How to Calculate Your Roth Conversions [Video]

by Financial Design Studio, Inc. / August 13, 2025Roth Conversions are a strategy to move income from high tax years to low years. But how do you decide how much to convert? In this video, we will explain how to calculate your Roth Conversion amount by looking at tax brackets, medicare premiums, and state income tax, (based on 2025 numbers).

Video Transcript

Do you want to pay lower taxes in retirement? Well, Roth conversions might just be for you. My name is Michelle and I’m a financial advisor here at Financial Design Studio. Our team helps business leaders who are retiring in the next 10 years with tax efficiency as the goal.

Now many corporate leaders expect to pay less in taxes once they retire. But between Social Security, pensions, deferred compensation, and required withdrawals from retirement accounts, they often find themselves right back in a high tax bracket, just like when they were working.

In this video, we will explain what a Roth conversion is, how it helps combat this tax problem, the steps to implement this strategy, and common mistakes to watch out for.

What is a Roth Conversion?

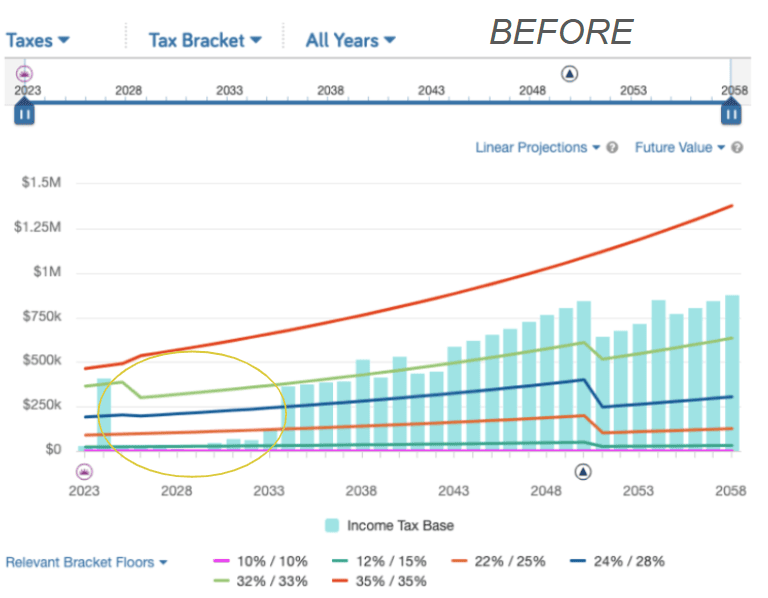

All right, so first let’s talk about what a Roth conversion is. I’m gonna use this chart to kind of explain this. We have a client who is working today and they have high income. And this green line here means that we’re in the 32 % tax bracket. So while they’re working, they’ve got high income, they’re in a high income tax bracket. But they’re retiring at the end of this year. And now you can see we’ve got several years here where we have very low tax, maybe even no tax. And that’s really highlighted by this yellow circle, you can see those years with really low taxes.

Now, if we shift forward, okay, what does my tax situation look like over my life? That’s really what you need to be looking at to see if Roth conversions make sense for you.

As we continue to move forward in retirement, you can see a point where income jumps up. All of that great saving that you did is now pushing those taxes into the future. So as we look at this green line, we can see that here later in life, we’re going to owe just as much or higher taxes.

The goal of doing a Roth conversion is to shift some of these high tax years into low tax years. So what we can notice here is even if we filled up one of these lower brackets, maybe like this 22% bracket, that’s much less that we’re paying in taxes than this 32% bracket.

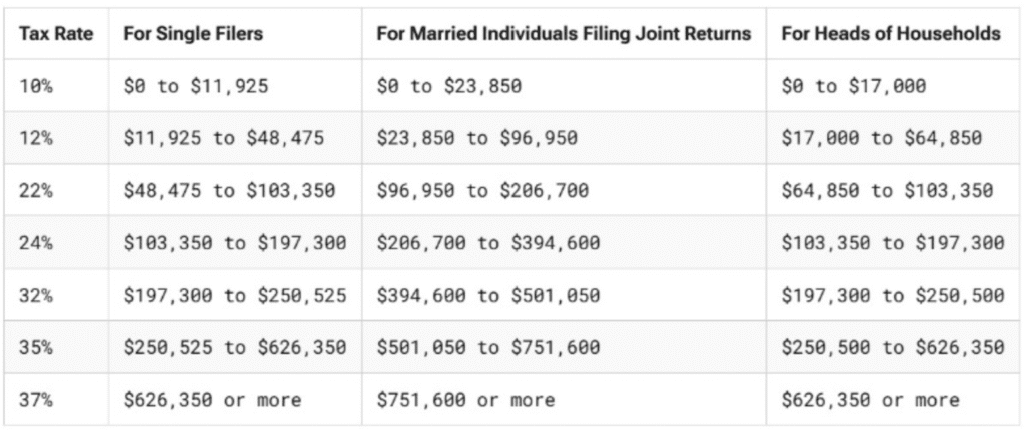

What Are the Federal Income Tax Brackets?

