Does Investment Diversification Matter Anymore?

by Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer / October 25, 2023

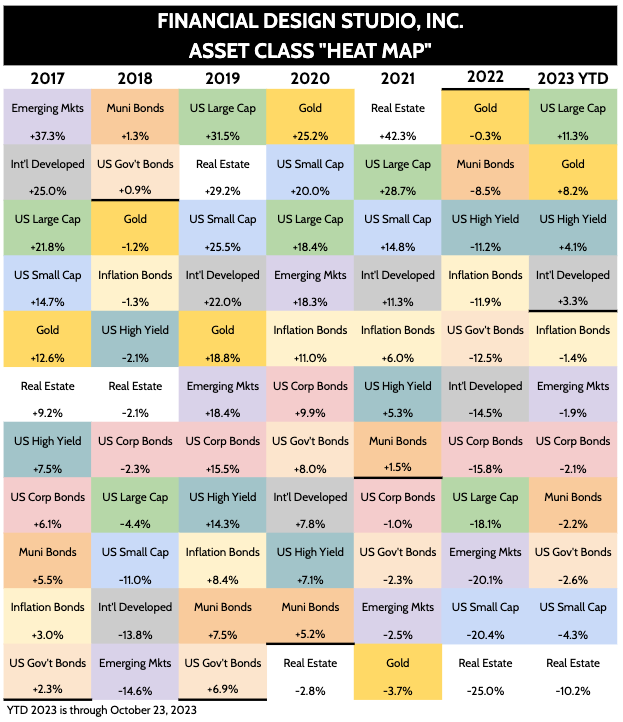

2023 is shaping up to be another challenging year for diversified investors. Using the word “diversified” is intentional as we are in a period when being a well-diversified investor has led to underperformance. Has the idea of being well-diversified run its course? As investors, we have to remain conscious of whether nice-sounding rules of thumb become dogmas without intellectual reasoning behind them. This article will first look at year-to-date returns for the main asset classes we track. Then, we’ll challenge the idea whether investors still warrant investment diversification in this day and age. Does investment diversification matter anymore?

Asset Class Returns in 2023

As recently as June, it was shaping up to be a pretty good year for investors. Both stocks and bonds were showing positive performance. This was a relief after 2022’s performance, which saw both stocks and bonds deliver negative double-digit returns.

Since June, the performance of many asset classes has lagged, particularly for bonds. At the high point for the year, the Bloomberg Aggregate Bond index was +4.5% for 2023. Now, it’s -2.7%, as long-term interest rates have continued to move higher.

