Everything to Know About Health Savings Accounts

by Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer / August 30, 2023

2023 marked the 20th year since Health Savings Accounts – or “HSAs” for short – first became available for use. Most people have heard about them, even if they don’t currently use one. While many people are aware of the benefits of using an HSA, we find several cases where people aren’t sure how to make the most of them. “What’s the use case?,” we often hear. HSAs are a powerful retirement planning tool, especially for high-income earners, those looking to retire early, or those concerned with how they’d meet an unexpected long-term care need when they get older. This post explains everything you need to know about health savings accounts: who they’re for, who they’re not for, and special use cases where they can be powerful.

Features of Health Savings Accounts

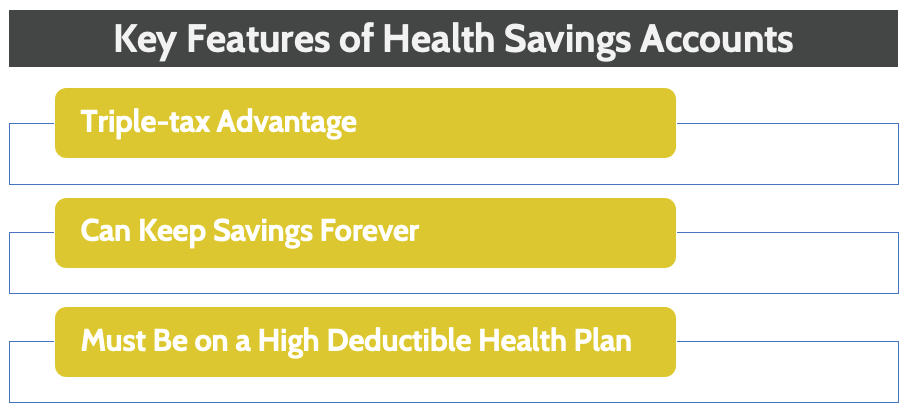

There are three key features of HSAs that are important to understand. They go a long way to answering the question, “Is an HSA right for me?,” as we’ll see in the rest of the article.

Key Feature of HSAs: The “Triple-tax Advantage”

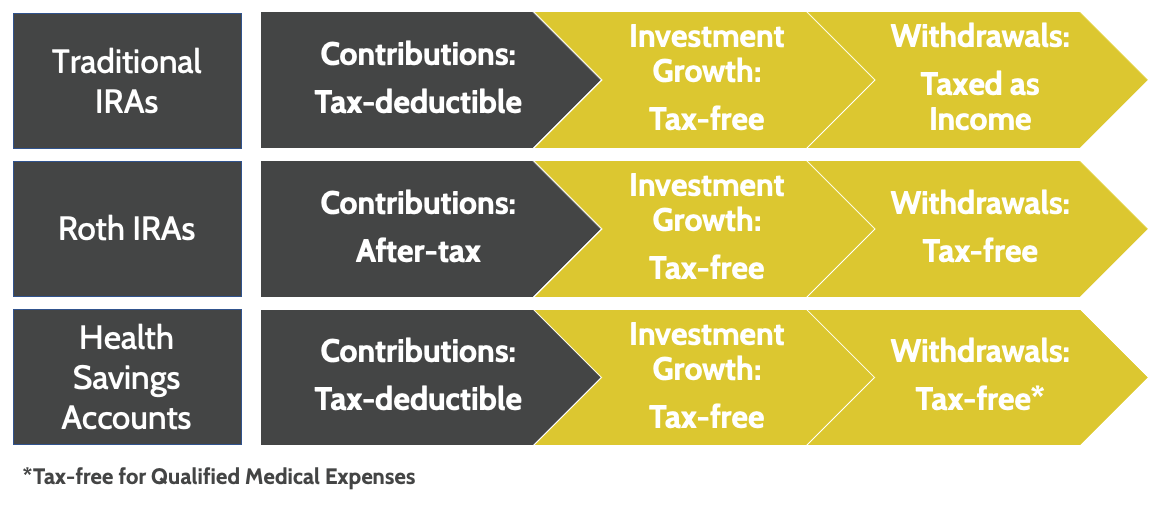

The most important feature to understand about HSAs is the special tax advantages they enjoy. They look and act much like Traditional and Roth IRAs, giving the saver a tax benefit either when they put money into the account or when they take money out. And just like IRAs, HSA also offer tax-free growth of the savings put into the account.

