Mortgage Rates Have Dropped To A New Low: Should I Refinance?

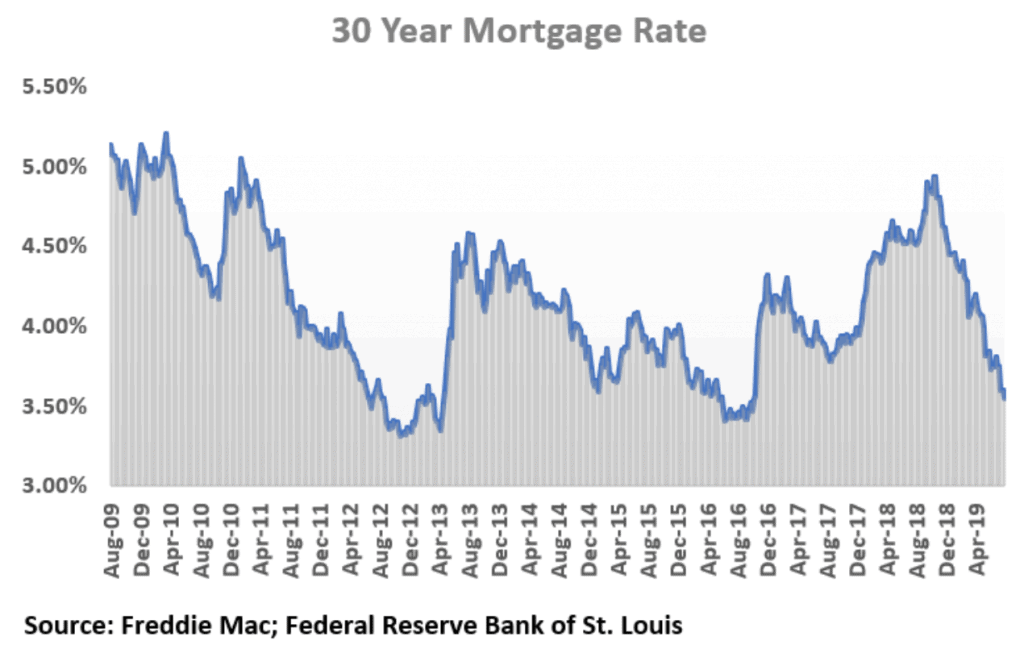

by Financial Design Studio, Inc. / August 29, 2019There’s been a lot of talk in the news lately about low interest rates and inverted yield curves. One newsworthy item that is being missed is how mortgage rates have dropped. As recently as last November, mortgage rates were approaching 5.00%. Now they’ve dropped all the way to 3.55% based on the latest survey from Freddie Mac.

So it begs the question, is now the time to refinance your home?

The only time mortgage rates have been lower than today was in late 2012 and a brief period in mid-2016. Meaning, many homeowners likely have mortgage rates that are higher than what they could get today.

Should you refinance?

The rule of thumb we here at FDS like to use is to start thinking about refinancing a mortgage when a family can reduce their interest rate by at least 0.50%. There’s a cost to refinancing a mortgage so you want to make sure the rate benefit is high enough to offset those costs.

Families can also take advantage of these low rates to not only get a lower rate, but to reduce the term of their mortgage as well. 15-year mortgage rates tend to be 0.50-0.75% lower than comparable 30-year mortgages. The current 15-year mortgage rate of 3.03% is 0.52% below the 30-year mortgage rate.

Let’s look at an example to see how this might work. Suppose we have a family that took out a 30-year mortgage 5 years ago at an interest rate of 4.25%. Mortgage rates have dropped, and today they can get a 30-year mortgage at 3.60% or a 15-year mortgage at 3.00%. They have three options:

- Keep their current loan (which has 25 years to go)

- Refinance into a new 30-year mortgage

- Refinance into a new 15-year mortgage

Here’s the refinancing math.

Here’s how the math would work out for them in terms of their monthly payments and total interest paid. The total interest you see for Stay in Current Loan is the interest they would pay on the remaining 25 years of their current mortgage.

By refinancing into a new 30-year loan, this family could save about $170 a month on their payment and still pay about the same amount of interest compared to staying in their current loan.

On the other hand, if they refinanced into a 15-year mortgage, they’d see their monthly payment go up $300 a month but they would pay their home off 10 years sooner and save over $75,000 in interest over the life of the loan!

While a lot of people will focus on the monthly payment amount, one should also consider the total interest paid and when the loan will ultimately be paid off. For homeowners in their mid-40’s or later, taking out a new 30-year mortgage will mean that they will be making mortgage payments into their retirement years, which is generally not recommended.

What should you do?

The takeaways in this Weekly Update are to look at your current mortgage and assess whether your current mortgage rate is too high relative to what you could get in the market today. Secondly, it’s also a good time to think about the bigger picture of when you’d like to have your home paid off and how much extra cash flow you have in the budget to put towards your house.

Wondering how this affects your investments? Schedule a call with Michelle and Steve to discuss your portfolio today.

Ready to take the next step?

Schedule a quick call with our financial advisors.