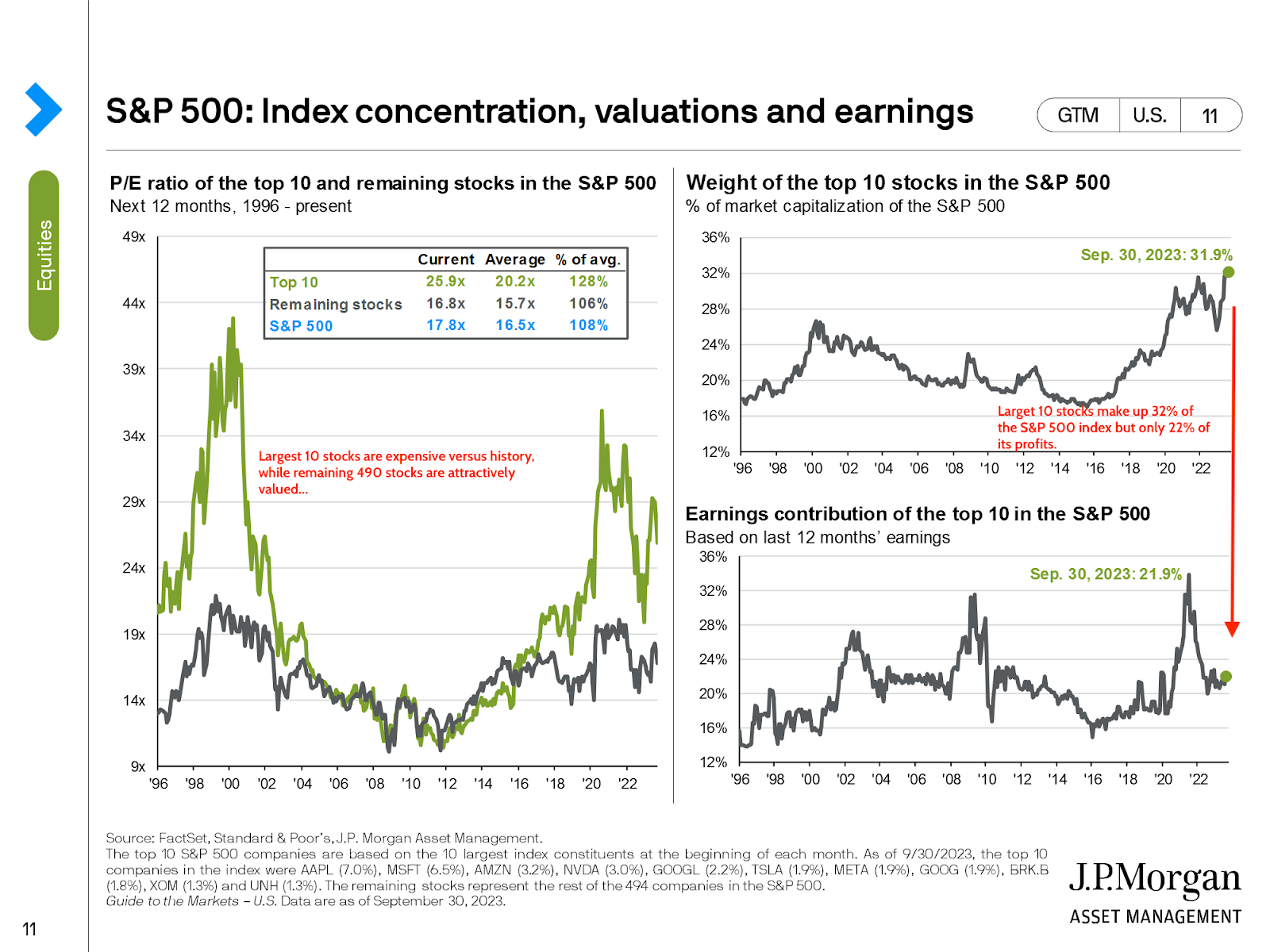

On the stocks side of the ledger, the only styles of stocks that are higher are large-cap US stocks and international stocks in developed countries. All other styles, from small-cap stocks to emerging markets, are down on the year. In fact, the stock “rally” has been quite narrow, heavily concentrated in the 10 largest stocks in the S&P 500 index.

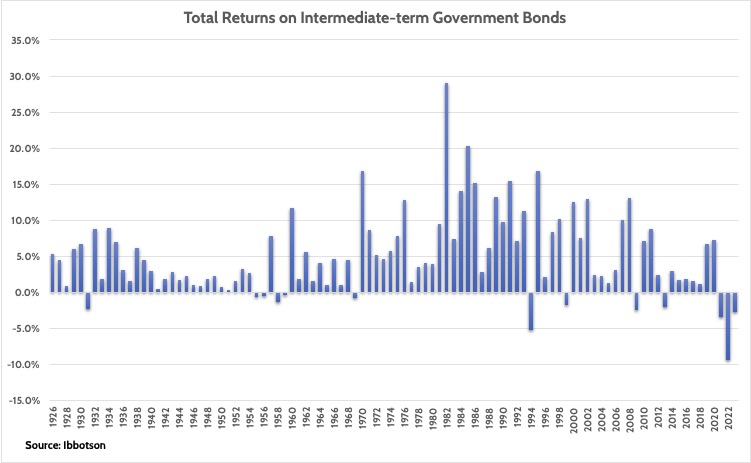

The biggest disappointment for investors has to be the negative return in bonds. Unless bonds stage a late-year rally, they are poised to deliver negative total returns for the third year in a row, which would be the first 3-year losing streak since 1926. I’ll speak more on this below, but 2024 should prove better for bond investors, for no other reason that we’re now getting 5%+ yields on high-quality bonds.

