Are You Fully Vested? [Video]

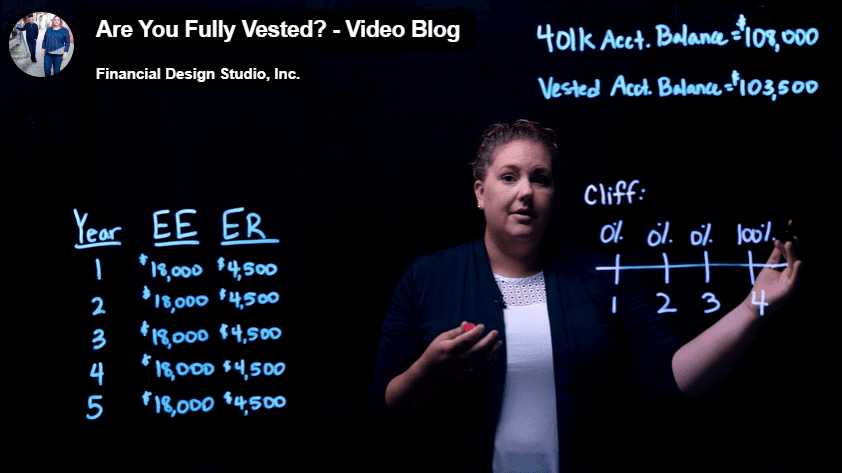

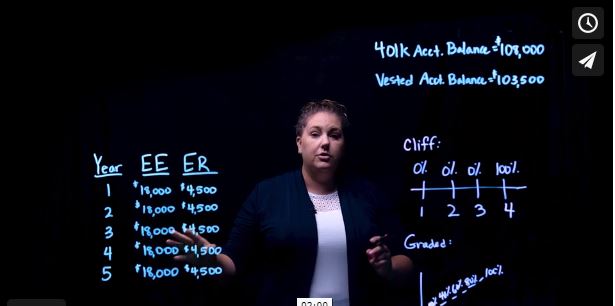

by Michelle Smalenberger, CFP® / July 18, 2022Have you ever looked at your retirement account statement and noticed two different balances? The first is an account balance and the second is the vested account balance. This is because there is a time frame that you have to wait before the employer contributions in your account are vested. Let’s talk through two common ways this happens.

For every company this is different so it’s important to know which one fits for your company plan.

Types of Vested Accounts

- Cliff vesting: Much like an actual cliff where you walk off the edge there is a point in time where 100% of your account balance becomes fully vested. Your employer will make contributions each year. But only until the year they are fully vested is the money yours, if you wanted to withdraw it for any reason. This can be after any year (typically limited to a maximum of 5 or 7 years), but in our example below we are showing an example of full vesting after year 3.

- Graded vesting: With this vesting schedule, a specified percentage will vest each year. In the following example you can see the percentage of employer contributions that would vest. If you leave your employer after year 2, you would only get 40% of the employer contributions. After year 4, you would receive 80% of the employer contributions.

With ANY vesting schedule you are always 100% vested in your employee contributions. The money you take out of your paycheck to deposit into your account is always yours. It’s not dependent on a vesting schedule.

This is really important to know. If you are considering a career change or employer change you want to know how much of the account balance you will actually be able to keep.

If you need help calculating what your balance is or how to best manage your contributions let us know. We would be happy to help you!

Ready to take the next step?

Schedule a quick call with our financial advisors.