How to do a Backdoor Roth IRA Contribution

by Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer / September 16, 2022

People and families with high income often feel like they’re not able to save enough for retirement. Maxing out one’s 401(k) is a great start, but how do you save money beyond that? And due to income limits, you may not be able to contribute directly into a Roth IRA. Is there still a way to save money into a Roth IRA even if your income exceeds the thresholds? The answer is YES, through a Backdoor Roth IRA Contribution. This post will walk you through the benefits of saving money into a Roth IRA, and how to do a Backdoor Roth IRA Contribution.

What’s the Benefit of Putting Money in a Roth IRA?

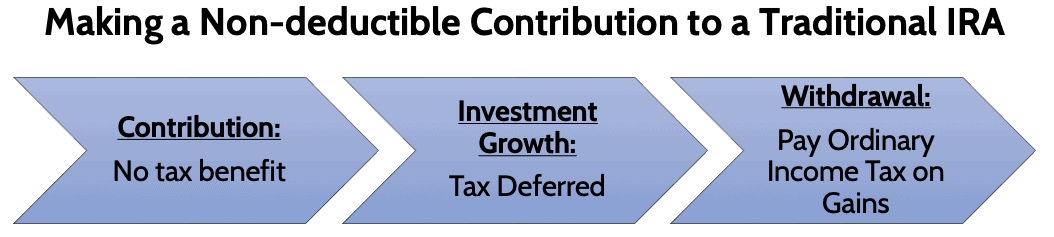

A natural question is why you’d want to get money into a Roth IRA. It mainly boils down to taxes. As a high-income earner, you can’t contribute directly to a Roth IRA, but you can contribute to a Traditional IRA. The downside with contributing to a Traditional IRA as a high-income earner is that you won’t get a tax deduction for that contribution if you’re already covered by a retirement plan at work. These are called “non-deductible” Traditional IRA contributions.

In the old days, making a non-deductible contribution to a Traditional IRA was a “better than nothing” approach to saving more money for retirement. While you don’t get a tax deduction today, your investments can at least grow tax deferred. The downside, however, is that you’re taxed on those investment gains when you pull money out of the IRA.

The appeal of the Roth IRA is what happens in the withdrawal stage. Just like a non-deductible Traditional IRA contribution, you don’t get any tax benefit for the contribution. And you don’t have to pay taxes on gains while your investments are growing. However, when you pull money out in retirement, you don’t pay taxes on any of the money you pull out!

A Backdoor Roth IRA Contribution helps high income earners get the benefits of a Roth IRA contribution even though they can’t directly contribute to a Roth IRA. Let’s see how.

Who’s the Ideal Candidate for a Backdoor Roth IRA Contribution?

Technically, anyone can do a Backdoor Roth IRA. But, this strategy is primarily for people whose high income prevents them from directly contributing to a Roth IRA. Here are the characteristics of the best candidates for a Backdoor Roth Conversion:

- Single tax filer making more than $144,000 per year (2022)

- Married tax filer making more than $214,000 per year (2022)

- You’re already maxing out your 401(k)

- You don’t have money already sitting in a Traditional IRA

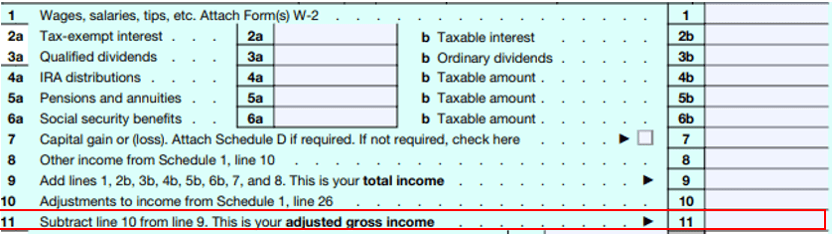

The income the IRS looks at is called the Modified Adjusted Gross Income, or “MAGI” for short. For the vast majority of taxpayers, Modified Adjusted Gross Income is equal to Adjusted Gross Income (“AGI”), which is found on Line 11 of your tax return. Once MAGI/AGI is above the amounts referenced above, you’re not allowed to put money into a Roth IRA.