Very Narrow Stock Market Performance in 2023

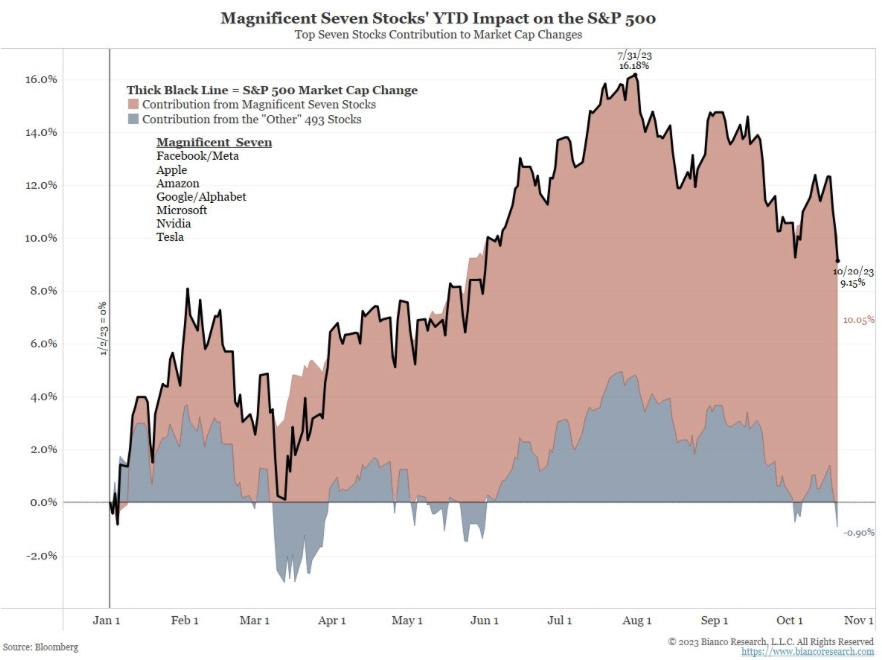

One of the key reasons diversified investors – including clients of FDS – have experienced a performance lag this year is because of the narrowness of the stock market rally. As economic uncertainty increased throughout the year – coupled with bank failures in March – investors gravitated towards the largest of the largest stocks in the S&P 500 index.

The chart below, from economist Jim Bianco at Bianco Research – highlights how narrow the rally has been in the S&P 500. Excluding what he calls the “Magnificent 7” – which are Apple, Microsoft, Google, Facebook, Amazon, Nvidia, and Tesla – the other 493 stocks in the index are actually down slightly in 2023.

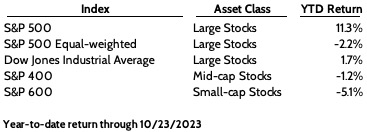

Narrow performance goes beyond the large company S&P 500 index. Medium-sized companies, small company stocks – even the venerable Dow Jones Industrial Average – are flat to down this year.

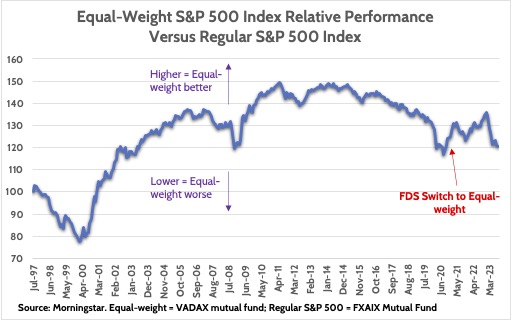

For FDS clients, the most problematic performance “contributor” has been our holding of the equal-weight S&P 500 index. It has lagged the normal S&P 500 badly this year after outperforming the regular S&P 500 by 6% in 2022. The catalyst for this underperformance was the bank failures in March. Banks are a heavier component of the equal-weight index versus the regular index, which is dominated by technology stocks, including the Magnificent 7.

We believe that the reasons to switch to the equal-weight index remain valid. The S&P 500 index remains very concentrated, where just 10 stocks make up almost one-third of the index value. Further, the valuation of those top 10 stocks is higher than what their earnings suggest they should be.

Is the Bear Market in Bonds Over Yet?

The performance of stocks gets the most attention from investors, but the biggest story the last 24 months has been the historic bear market in bonds. Not only are bonds on track to deliver their third year of negative performance, but the scale of the downdraft has been large, with bonds falling about -15% since the end of 2021.

