continues-589x328.png)

Financial Market Update: The Recovery Continues [Video]

The expectations have picked up and unemployment continuing claims have come down quite a few million people. This 25 minute market update is for the week of June 1, 2020: Market & Economic Update EIDL & PPP Loan Details Tax Update (Business & Personal) FDS Resources Here are links to the resources mentioned in our…

State of the Stimulus

How has the coronavirus stimulus helped the economy? There are still funds to be deployed but a second stimulus package is likely needed.

Michelle Smalenberger, CFP®

I have a passion for helping others develop a path to financial success! Through different lenses on your financial picture, I want to help create solutions with you that are thoughtful of today and the future. I have seen in my life the power of having a financial plan while making slight changes of direction from time to time. I believe you can experience freedom from anxiety and even excitement when you know your finances are on track.