The first step that we just looked at was that diagram that showed your income over your lifetime. Now you can see which tax bracket you’re going to be in. Now this example that I’m showing you right now is the federal income tax brackets.

When we’re thinking about doing a Roth conversion, we really want to be converting at least 32% or less. We don’t want it to be any higher than that, because then we really wouldn’t be saving ourselves any money. Let’s look at this for a single filer. Our goal is to be in anything less than the 32% bracket. That’s as high as we want to go. There is an 8% tax savings there.

Let’s say we’re gonna do $197,000 in a Roth conversion to get up to the top of the 24% bracket, but we don’t wanna go over and pay 32%. So we’re gonna target our income to be $197,000.

How Do Roth Conversions Affect Medicare Premiums?

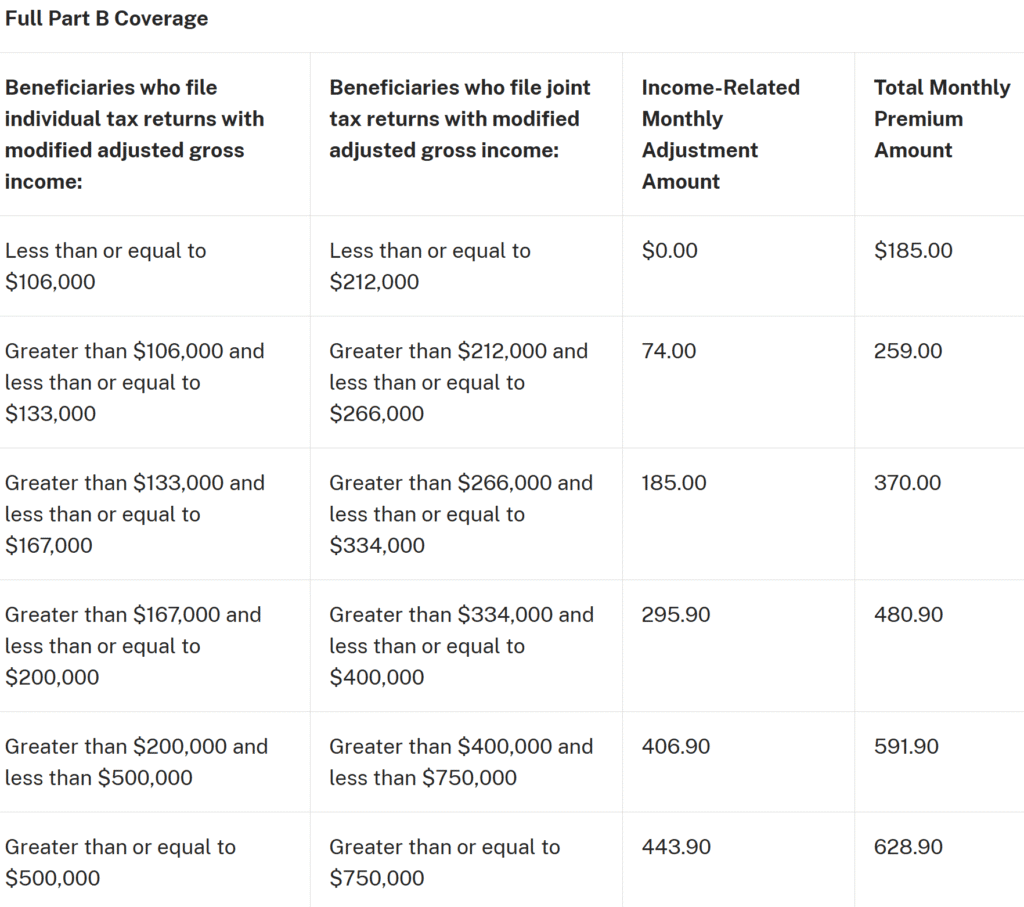

We just looked at the federal income tax chart to see how much of a Roth conversion we could do. But something that people are often surprised by and that their Medicare Part B premiums start to rise significantly when they start doing Roth conversions.

So your Medicare Part B premiums are based on your income. And so when you’re doing Roth conversions, remember that the bracket you’re in will determine what medicare premiums you’re going to pay. So let’s look at this for this single filer again. They want to do $197,000 in a Roth conversion, meaning that will be their annual income. That’s what we had decided for federal tax purposes.

So we’re gonna look at this and basically just go through each of these boxes. Starting with, is my income less than or equal to $106k? No, it’s greater than, but it’s not less than $133k. So we move up. Here their income IS greater than $167k but less than $200k. So this is the premium that we fall into. Looking all the way to the right, we can find their premium amount. This single filer with an income of $197K is going to pay $480.90 in a monthly premium for Medicare Part B coverage.