However, IRAs only offer two tax benefits. The HSA offers three, which is why we refer to HSAs having a “triple-tax advantage.” The graphic below shows you the key tax differences between Traditional IRAs, Roth IRAs, and HSAs.

If you look at the graph closely, you’ll see that for Traditional and Roth IRAs, there’s always a point when Uncle Sam is getting his cut by taxing you. For Traditional IRAs, it’s when you take money out during retirement. For Roth IRAs, it’s when you put money in.

Health Savings Accounts are the only account to enjoy the “triple-tax advantage” as long as any withdrawals are used to pay for Qualified Medical Expenses. What are Qualified Medical Expenses? The list is very long, but include:

- Copays for doctor visits

- Out-of-pocket expenses for doctor and hospital visits, if you haven’t reached your plan’s deductible

- Prescribed medicines

- Dental treatments

- Glasses & contact lenses

- Medicare Part B & Part D premiums

- COBRA premiums

As long as money taken out is used to pay for a medical cost, you won’t have to pay tax on any money that comes out of your HSA. However, if you take money out of the HSA for anything other than medical expenses, you’ll pay tax:

- Under Age 65: Pay income tax + 20% tax penalty

- Age 65 or Over: Pay income tax (no penalty)

Key Feature of HSAs: No Use-it-or-Lose-it of HSA savings

Many employees confuse the rules that surround HSAs and a similar-sounding benefit, the Flexible Spending Account (“FSA”.) The main point of confusion stems from what happens to money you put in that you don’t use by the end of the year.

FSAs have what’s called a “use-it-or-lose-it” feature. This rule comes straight from the IRS and says that any money you contribute to an FSA is lost if not used it by the end of the year. While FSAs can help pay for medical expenses using pre-tax dollars, too often we find people in a panic every December trying to empty their FSA by year-end. My wife is an optician and sees this happen every year!

Health Savings Accounts do NOT have any use-it-or-lose it feature. You can leave any money you put in there until the day you pass away. Even if you’re no longer on a HSA-qualified health insurance plan (more on that later), you can keep money you saved in an HSA while you were on a qualified health plan.

Pro Tip: If you’re good at savings receipts, it’s a great idea to save all your medical-related expense receipts. HSAs allow you to take a tax-free withdrawal for any qualifying expenses, no matter when you had the expense. For example, if you paid $100 for eyeglasses this year, you can save your receipt and take $100 out of your HSA in 10 years for that purchase.

Key Feature of HSAs: Require High-Deductible Health Plans

The last key feature to be aware of is that you have to have a special type of health insurance plan to open and contribute to an HSA. These are called “high-deductible health plans,” or HDHPs.

As the name implies, this is a type of health insurance that has higher deductibles. Of all the features to consider about HSAs, this is the most important. Why?

If you have medical issues that require regular doctor visits and treatment, you’re well-aware that those costs can add up quickly. Having a health plan with lower deductibles and out-of-pocket maximums is most often the best option. Even though there are many advantages to HSAs, the fact you’d have to be on a health insurance plan with high deductibles may prove more costly than the HSA is worth.

However, if you’re younger and/or in great health and rarely need doctor visits, getting on an HSA-eligible high-deductible health plan might be worth it. There won’t be high annual medical expenses, and you can use that extra money to put money away into an HSA.

When you shop for health plans, most likely the insurance carrier will make it clear if a particular plan is HSA-eligible or not.

Contributing to a Health Savings Account

Getting money into an HSA looks and feels a lot like when you contribute to your IRAs or employer’s 401(k). You can make direct contributions to it like you would a personal IRA, or your employer can withhold a certain amount from your paycheck and put that in your HSA, just like they do with your 401(k).

Another similarity to IRAs and 401(k)s is that you’re limited how much you can put in each year. For 2023, these annual contribution limits are:

- Single taxpayer: $3,850

- Family: $7,750

- Age 55 and Over Catch-up Contribution: $1,000

One unique rule about contributing to an HSA is that you can’t contribute to an HSA once you’re enrolled in Medicare. This differs from IRAs, where recent tax law changes did away with age limits for IRA contributions.

If you sign up for an HSA through your employer, they may offer to make HSA contributions for you. The most common way companies do this is by offering to contribute a specific dollar amount. For example, they may offer to contribute $1,000 to your HSA for every year you’re on an HSA-eligible health plan. Employer contributions count against your annual maximum contribution.