The ideal Backdoor Roth Conversion candidate is also maxing out their 401(k). Why? Because it’s the one savings vehicle, you have that allows you to put a lot of money into ($20,500 in 2022) and does not have income limits. So while the IRS says you can’t contribute to a Roth IRA if your income is too high, you can contribute to a Roth 401(k) regardless of how much you make. That’s why we recommend doing a Backdoor Roth IRA contribution only after you’re maxing out your other options.

Finally, it’s critical that you don’t already have money saved in a Traditional IRA. We’ll get into the reason later in the article (see IRS Pro-rata Rule), but the key reason is that the IRS will tax part of your Roth Conversion. That defeats the purpose of doing a Backdoor Roth Conversion in the first place!

How to do a Backdoor Roth IRA Contribution

The mechanics of doing a Backdoor Roth IRA contribution are relatively straightforward. There are just four steps you have to take. To get started, you’re going to need to open a:

- Traditional IRA account with zero balance

- Roth IRA account

We recommend getting these two accounts at the same bank or custodian. For example, if you like Schwab, you’d open both IRAs at Schwab. The reason we recommend having the accounts at the same place is that it makes the conversion from Traditional to Roth much smoother.

Once you have those accounts, here’s what you need to do.

Step 1: Make a non-deductible contribution to your Traditional IRA. Most big savers aim to “max out” their IRA contributions each year. That would mean a contribution of $6,000 in 2022, or $7,000 if you’re Age 50 or over.

Step 2: Wait one or two business days. The reason to wait a couple of days is that the contribution from your bank to the Traditional IRA usually needs 1-2 days to fully settle at the custodian.

Step 3: Convert your Traditional IRA contribution to your Roth IRA. Many custodians allow you to do this online now, otherwise you may have to call. Remember, because you started with a Traditional IRA balance of ZERO, you’ll also end up with a zero balance in your Traditional IRA after converting it to the Roth IRA.

Step 4: When you file your taxes for the year, you’ll want to make sure you fill out IRS form 8606. This alerts the IRS to the fact you made a non-deductible contribution to your Traditional IRA, this establishing basis making the conversion tax-free and helps to avoid any confusion in the future.

Those are the steps you need to take from beginning to end!

Other Things to Know about Backdoor Roth IRA Contributions

The “who” and “how” of Backdoor Roth IRA contributions is straightforward. But there are two other things to keep in mind if you’re looking to pursue this strategy.

First, if you’re married and your combined income prohibits you from contributing to a Roth IRA, you BOTH can do a Backdoor Roth IRA contribution. Essentially, you’d follow the same 4 steps above, but each spouse would do their own Backdoor Roth contributions. That way a married couple can save twice as much with this strategy.

Second, you must do a Backdoor Roth IRA contribution before December 31st of the current tax year. Many people get confused by this because the IRS allows you to make IRA contributions for a tax year until April 15th of the following year. But to get credit for a conversion in a particular tax year, the conversion must happen before December 31st of the tax year.

Backdoor Roth IRA and the IRS Pro-rata Rule

We’ve mentioned that a Backdoor Roth IRA contribution strategy only works if you have no money in a Traditional IRA already. The reason is that the IRS has a rule called the “Pro-rata Rule.” The best way to explain the rule without getting into the weeds is to show an example of how it works.