So if we’re doing a Roth conversion today, this is going to impact our Medicare Part B premiums in two years.

Now in these examples, you don’t necessarily want to look at the federal income tax bracket or the Medicare bracket to see what the costs are. You want to now look at this as a combination of the two. So if I were to do this, how will this impact my overall plan? That’s really what you’re trying to accomplish.

What About State Tax?

But you also need to watch out if your state has an income tax. Roth Conversions count as retirement income. And now surprisingly, there are a good number of states that actually do not tax retirement income. So in many states, doing a Roth conversion actually is not taxable at the state level, but you just need to know for your state, because that would be an additional consideration that you would want to think through.

What Are the Results of Roth Conversions?

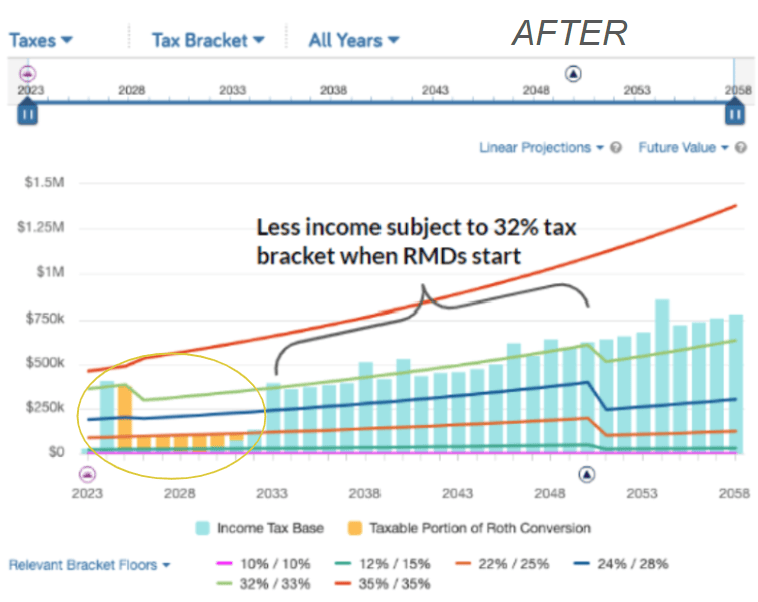

All right, so now we’re looking at the whole picture and we’re really kind of looking at the after of we’ve made a decision to do some Roth conversions here by this yellow circle area. We’ve decided we’re gonna do some Roth conversions up to some tax levels, but not over or not too much, more than we need to.

In this first year of retirement, we’re basically gonna keep ourselves in that high income tax year. We’re gonna do one large year where there’s gonna be a higher Roth conversion amount rather than these fewer years. And this is where you really have to evaluate it year by year because remember when I said your Medicare premiums, age 65 is when those start and they look at your income two years prior.

Well, let’s say this is someone who’s retiring when they’re actually age 60. So if someone is 61 and in their first year of retirement, we might want to do a large Roth conversion. Two years ahead, they’re only gonna be 63 and they won’t have started Medicare yet. They still have two more years before that high income is really going to impact them. Once they hit 63, we’re keeping these Roth Conversions in this low 22% bracket, shown by the orange line.

Leading up to Medicare starting ages, you can see that we’re being thoughtful of the amount of the Roth conversion that we’re doing. We don’t want to do too much and push our premiums too high. But we’re doing enough so that we’re still paying a reasonable amount for Medicare. We did take advantage of this one year in the beginning where we did high Roth conversions and got a lot of those funds into Roth IRAs early on.

Remember in our before example, we had a lot of years up here where we were paying 32% bracket. But now what’s happened, we shifted some of these into these lower years, shown in our yellow circle.

So for a lot of these, they’re only paying up to the 24% bracket. We just went to the top of that in these. In these early years, we are saying, let’s do enough to keep most of these later years in lower brackets.

What you will notice when you see the accumulated value of how much you’re saving in taxes across your lifetime is that number gets to be very large. So I’m going to pay less in taxes, so I’m keeping more of my money all by just timing out when I do the Roth conversion.

Your Next Steps for Roth Conversions

Now there are some common things that you need to watch out for with Roth conversions and that’s that they aren’t a silver bullet and they aren’t for everyone. So what you notice is we didn’t completely wipe out the income tax that this client would pay over the course of their life, but we did minimize the taxes. So it isn’t necessarily something that’s going to fix 100% of the taxes that you pay. And in fact, it can really mess up your taxes if you don’t do them right. So it’s really important that you’re looking at this year by year. you can work with a financial advisor who’s helping you all year every year.

So if you are someone who’s starting to think about retirement and you want to do so in a tax efficient way, we’d love to help you. Click “Get Started” on our website to schedule a free consultation with our team to discuss your retirement needs. Thanks for watching!

Bonus: Retirement Planning Guide

Ready to take the next step?

Schedule a quick call with our financial advisors.