Once you contribute money to an HSA, you face the next topic we’re going to discuss: “What do I do with my HSA savings?”

How to Use Health Savings Account Funds

The discussion to this point has been mainly about understanding HSA mechanics. Now, it’s time to talk about HSA use cases and why they may prove valuable.

There are two things you can do with money you contribute to an HSA. You can either use it immediately, or you can invest it for the future.

HSA Use Case #1: Use Funds Immediately to Pay Medical Costs.

This is the most common way we see people use HSAs. They contribute money to the HSA, and then during the year they take the money right back out as they incur medical expenses.

Is there anything wrong with using an HSA this way? No! Many high income earners with bigger families find this to be a great way to pay for ongoing medical costs (new eyeglasses for the kids, etc) while getting a tax break.

Suppose an employee with a large family is making $400,000 per year, putting them in the 32% tax bracket. If they contribute the maximum $7,750 to their HSA, that lowers their taxable income dollar-for-dollar, saving them $2,480 in Federal income taxes [$7,750 x 32%]. They then use that $7,750 to pay for copays, deductibles, and other medical expenses. The logic is simple: “If we’re going to spend this money on medical costs anyway, we might as well get a tax break by using an HSA!”

Pros:

- Get tax deduction on your HSA contributions

- Employer may offer to contribute money to your HSA

Cons:

- Don’t take advantage of tax-free investment growth

- Tax benefit depends on your marginal tax rate, which might be low

HSA Use Case #2: Invest HSA Contributions to Generate Growth and Cover Future Expenses.

This is the less common – but much more powerful way – to use HSAs. By default, most HSA plans put your contributions into an HSA checking account that pays little in interest. However, most companies that offer HSAs also offer ways to invest those savings, much like you would in a 401(k) or IRA.

Investing HSA contributions in stocks and bonds exposes you to investment risk just like a retirement plan. But as we’ll see below, if you’re intentional about WHY you’re contributing to and investing money in an HSA, it can help cover future (higher) medical costs when you’re older.

Contributing to an HSA and investing the money for the future is one of the key savings strategies we recommend to high-income earners when they’re already maxing out IRAs and 401(k)s. It’s a great way to save more for retirement. [See our downloadable guide, “5 Retirement Savings Strategies for High Income Earners”]

How to Think About Your HSA

The concept is simple: By contributing to an HSA and investing it for the long-term, you create a dedicated pool of money that’s there to cover your future medical needs. As we’ve written about before, the cost of healthcare only goes up as you get older. And for those concerned that they might need long-term care or memory care when they’re older, a large HSA account can go a long way to covering those costs, allowing you to “self-insure” yourself against that risk.

Pros:

- Earn tax-free growth on your HSA investments over the long-term

- Create a dedicated pool of assets to cover future medical needs

Cons:

- Investment values fluctuate and may have lost value in the event you have to take the money out for a medical emergency

- Non-spouse HSA beneficiaries are forced to remove all HSA funds and pay taxes in the year you pass away

There’s no right answer on how best to use an HSA. With most things in life, the best use of an HSA depends on your particular circumstances.

Who is an Health Savings Account Good For?

Let’s look at some examples of people that might get a lot of value out of using an HSA.

Young and/or healthy people with low annual medical expenses.

Unless someone has struggled with a disease since birth, most young people rarely end up going to the doctor other than for the occasional physical or when they get sick. This also applies to anyone who actively exercises and takes care of themselves.

A high-deductible health plan with an HSA can be a great option. Even though the health plan will have higher deductibles, if they’re not likely to spend much on medical care, then it shouldn’t be an issue. And if there’s room in the budget to make HSA contributions in addition to regular 401(k) or IRA contributions, all the better.

Those already maxing out 401(k) contributions.

A common question we get from high-income earners is how they can save more for retirement once they’re already maxing out 401(k) and IRA contributions. HSAs are definitely high on the list, assuming other factors (such as poor health) don’t argue against using them.

High-income earners have a special challenge of saving enough money to cover their living expenses when they retire. Social Security will only cover a portion of their retirement expense needs. By saving to an HSA, they can create a “bucket” of savings dedicated to medical expenses when they’re older.

If you’re concerned about needing long-term care when you’re older.

Long-term care is huge for many Americans. The cost of needing long-term care or memory care can easily run $6,000-$10,000/month in today’s dollars.

