[Video] How Tax-Free Accounts Work

by Stephen Smalenberger, EA / July 25, 2017STEPHEN SMALENBERGER, EA

There are only three types of accounts:

- Taxable

- Tax-Deferred

- Tax-Free

We focused on the first two types already. Let’s focus on the last, Tax-Free.

The accounts in this registration category include the following:

- Roth IRA

- Roth 401(k)

- Roth 403(b)

- Roth 457

- Roth Thrift Savings Plan (TSP)

The word Roth is really important because it signifies how the account is treated per IRS rules.

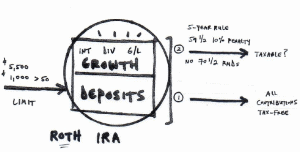

The movement of money within this type of account is seen below:

Who are these accounts for?

Anyone who has earned income from an employer or from self-employment can make contributions or have payroll deferrals. In this case, young children and retirees would not qualify.

How much can you deposit?

The amounts are limited to the annual contribution limits:

- Roth IRAs: $5,500 or $6,500 (if over the age of 50)

- Roth 401(k)s/403(b)s/457/TSP: $18,000 or $24,000 (if over the age of 50)

How are these accounts taxed?

Hopefully, these accounts are being saved for your retirement years. If so, none of the funds in the account would be taxable either to you or your heirs.

There are not many absolutes but here’s one: you can always take your contributions back out of a Roth IRA tax-free! That means any money that you put in, you can take out without triggering a taxable event.

The rules are a little different for the employer-based retirement plans like 401(k)s which this video does not go into.

Knowing that your contributions are not taxable, what about the growth? That depends.

First, how old are you when you need to take the money out? If it is before retirement age, 59 ½ specifically, this money may be taxable and may also incur a 10% Early Distribution Penalty. Therefore, it’s important to know the rules or work with an advisor that does. Second, has the Roth account been established long enough which is in reference to the 5-year rule.

If you meet both the age and time tests, the withdrawal is a “qualified distribution.” If not, it’s termed “non-qualified” and may have tax implications if no exceptions apply.

Are there any restrictions on the amount that you can withdraw?

Again since these accounts are for retirement purposes, there are some restrictions based upon your age. However, unlike the Traditional IRA, the Roth IRA account owner never has to start taking Required Minimum Distributions (RMDs) at age 70 ½. So the funds can continue to grow and multiply tax-free! Be careful because this is where the Roth 401(k) and the Roth IRA differ. If your Roth 401(k) is not rolled over into a Roth IRA then you may have to take an RMD. The funds are still tax free when distributed but you do have to remove them as calculated each year.

As always, these posts are general in nature and are meant to be educational, introducing various topics. If anything shared raised a question or prompted some curiosity of a strategy that could potentially be applied to your particular situation… please let us know. We are happy to help!

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

How to Plan for Deferred Compensation in Retirement [Video]

In this video, we share how to plan for deferred compensation as it impacts your income and taxes in retirement.

What if the Market drops before I Retire? [Video]

In this video, financial advisors share the strategies they use before, during, and after if the market drops before you retire.

Stephen Smalenberger, EA

Steve enjoys getting to know clients and hear their unique stories and the lessons learned which has brought them where they are today. One of the reasons he enjoys what he does is the ability to show the outcome that can be achieved with different choices. He also enjoys continually learning.