Cash Savings Rates: Back to Zero

by Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer / April 16, 2020

Keeping cash in savings accounts for emergencies and other cash needs is a bedrock of sound personal financial planning. But there’s a trade-off: earning lower returns.

As we assess the post-COVID landscape, we turn our attention to the outlook for cash savings rates. Unfortunately, the potential to earn decent interest rates on our cash isn’t very good!

During the Great Recession of 2008-2009, the Federal Reserve took the bold step of cutting short-term interest rates all the way to zero. That policy was followed by other central banks across the globe, leading societies into a world of zero rates.

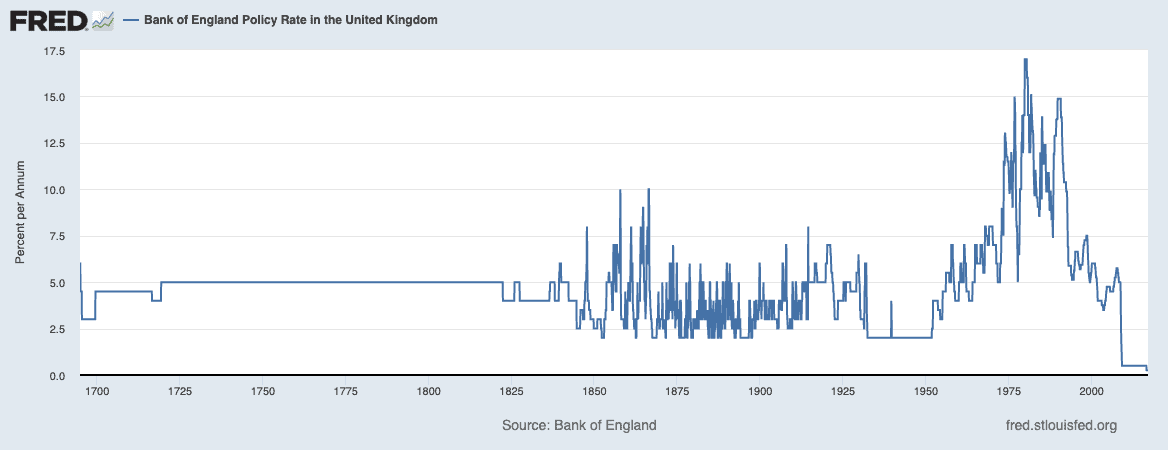

How unusual are short-term rates of zero percent? We can look at data from the Bank of England’s policy rate going all the way back to 1694!

Until the financial crisis of 2008, England’s short-term rates never went below 2.00%. Today, they’re 0.25% – effectively zero for savers.

Fast forward to 2020, the Federal Reserve cut its short-term interest rate twice in March, bringing it down to a range of 0.00-0.25% in order to combat the negative impact of the COVID-19 virus. We last saw rates at this level in late 2015.

Interest rates on savings accounts and money market funds are largely determined by short-term interest rates.

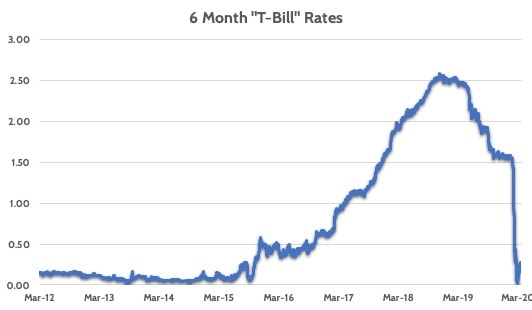

Money market funds will invest in government and/or corporate debt that matures in less than 1 year. To get a sense for where rates are going, we like to look at the rate of 6-month Treasury Bills (“T-Bills”).

Prior to 2016, 6-month T-Bill rates were just above zero. During that time, most money market funds were paying interest rates of 0%. The same was true for big bank savings accounts.

As rates rose from 2016 to 2019, cash savings rates also moved higher, topping 2.50%. But with 6-month “T-Bill” rates dropping rapidly to less than 0.25%, it’s only a matter of time until bank savings accounts and money market rates drop towards zero again.

What can you do?

Online banks tend to offer better savings rates than their branch-based banking peers. The reason for this is because gathering deposits from customers is a lot easier if the bank has a physical bank branch presence. Even in today’s digital world, people get comfort knowing their bank is around the corner if they need them.

To compete with this advantage, online banks need to ‘entice’ customers with higher savings rates. And this enticement can be very attractive.

For example, there are online banks right now that are paying 1.50% for online savings. This is 2-3 times higher than the rates you could get on money market funds.

Granted, these juicy rates are likely to come down in coming months, but not all the way to zero like branch-based banks and money market funds.

The outlook is for the Federal Reserve to keep rates near zero for the foreseeable future. In fact, bond markets are expecting the zero-rate environment to last at least until 2024.

Given this, it might make sense to take advantage of the higher savings rates you can get from an online bank.

And remember, online bank deposits enjoy the same $250,000 FDIC insurance that your local bank has.

Wondering how this affects your future finances? Schedule a call with Financial Design Studio, financial advisors in Deer Park, to discuss your portfolio today.

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

How Will AI Affect the Jobs Market?

White collar workers are wondering how AI will affect the jobs market, and their career. This article shares what's noise and what's real.

Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer

Rob has over 20 years of experience in the financial services industry. Prior to joining Financial Design Studio in Deer Park, he spent nearly 20 years as an investment analyst serving large institutional clients, such as pension funds and endowments. He had also started his own financial planning firm in Barrington which was eventually merged into FDS.