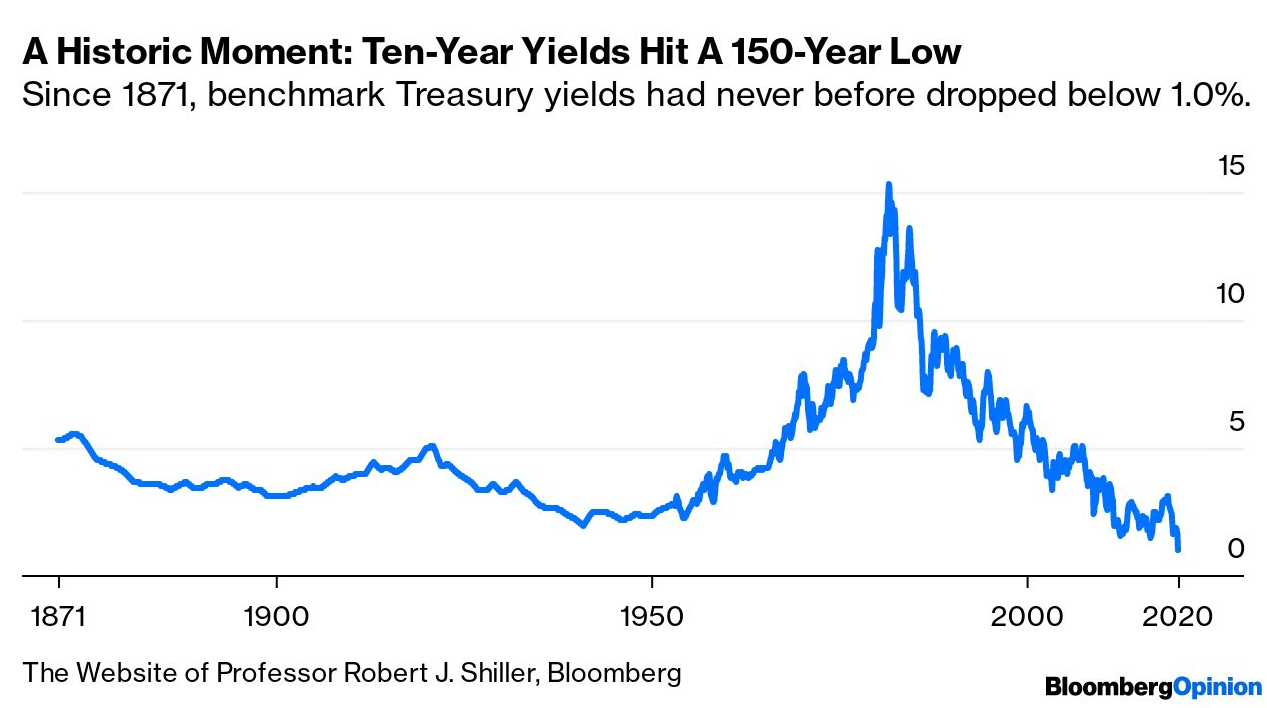

For retirees who count on bonds to provide stable returns and a decent yield, this negative performance has been a bitter pill to swallow. The key reason returns have been so bad is that the Fed pushed bond yields to extremely low levels during COVID. This is a chart I shared in 2020 showing how low bond yields got compared to history.

When bond yields rise from very low levels, there’s an outsized negative response to bond prices. This is called “duration.” In the Spring of 2021 we changed the bond portfolios of FDS clients to help shield them from the risk of rising interest rates. These moves didn’t completely insulate clients from negative bond returns, but offset some of the impact.

Are Bonds Attractive Investments for 2024?

During the Summer of 2023, we brought client’s interest rate risk back to “neutral.” This turned out to be premature, but we’re comfortable with the move because investors are getting very attractive yields on high-quality bonds for the first time in over a decade.

For example, you can buy bonds in Warren Buffett’s Berkshire Hathaway today and earn a yield of 5.8% for each of the next 20 years. A 30-year US Treasury bond yields just over 5%. As we extended bond duration over the summer, we allocated more to these high-quality corporate bonds.

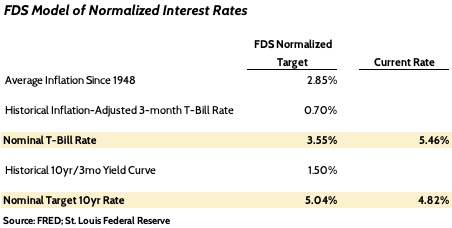

I believe there’s a strong case to be made that interest rates have peaked for this cycle. Inflation is falling back towards normal levels. We have a model what interest rates “should” be in a normal inflation environment, looking at the historical relationship between interest rates and inflation. Our model is below.

