The Federal Budget Deficit and Fiscal Dominance

by Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer / May 20, 2024

There’s a debate happening in financial circles around the sustainability of the federal budget deficit. Hand-wringing about federal spending has been a hotly debated topic for decades. However, the conversation has taken a more serious tone as government debt has exploded higher and interest rates have increased. In short, the spending needs of the government have reached a level where they may “dominate” efforts by the Federal Reserve to conduct policy aimed at reducing inflation. Economists call this “fiscal dominance.” While we’re not seeing evidence of this dynamic yet, it’s good for us to know what fiscal dominance is and what it means to investors.

Why is the Federal Budget Deficit Suddenly an Issue?

The topic of runaway deficits and endless Congressional debt ceiling battles is nothing new. Many of us have become accustomed to ignoring these “crises” in recent decades. But two key things have happened that have pushed the issue to the forefront.

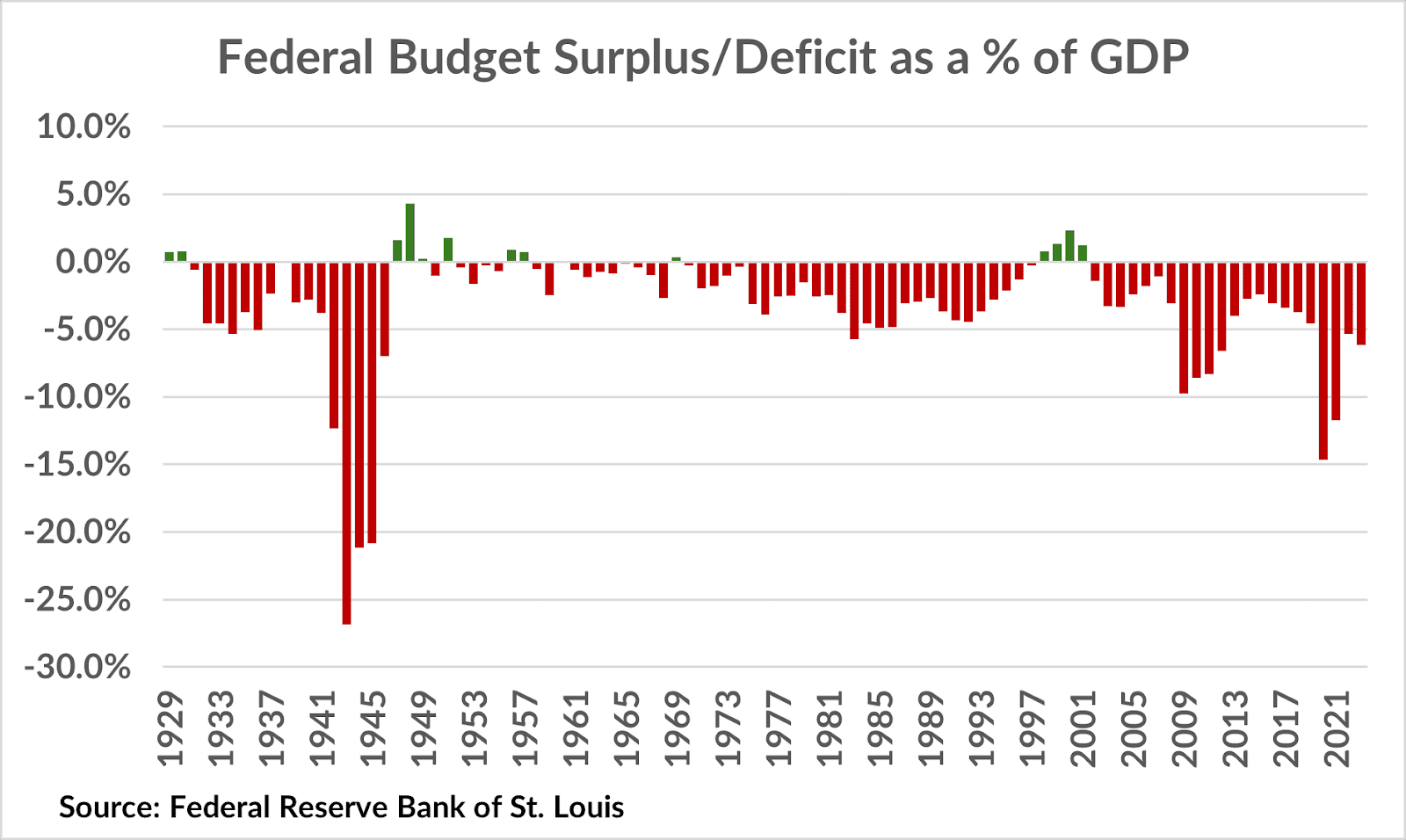

First, the spending blitz brought on by COVID was truly unprecedented by any measure. Going all the way back to 1929, the only time the federal government spent more money as a share of economic output (called “gross domestic product” or “GDP,” for short) was during WWII. For 2023, the deficit amounted to -6.2% of GDP. Only in the aftermath of the 2008 recession have we seen deficits that large in peacetime. Worryingly, we don’t think the deficit will improve much in the coming years.

Second, the steep rise in long-term interest rates from the extremely low levels in 2020-2021 had caused the amount of interest paid on government debt to rise significantly. Interest payments to service government debt are at an annual run rate of $1.1 trillion and surpass the cost of running Social Security or Medicare.

These two dynamics create a vicious cycle. As investors worry about high deficits, they demand a higher interest rate. That feeds into higher interest costs, which is a key contributor to the elevated deficits we see. The government quickly finds themselves in a no-win situation, needing to issue more debt to pay the interest costs on old debt!

Can the Government Realistically Cut Spending?

One obvious solution to breaking the cycle of deficits, debt, and interest payments is for Congress to cut spending. But it’s important to understand how difficult it is to put the spending genie back in the bottle. The reason it’s hard is that nearly two-thirds of annual government spending is on “mandatory” programs: Medicare and Social Security.

The (rising) cost of those programs is on autopilot, driven by higher healthcare costs (Medicare) and cost-of-living adjustments (Social Security). I say that spending is on “autopilot” as their costs increase naturally each year. For example, Social Security benefits increase each year for inflation. Worryingly, these costs cannot be cut without action by Congress and the President, which is highly unlikely in this political environment.

