Leaving a Legacy by Thinking Two Generations Deep

by Financial Design Studio, Inc. / September 5, 2025

Five generations. That’s the number of familial generations we will probably know well in our lifetimes. Beyond our own generation, we will know our parent’s generation, our grandparents, and lucky folks may also know their great grandparents. Looking past our generation, we have our kid’s generation and their kids – our grandchildren.

As people age into retirement, a common question that comes up is, “How will people remember me/us?” The sobering reality is that beyond our grandkids, we likely won’t be remembered at all. But we have the opportunity and the finances to affect the two generations below us in ways that will last the rest of their lives and possibly get passed down to future generations we won’t ever know. That’s called leaving a legacy. As we discuss regularly with clients in and near retirement, it’s good to think two generations deep when thinking about our final stage of life. But how can we do that? This article aims to give you a place to start when thinking two generations deep.

Give it Away Now or Give it Away Later?

Looking back through American history, generations have agreed to the idea of waiting until the end of their life to pass on assets to kids and grandkids. If you look back at the trajectory of American life expectancy over the last 100 years, this was the correct course of action. People in 1925 expected to live into their mid-50s. Hence, any assets passed on to their kids happened when their kids were in the early stages of building their own families.

But things have changed dramatically. Today, people are living into their 80s and beyond. And by the time they pass away, their children are already half-way or more through raising their own kids. This has introduced a new way of thinking about passing on a legacy: “Can giving away assets before we pass away have a greater impact on our children and grandchildren versus waiting until we’re gone?”

Now having strong estate plans in place for when you pass away is crucial to taking care of your family. With the correct documents in place, you can help your beneficiaries avoid fights and ensure your wishes are carried out. But how much more impactful is it to be apart of the process of giving away your finances and seeing the impact during your lifetime?

Given the heading of this section – “Give it away now or give it away later?” – you may expect us to provide a firm answer. But we can’t. Each family’s view of when is the best time to pass on assets is as varied as our views about whether it’s appropriate to put pineapple on pizza or not. There is no “right answer.” Our purpose here is to convey the idea that things have indeed changed. What was a “norm” a generation or two ago is no longer the norm today. So what does it look like to give money away today?

How has the Cost of Education Impacted Families?

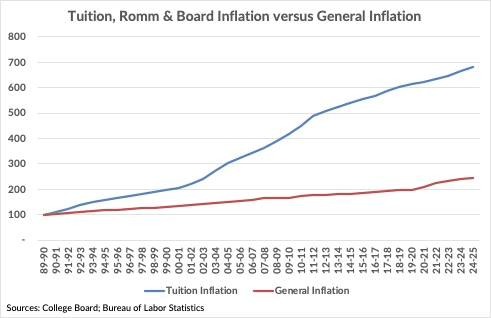

We will begin by looking at two key factors that are affecting young families today. The first is the cost of education, namely college tuition. Since 1990, the inflation rate for college tuition, room & board has increased at nearly three times the rate of general inflation. This has had a severe impact on affordability for families.

I’ll share my experience as a real world example. In the 1993-1994 school year, I worked summers and weekends making about $4.50/hour. Working full time for 15 summer weeks, I could scrape together about $2,200. The total cost of tuition, room and board at the University of Wisconsin Madison – where I went to school – was $5,200/year. Meaning, by working summers plus some weekends and winter break, I could have enough to pay for about 50% of my tuition bill.

Today, the cost of in-state tuition at Madison is now $31,000/year. A same student working summers and making $15/hour could accumulate about $7,200. That, plus working some weekends and winter break would be enough to cover about 30% of current tuition costs. Leaving over $20,000 per year (for four years) that would need to be financed or paid for by parents.

Multiplying this family’s dilemma over 2, 3, or 4 children and we can see the burden that families face in wanting to send their children to college.

Benefits of Grandparent 529 College Savings Accounts

Grandparents can step into this void to support their children and grandchildren. One great way to help pay for college is by contributing regularly to a 529 college savings account. There are several benefits for grandparents to do so:

- The grandparents are owners of the account, giving maximum flexibility to have those funds used as they see fit.

- Many states will offer a break on state income taxes for contributions made to a 529 planned opened in the state the grandparents live in.

- Grandparents often have the financial capacity to save into a 529 when the grandchild is born, reducing the need to contribute large sums each year as money has time to be invested and grow.

- 529 savings can be used for the benefit of a grandchild’s education at any time they are in college, or even in K-12 school.

We’ve seen with our own clients that opening 529 college savings plans has become a popular option to give money to future generations while they’re still living. Some even do so without telling their own children (parents of grandchildren,) wanting to make sure their children don’t rely too much on them to pay for college. No matter how one does it, helping grandchildren pay for future educational needs is a great way to make a tangible impact while you’re still living.

How to Help Grandchildren Own a First Home

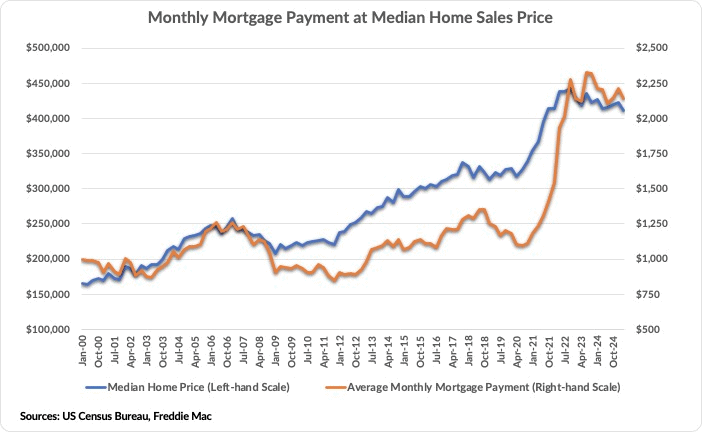

Another big change in American society over the last few decades is the cost of buying and owning a home. Home prices have surged in recent years while mortgage rates have risen to their highest levels in 20 years. The combination of these two factors has significantly increased the cost of having a mortgage.