We believe the short-term rates set by the Federal Reserve are 2% higher than normal. This gives the Fed room to cut rates, as we continue to expect a recession or economic slowdown soon. But we don’t expect rates to go back to 0% – if ever in our lifetimes – as that policy created distortions that are proving very hard to reverse.

10-year government bond yields recently touched 5% for the first time since 2007. Based on our model, I believe government bond yields are close to fair value.

What does this mean for investors? If medium and long-term rates hold steady at these levels, investors will earn close to 5% by “clipping the coupon” on the bonds they own. But if our thesis of economic softness (finally) plays out, then there could be price appreciation on bonds that boost returns further. Either way, the negative price impact of a continued rise in interest rates is significantly less than what it was two years ago.

Has Investment Diversification Worked?

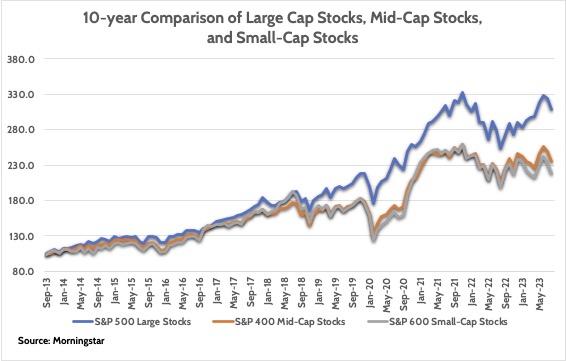

Now, we move on to a very important question: Does it still make sense for investors to diversify their investments? Investors are right to ask this question. Since 2017, large-cap stock performance (Below: blue line) has dominated any other type of stock investment, whether it’s small company stocks in the U.S. or international stocks.

We can excuse investors for believing that diversification doesn’t help anymore. Since 2017, they’ve gotten 10% annualized returns from the large cap S&P 500 index, 5% returns from the mid-cap S&P 400 index, and 4% returns from small-caps.

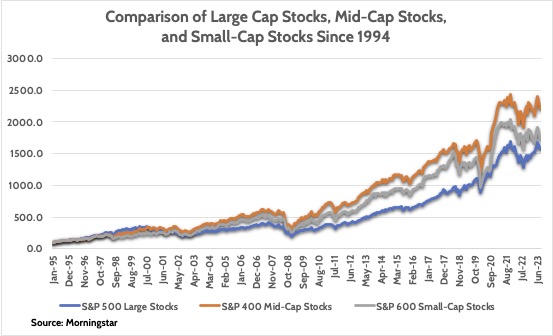

However, if we look at a full history of data that we have – going back to 1994 – we can see that large-cap stocks haven’t always been the winners. This is a valid historical period to look at. It includes the internet bubble in the late 1990s, which sent large-cap stocks soaring. It includes the subsequent bursting of that bubble in 2001-2003. The housing bubble and Great Recession are included, as is the COVID downturn of 2020.

Most of our clients – even ones in retirement – don’t have a 5 year time horizon. We measure their time horizon in decades. So taking a long-term view of diversification is important.

What’s the Practical Benefit of Having a Diversified Investment Portfolio?

Our view has always been that the key benefit to investment diversification is that it helps smooth out returns and avoid extended periods of underperformance. But does this belief hold any water?

Many investors – including me – can get fixated on short-term investment performance. “Man, that index has done nothing this year…let’s get out and try this other one that’s done great.” But we remember that we’re investing for long-term goals that could be decades into the future. So we have to think long term.

To test whether there are benefits to investment diversification, we’re going to run an example of a Diversified Investor versus the S&P 500 Investor. The S&P 500 investor only invests in that index. The Diversified Investor invests in all 3 major U.S. stock indices as follows:

- ⅓ in S&P 500 index (large company stocks)

- ⅓ in S&P 400 index (mid-caps)

- ⅓ in S&P 600 index (small-caps)

Using monthly performance data for these indices since 1994, we’ve constructed 3 “rolling” performance periods: 3-year, 5-year, and 10-year periods. For example, the current 3-year rolling return of the S&P 500 index would capture the index’s return from September 2020 to September 2023.

We’ll first look at the table and then I’ll comment on important observations below it.