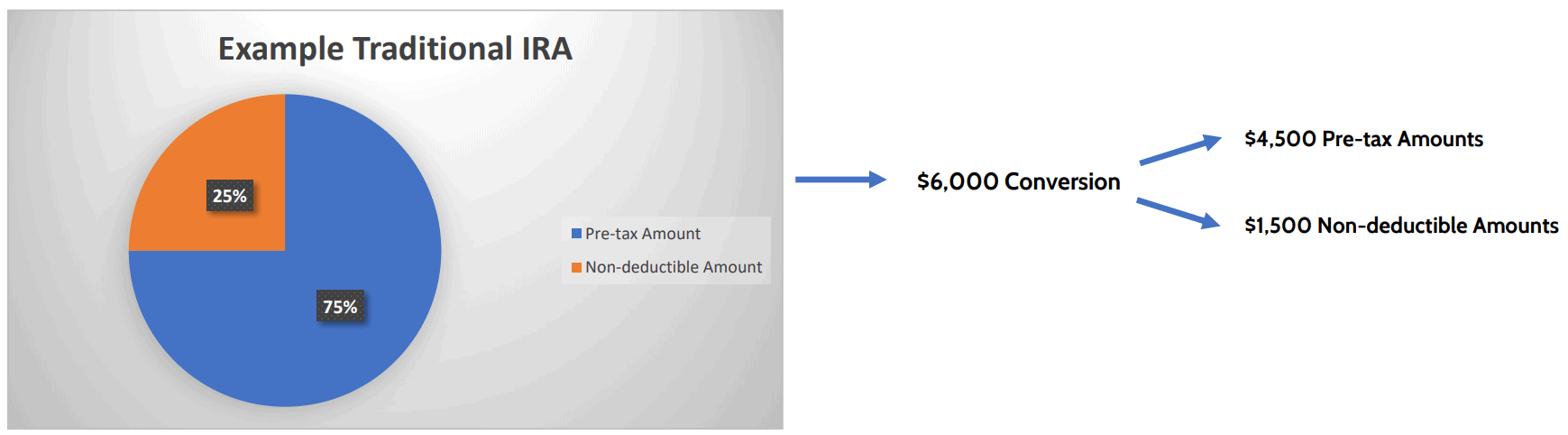

Suppose someone has a Traditional IRA with $18,000 in it which they funded by making tax-deductible contributions. Now, their income is too high to make a tax-deductible contribution. So now they want to pursue a Backdoor Roth IRA strategy.

Going back to the four steps above, you’ll remember that Step 1 was to make a non-deductible contribution to the Traditional IRA. At that point this person would have $24,000 in their Traditional IRA: $18,000 from before plus a $6,000 non-deductible contribution.

Unfortunately, the IRS doesn’t allow you to take that same $6,000 and convert ONLY that to a Roth IRA. Instead, the Pro-rata Rule works like this:

The Pro-rata Rule forces you to take a proportionate amount of pre-tax money and non-deductible money from a Traditional IRA when you convert it to a Roth IRA. This can cause unwanted tax consequences.

In the example above, the Pro-rata Rule would determine that $4,500 of the $6,000 conversion amount was pre-tax money. If our example client is in the 24% tax bracket, that means they would have to pay $1,080 of income tax on that part of the conversion ($4,500 x 24%). This defeats the purpose of doing a Backdoor Roth IRA contribution, as we’re trying to avoid paying taxes.

What if you want to do a Backdoor Roth IRA but already have a Traditional IRA with money in it? You’re not out of luck!

To “get rid” of your Traditional IRA balance so you can do a Backdoor Roth IRA, you “roll” the Traditional IRA into your employer’s 401(k). Not every employer plan allows you to roll IRA money into the 401(k) plan, but most do. You should also consider whether your 401(k) investment choices and fees are worth doing it.

But by rolling your Traditional IRA to a 401(k), you can get to a zero balance in your Traditional IRA. This allows you to do a Backdoor Roth IRA contribution without having to worry about the IRS Pro-rata Rule.

Conclusion

Of all the ways for high-income earners to save more for retirement, the Backdoor Roth IRA strategy is one of the most logical; it’s the right thing to do after maxing out 401(k)s. You get tax-free growth on your investments, and tax-free withdrawals when you pull money out of the Roth IRA.

Because of the complications from the IRS Pro-rata Rule, it may be a good idea to work with a financial advisor if you already have a Traditional IRA with money in it. The last thing you want to do is make a mistake and get a surprise tax bill next April.

At Financial Design Studio, we help create retirement savings strategies for high-income earners. And because we have in-house tax expertise, you can rest assured that more advanced strategies such as the Backdoor Roth IRA contribution are being done correctly.

Ready to take the next step?

Schedule a quick call with our financial advisors.