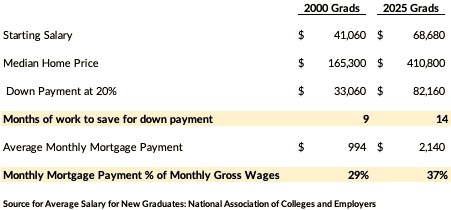

By comparing the starting wages for recent college graduates for those who graduated in 2000 versus those who just graduated in 2025, we can see how housing has become an issue.

Compared to graduates 25 years ago, it takes 50% longer for a 2025 graduate to save for a down payment and their monthly mortgage payment eats up a higher percentage of their income. Remember, bank rules make it hard to get a mortgage if debt payments as a percent of gross wages are over 43%. Since recent graduates are leaving school with more student loan payments compared to 2000 graduates, many current graduates aren’t even able to qualify for a mortgage.

It’s unrealistic to ask grandparents to take on the housing costs of their grandchildren. Nor is it advisable to co-sign a mortgage so they can qualify. But a grandparent could help with a one-time gift towards the down payment of their grandchild’s first home. The bigger the down payment, the lower the monthly mortgage payment, which could help many young people qualify for a mortgage.

Strengthening Family Bonds: Your Purpose & Legacy

The two issues we’ve discussed above are real, tangible issues that our grandkids are dealing with today. By supporting them in achieving their educational and home ownership dreams, you can strengthen emotional bonds with your grandkids. Your gifts provide real purpose and legacy towards helping these future generations.

There’s also the benefit of setting a generous example for future generations. As mentioned at the outset, the idea of giving assets away before one’s death is a relatively new concept. Not surprisingly, our society is struggling with this reality, resulting in a lot of back-and-forth between older and younger generations. By generously providing support for grandchildren while you’re still alive, you’re setting an example for them to follow when they have their own kids and grandkids. Put another way, you can set a new example of generosity today, which will last for generations to come. That’s what we call leaving a legacy.

Giving Beyond the Family: Qualified Charitable Distributions

Another way to give during your lifetime that can affect future generations is to start routinely giving to charities in retirement. As financial planners, we spend the vast majority of our time with clients nearing retirement making sure they have enough resources to sustain themselves throughout retirement. This can sometimes limit the conversation to “How are we doing?” versus “What can we do?”

Financial planning realities often lead us to look for ways to help clients save on taxes. One planning issue our clients face is future Required Minimum Distributions (“RMDs”) that will be sizably higher than projected cash flow needs. This can lead to unnecessary tax burdens in the future. Roth conversions in retirement are one way to deal with this issue, but there’s also a charitable giving strategy that can help.

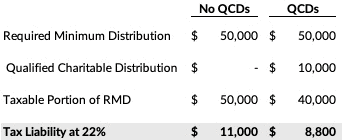

Qualified Charitable Distributions – or “QCDs” for short – are available to retirees who are at least 70-½ years of age. QCDs refer to the ability to give to charity direction from pre-tax IRAs without those donations counting as taxable income. This can be a powerful strategy for charitable-minded people facing high RMDs.

The benefit of doing QCDs is that the IRS lets you use those amounts against your annual RMD. This lowers the taxable portion of your RMD, which reduces the taxes you owe.

While this makes for a nice tax-saving strategy, there’s the added benefit of supporting organizations that are important to you. And doing so while you’re alive helps you see those organizations impact the communities they support.

Leaving a Legacy by Thinking Two Generations Deep

Statistics show that anyone that makes it to age 60 can expect to live for another 22-25 years. That’s a long time to spend doing the things you like to do, such as travel and spending time with family. But it also represents a tremendous opportunity to impact future generations.

We’ve shown here how grandparents can make a lasting, positive impact on their grandchildren but supporting them in two “struggle” areas they face: paying for college and buying their first home. This is obviously a delicate conversation, however. While we want to be supportive of our kids and grandkids, we don’t want to become a crutch to them; they have to learn how to fend for themselves.

But by virtue of longer life expectancy, the current generation of grandparents have a unique opportunity. Grandparents can both support future generations and set a good example that will last longer than people’s memory of our lives. And this opportunity extends beyond family, but to churches and charitable organizations that depend on the support of generous people. The memory of who we are will fade over time, but we can make an impact today that will last for generations to come.

At Financial Design Studio, we help corporate executives and directors not only prepare for their own retirement, but to look beyond retirement for ways to make a lasting impact. Are you wondering if you’re ready for retirement? Please hit the “Get Started” button at the top of the home page to begin the conversation!

Bonus: Retirement Planning Guide

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

Outlook for Interest Rates and the Budget Deficit

Explore the link between interest rates and the U.S. budget deficit, and how the Iran War and the Fed are impacting stock and bond markets

How to Plan for Deferred Compensation in Retirement [Video]

In this video, we share how to plan for deferred compensation as it impacts your income and taxes in retirement.

Financial Design Studio, Inc.

We are financial advisors in Deer Park and Barrington, IL. A team with a passion for helping others design a path to financial success — whatever success means for you. Each of our unique insights fit together to create broad expertise, complete roadmaps, and creative solutions. We have seen the power of having a financial plan, and adjusting that plan to life. The result? Freedom from worrying about the future so you can enjoy today.