Unfortunately, long-term care needs are often hereditary. Meaning, if you have a family history of parents or grandparents needing long-term care, the chances that you’ll need it are higher.

More unfortunate is the fact that long-term care insurance is extremely expensive. The insurance industry has struggled to offer this kind of insurance since it became popular in the late 1990s. While you can get long-term care insurance, it shocks many people how much it costs and how little the benefit is if you end up using it.

HSAs are a solution to self-insure against this risk. By saving into an HSA and investing it for your future, you might build up enough money to cover several years of long-term care expenses.

Early retirees.

Anyone looking to retire early – which we’ll define as several years before Age 65, when Medicare kicks in – will face the prospect of very high health insurance costs. When you stop working, you not only give up your income but also the benefits you were receiving while employed.

HSA funds can’t be used to pay for Marketplace (Obamacare) premiums. But HSA funds can pay the cost of continuing COBRA coverage. By law, any company that has at least 20 regular employees offers departing employees COBRA healthcare coverage for up to 18 months. While COBRA coverage isn’t cheap, the plans are often better than what you’d get on the Marketplace for a similar cost.

Think of someone who wants to retire at Age 62. They would have a 3 year gap from ages 62 through 64 before Medicare coverage would kick in at Age 65. If this person has a fully stocked HSA, they can cover the cost of health insurance for half of this 3-year gap (18 months) via COBRA coverage.

Even if someone is looking to retire very early, say their mid-50s, they can of course use an HSA to cover the cost of COBRA for 18 months. But after that, when they’re on a Marketplace plan, they can use HSA funds to cover insurance deductibles and other medical costs, avoiding having to “dip in” to their retirement savings.

Who Isn’t an Health Savings Account Good For?

Individuals with higher annual medical costs. If you suffer from a chronic illness or have to go to the doctor a lot, an HSA strategy isn’t likely a good option. The reason is simple: the HSA requirement to have a high-deductible health plan means you’ll have to cover a lot more of your ongoing medical expenses before insurance coverage kicks in.

Not maxing out retirement account contributions. In almost all circumstances, if you’re not already maxing out your 401(k) or IRA, then your best bet for your next extra dollar of contributions is to put it towards those accounts rather than an HSA. Yes, you’d get all the benefits of an HSA mentioned above by contributing to it. But remember, your 401(k) and IRA can cover any type of expense need you have in retirement, including medical expenses.

Those in a low tax bracket today or in retirement. The primary advantage of an HSA is its “triple-tax advantage.” The value of this tax advantage rises and falls with one’s marginal income tax rate. Someone in the 35% tax bracket today would get a larger tax deduction than someone currently in the 12% tax bracket. Similarly, someone expected to be in a high tax bracket while in retirement would get more value from tax-free HSA withdrawals than someone expected to be in a low tax bracket.

That’s not to say there wouldn’t be value to having an HSA regardless of what tax bracket you’re in. But the value diminishes at lower tax brackets.

Everything You Wanted to Know About Health Savings Accounts

This article covered what you need to know about HSAs. It’s a powerful savings tool that’s underappreciated by many people despite being around for 20 years. By understanding the mechanics of how they work, you can better understand whether contributing to an HSA would be an excellent strategy to pursue.

Early retirees and high-income earners that already maxed out other savings strategies should add the HSA to their retirement “arsenal.” Given the high cost of healthcare – and especially when you’re older – having a dedicated bucket of funds set aside for these costs can be quite valuable.

We’ve worked with many clients approaching early retirement and have helped them plan out their health coverage needs BEFORE they officially retire. Having a simple plan of action in place to cover this important cost can set your mind at ease and give you confidence to make that important (and scary!) early retirement decision. If you’re looking to gain confidence about your finances and plan for the future, please reach out to us to see how we can help you.

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

Should I Retire Early? The Pros, Cons, and Hidden Costs [Video]

In this video, we explore the financial pros and costs, as well as the hidden costs we see as financial advisors when clients retire early.

Ep 75: How to Decide When to Move into a Retirement Community

In this episode, Michelle interviews Royce on the process of downsizing, picking the community, and what her family's experience has been.

Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer

Rob has over 20 years of experience in the financial services industry. Prior to joining Financial Design Studio in Deer Park, he spent nearly 20 years as an investment analyst serving large institutional clients, such as pension funds and endowments. He had also started his own financial planning firm in Barrington which was eventually merged into FDS.