As mentioned, higher interest costs are eating up more of the budget; another 15% of total spending. And like mandatory spending, there’s not much the government can do to control that cost. They have to pay whatever the prevailing interest rate is for new debt.

Taken together, mandatory spending and interest costs account for 80% of government spending each year. The rest – discretionary spending – can be cut. But within this bucket lies defense spending. But that is highly unlikely to get cut given what’s going on with Russia & Ukraine, Israel & Palestine, and China.

Watch the Primary Budget Surplus

One budget indicator we are watching closely is what’s called the “primary deficit.” A primary deficit is nothing more than the total deficit minus interest payments. It focuses us on the core problem: too much spending on government services compared to the taxes that are brought in. The primary deficit is the blue line that’s circled below.

From the mid-1980s until the Great Recession of 2008, the primary surplus/deficit was close to 0% of GDP. The core budget was sustainable. That changed in the 2010s and we expect that to continue for at least the next decade. Interestingly enough, the last time the government was running persistent primary deficits was the 1970s. That was the last time inflation was a problem, just as it is today. We don’t think that’s a coincidence.

Fiscal Deficits Make the Fed’s Inflation Fight Harder

The Federal Reserve has been engaged in a furious fight against inflation since early 2022, raising rates from 0.25% to 5.50%. Hiking interest rates is traditionally the best way to fight inflation. This is because higher borrowing costs on mortgage and business & consumer debt causes the economy to slow down. This slowdown in consumption helps bring supply and demand dynamics into balance, which reduces pressure on prices.

There is one major downside, as we’ve seen above. Raising interest rates also raises the interest rate on the government’s own debt! Effectively, by raising interest rates to fight inflation, the Fed also causes the budget deficit to worsen. In fact, the average interest rate on government bonds has doubled from 1.60% at the end of 2021 to 3.22% as of March 2024.

When former Federal Reserve Chair Paul Volcker took charge in 1979, he declared that the inflation misery of the 1970s had to be dealt with once and for all. At the time he took over as Fed Chair, interest rates were already 10%. The problem was that inflation was also 10%, so monetary policy was not restrictive enough to combat inflation. Volcker eventually took interest rates to 20% in 1980. The cost of money was finally tight enough to slow down the economy and allow inflation to dissipate.