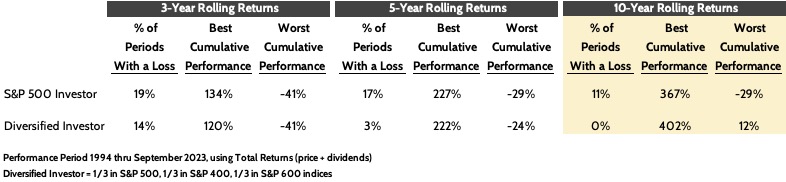

Key observations:

- On a 3-year basis, it has made little difference to be diversified or not. Best and worst returns between the two investors are similar, as have been the chances of experiencing a loss.

- 5-year rolling returns are also similar between the two investors, but the S&P 500 investor has experienced a loss more frequently than the Diversified Investor (17% vs. 3%).

- Long-term, Diversified, 10+ year Investors, have clearly been better off compared to the S&P 500 Investor.

- Diversified Investor suffered no 10-year period of negative returns

- Diversified Investor’s best 10-year period was better than the S&P 500 Investor

- The S&P 500 Investor’s worst 10-year period saw -29% total returns, while the worst 10-year period for the Diversified Investor was +12%.

Investment Diversification helps long-term investors avoid catastrophic periods of underperformance. When we build client plans, we assume long-term investment returns of +6.5% per year. Within that assumption is the assumption that stocks generate average returns of +9-10% per year. That’s supported by 100 years of historical data.

A long-term investor can overcome a 3-year or even 5-year period of negative performance. But suffering a 10-year period of negative performance – as the S&P 500 Investor did – is hard to overcome.

Make no mistake: the worst case 10-year total return of 12% for the Diversified Investor (+1.1%/year for 10 years) is a terrible outcome. But it’s a far cry from losing an average of -3.3% per year for 10 years as was the case for the S&P 500 index from February 1999 to February 2009.

Investment Diversification is About Risk Management

There are two things we need to understand about investing. First, we have very long-term historical evidence that investing in stocks generates investment returns well-above the rate of inflation. That’s why we invest. We not only want to protect the purchasing power of your future dollars, but enhance that power.

Second, the key to investment success is staying disciplined. I’ve worked with and know a lot of extremely smart investors and traders. Some do well, many don’t. We can look to the example of Warren Buffett, who makes an investment and sticks with it for years – sometime decades – at a time. I can’t recall him ever making a “trade” with the idea that it’s a short-term play on whatever fad stock is popular.

For long-term investors – which include all FDS clients young and old – investment diversification has a proven track record helping people avoid protracted periods of poor performance. It reduces the risk of having to re-boot a client’s financial plan, which might include less spending in retirement or fewer vacations.

Diversification does NOT eliminate the risk of long stretches of below-average returns. Investors in the 1970s and 2000s found that out the hard way. With investing, there are no guarantees.

Does Investment Diversification Matter Anymore?

Our answer to this question is a definitive “yes,” based on the evidence shown above. That said, I’m sympathetic to the feelings of “missing out” on whatever the hot investment trend of the day is, whether it’s cryptocurrencies like 2020-2021 or artificial intelligence stocks in 2023.

We focus on doing the very un-sexy things that we think deliver long-term value for clients. That includes staying invested in a core, diversified portfolio of stocks and bonds. Making sure there’s a discipline rebalancing process in place to take advantage of the market’s ups and downs with as little emotion as possible. Keeping investment expenses as low. And always monitoring taxes, which are a silent killer of long-term investment returns.

Never underestimate the power of a disciplined investment process. As your financial advisor, we come up with many strategies to help you make the most out of your financial resources. Doing Roth conversions, choosing employee benefits, exercising stock options and restricted stock for executives, Social Security timing, Medicare planning, and making smart choices when buying a home, to name a few. But if there’s a failure in the investment process, it can negate the benefits of these strategies.

For ongoing clients, I can confidently say that the real value we provide to you is that we’re always making sure you’re doing the things we recommend you do. It’s very easy to forget about doing a Backdoor Roth conversion. Or increasing your 401(k) and HSA contributions as the IRS lifts maximum contribution limits each year. Or boosting tax savings by making timely contributions to a Donor Advised Fund. All the while, keeping you fully invested in a well-diversified investment portfolio. We’re all busy people and have better things to worry about; you pay us to make sure you’re getting these things done, consistently.

Ready to take the next step?

Schedule a quick call with our financial advisors.