[Video] Roth Conversions: What Are They & How Do They Work?

by Stephen Smalenberger, EA / August 8, 2017

STEPHEN SMALENBERGER, EA

We want to introduce a design element that we like to use in financial plans, when it makes sense. And this strategy is known as the Roth Conversion.

Money may be put into a Roth IRA in two forms:

- Contribution(s)

- Conversion(s)

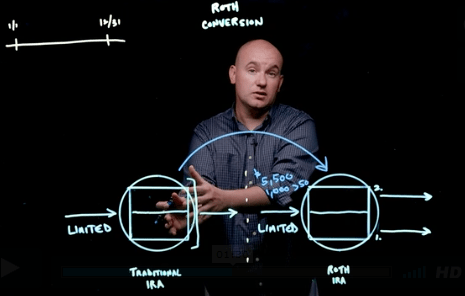

As explained in prior articles and videos, the Roth IRA contributions are limited to either $5,500 or $6,500 for individuals over the age of 50. The ability to make a contribution depends upon whether you have enough earned income and may be completely eliminated if you make more than the income limit.

Yet, no matter how much you make, how much you own, what your age or whether you are working or retired… the conversion is available to you!

Essentially, what you are doing is shifting assets (cash and/or investments) from one type of an account to another.

Unlike the contribution which has an annual limit, the conversion is unlimited. That means that you can decide each year how much makes sense to convert in order to accomplish your goal(s).

This movement of money creates a taxable event since funds are leaving an account that is tax-deferred and moving to an account that is tax-free.

How much to convert is an important consideration. A full conversion of an account can be done. However, you may find that this pushes you up into a high tax bracket and causes many of the tax deductions enjoyed to be phased-out. Another maybe better option would be to process partial conversions over a period of time. This means moving just enough to fill your current tax bracket and then deciding what bracket after that makes sense.

Timing is also an important consideration. Whether that is timing of year due to market conditions or timing in your life related to other taxable events, having a specific action plan in place is important.

In summary, here are the important takeaways:

When?

A Roth Conversion can be processed any time between January 1st and December 31st for that respective Tax Year.

Who?

Anyone that has a tax-deferred account can convert funds to a tax-free account. There is no income limit, age limit or conversion amount limit.

How Much?

You can convert all, some or none. The choice is up to you depending upon your specific goals and circumstances.

There is power in laying out a plan since it identifies opportunities that exist and how implanting a strategy will impact you and your family.

As always, there are many considerations and details not addressed in this post. It is meant to be general and educational in nature. However, if this raised a question or prompted curiosity on how various planning strategies could potentially be applied to your particular situation… please let us know. We are happy to help!

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

How to Plan for Deferred Compensation in Retirement [Video]

In this video, we share how to plan for deferred compensation as it impacts your income and taxes in retirement.

What if the Market drops before I Retire? [Video]

In this video, financial advisors share the strategies they use before, during, and after if the market drops before you retire.

Stephen Smalenberger, EA

Steve enjoys getting to know clients and hear their unique stories and the lessons learned which has brought them where they are today. One of the reasons he enjoys what he does is the ability to show the outcome that can be achieved with different choices. He also enjoys continually learning.