How was Volcker able to raise rates to 20% without blowing up the federal budget? Federal debt was much, much lower than where it is today. Total government debt outstanding as a percent of economic output (“GDP”) was just 31% when Volcker started hiking rates aggressively. Current Fed Chair Jerome Powell began hiking interest rates with a government debt burden 4 times larger than what Volcker dealt with.

What is Fiscal Dominance?

This brings us to the question, “What is fiscal dominance?” There’s debate about the exact definition, but our interpretation of this question is: fiscal dominance happens when the actions of fiscal policy (Congress & President) overwhelm the ability of the Federal Reserve to fight inflation using traditional monetary policy tools, such as managing interest rates. Effectively, fiscal policy takes over (i.e. dominates) the monetary policy.

To effectively combat the inflation problem we have today, the Fed needs to set real interest rates at a level that is sufficiently restrictive. A “real” interest rate is the current interest rate minus current inflation. If the real interest rate is positive, we say that is “restrictive.” This is because the cost of money is higher than the growth rate in wages, business profits, etc. Conversely, if the real interest rate is negative, we say that policy is “easy” because the wages and profits used to pay back debt are growing faster than the rate of interest they’re paying.

Today’s monetary policy is restrictive, but this follows a long period of very easy policy. Notably, we can see how restrictive monetary policy was in the 1980s as Volcker combated inflation from the 1970s.

Increased Risk of Fiscal Dominance from High Debt Levels

We could argue that a degree of fiscal dominance is already happening today. The current Federal Reserve cannot enact restrictive enough policy to fight inflation, as they did in the 80s. The reason? High government debt levels and the interest costs of servicing that debt quickly become a vicious circle as rates rise.

Think of a credit card. If you carry a $1,000 balance on your credit card and the card company doubles your interest rate from 10% to 20%, you’ll be annoyed by the higher interest cost but it likely won’t tip you into a cash flow crisis.

However, if you carried a $50,000 credit card balance and rates doubled to 20%, that would be an immediate problem to your cash flow! This is the exact problem the current Fed faces. They simply cannot create restrictive enough monetary policy to combat inflation without throwing government finances into a tailspin.

With inflation ticking up the last few months, the Fed suddenly finds itself in a tight box. They wanted to cut interest rates in 2024 to avoid tipping the economy into recession. But an emerging second “wave” of inflation makes rate cuts impossible without further fueling inflation. The most honest view of the Fed’s current policy is hope and prayer that inflation comes down of its own volition. Not a great spot to be, if you’re running the Fed.

Is the U.S. Experiencing Fiscal Dominance?

Based on what we’ve talked about thus far, it may seem clear that the U.S. is already experiencing fiscal dominance. But I don’t think we’re there yet.

Fiscal dominance will become clear when the government encounters difficulties raising cash to pay for the day-to-day functioning of government. These “difficulties” would most likely become apparent in the bond market. The Treasury Department regularly auctions new debt to investors, and those debt sales almost always get done without a problem. If investors grow uncomfortable with the fiscal outlook, they will demand the government pay a higher interest rate to compensate for the risk of higher future inflation. Worst case, investors will revolt and simply won’t buy a new bond issue, causing a “failure” of an auction.

We haven’t yet seen any signs that bond market investors are ready to revolt. Demand for bonds is still very good, particularly as interest rates have risen to more reasonable levels. Big pension funds with a mandate to generate annual investment returns of 7% are very comfortable owning more bonds. They can get 5% from “risk-free” government bonds, compared to 1-2% just a few years ago.

We don’t know when true fiscal dominance may happen. But with large (and increasing) budget deficits and already-high government debt levels, the risks for such a scenario are higher than they’ve ever been. The political dysfunction we’ve seen in recent years doesn’t provide any comfort that there’s an “adult in the room” anywhere in Washington, D.C.

How Can the U.S. Avoid Fiscal Dominance?

The cleanest way for the U.S. to deal with the threat of fiscal dominance is to get its budget in order. That would mean getting the primary fiscal deficit mentioned above back towards 0% of GDP. As a reminder, Social Security, Medicare, Defense, and other discretionary spending drives the primary surplus or deficit.

Sounds easy enough, but reforming either Social Security or Medicare, or cutting defense spending is a huge hurdle in today’s political climate. But it’s not an impossible task. Ironically enough, the last time the government reformed Social Security was in 1983, at the very moment they were grappling with high inflation and rising budget deficits. Those reforms increased the retirement age from 65 to 67, amongst other measures to shore up the program.

What About Social Security?

There is a ticking time clock whereby Social Security will “run out” of money in 10 years. As mentioned in a recent podcast we did on Social Security, we are NOT in the camp that Congress will allow Social Security to cut benefits. But the timing of the coming Social Security “crisis” lines up well with the increasingly urgent need for the government to get its finances on sustainable footing.

We fully expect the topic of shoring up Social Security to become a dominant theme, possibly as soon as the 2024 election cycle. The problem has to be dealt with. There are a million ways to fix the problem; most likely lifting Social Security wage limits so higher-income earners pay more into the system.

Another way to keep fiscal dominance at bay would be if the economy tipped into a recession, alleviating upward pressure on wages and profits. This obviously isn’t an ideal outcome, and I’m not even sure a recession would help. The COVID experience introduced several budget-unfriendly ways to deal with a recession: stimulus checks sent to taxpayers, higher child tax credits, higher unemployment benefits, and loan forbearance measures. Arguably, we are in a fiscal dominance predicament precisely because of these spending measures.

Investment Strategy During Fiscal Dominance

While I don’t think we’re in fiscal dominance, it is an emerging risk that investors have not had to deal with before. We’ve managed client investments in recent years with an eye towards the 1970s inflationary experience. What’s new this time around is the federal budget situation, which didn’t exist in the 70s.

One obvious asset class that should do okay in a fiscal dominance regime is inflation-linked bonds. In such a regime, inflation is clearly a problem, so it warrants owning bonds that are immune from inflation’s effects. We recently increased the weight of inflation-linked bonds in client portfolios.

Another asset class that would likely do well is commodities. Precious metals such as gold and silver along with other scarce commodities, such as oil and copper would likely see price increases. In fact, gold recently broke out of a 12-year holding pattern, with silver also breaking out. This could be an early sign that the market is sniffing out a fiscal dominance problem.

Finally, one asset class may do well (for a time) that isn’t logical: U.S. Stocks. This is a highly speculative view. The logic here is that if we look at other historical instances where a government lost the fiscal dominance battle, inflation surged but stocks also surged. Why would that happen? Stocks are a function of company sales and earnings, and if inflation is high, then these companies will see the nominal value of their sales go up. Inflation is “prices going up” and companies largely control the prices we see. Essentially, U.S. companies “pass through” inflation.

How will U.S. Stocks Perform?

Many investors, including yours truly, have wondered how U.S. stocks can be near all-time highs even as inflation is a problem and interest rates have increased so much. One answer is that companies have been able to pass price increases along, preserving their profit margins. Inflation driven sales and profits will drive stock prices higher, assuming valuations remain constant.

We’re uncertain stocks would work well in such a regime, however. The wildcard is unemployment. If people are employed – as they are today – it’s easier for companies to pass along price increases. However, the experience of the 1970s showed stocks struggled for many years. At the same time unemployment steadily increased, hurting profits and stock valuations.

Keys to Know About Fiscal Dominance

As mentioned at the outset, the point of penning this piece is to put “fiscal dominance” on your radar. The government is spending money like never before. And higher interest rates are causing a surge in interest costs on government debt, worsening the budget outlook.

We don’t think the U.S. is experiencing fiscal dominance – yet. But we are closely watching the trajectory of the primary federal budget deficit. We are monitoring government bond auctions for any signs that buyers of government debt are tapped out.

The main takeaway I’d like everyone to get from this is that the potential for fiscal dominance introduces an unknown risk to investors. One that none of us has had to think about in our lifetimes. If you’re an investor that’s ever worried about the debasement of the dollar (i.e. rapid devaluation) then fiscal dominance would be a trigger for such a scenario. We wrote an article called, “Is the Dollar Going Away,” which you can read if you have more questions.

We incorporate these views into how we manage client portfolios. Markets change every day, and as prices change, we constantly reassess where emerging opportunities and risks are. As my old boss used to say, “If it’s news to you, it isn’t news.” A consistent investment framework endeavors to anticipate what’s coming, not reacting to what happens. You can read more about our wealth management process here! We at FDS are your guide to make sure your investments are managed effectively so you’re confident that you’re on-track to reach your goals.

Ready to take the next step?

Schedule a quick call with our financial advisors.