What if the Market drops before I Retire? [Video]

by Financial Design Studio, Inc. / March 13, 2026This is the number one concern we hear from people approaching retirement. It’s our job as financial advisors to know how to handle possible market drops before you retire. In this video, we share what we do before, during, and after a drop, as well as opportunities you can take advantage of!

Video Transcript

A question that keeps business professionals up at night is what if the market drops? Looking at history, it’s not really a question of if but when.

Hi, my name is Michelle and I’m a financial advisor here at Financial Design Studio. We help business professionals retire in a tax-efficient way. So if retirement is getting close for you, we have a free retirement planning guide that you can download, which is linked below.

Our job as financial advisors is to run your retirement plan for you so you never have to worry about these risks. So before we dive into three ways we help protect clients’ retirements, I want to share the example we’ll be working with today.

Example: The 2008 Market

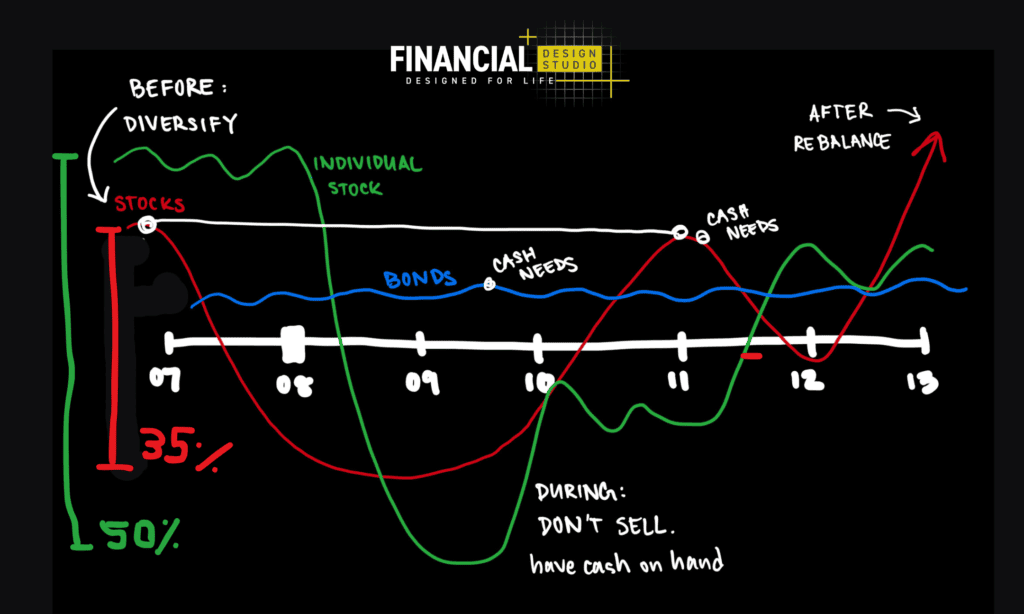

Let’s think back to a specific market drop like 2008, where there was a 35% drop in equities in the stock market and fast growing companies were also hit hard. So in our example:

- A client had $2 million in their portfolio before the market after that 35% market drop, now they have $1.3 million in that same portfolio.

- We’re going to assume that they had $1 million dollars in their company stock and now they had a 50 % drop in that single stock and so now they only have $500,000 in their portfolio.

- Now one additional thing is that this client still needs to take $180,000 out of portfolio each year, whether the market has dropped or not. That’s 10% of this clients new net worth!

You might even remember back to 2008 where you did watch your 401k or your stocks drop in those values. You may remember what that felt like.

The exact wrong time for the market to drop like this is the day you retire you’ve already decided and left. There’s no going back to your employer just because the market drops. What you really want to be thoughtful are the strategies you have in place, so that if something like this happens, your plan is protected.

Before a Drop: Diversify

I wanna share three strategies that we’re using as advisors in this example of what the market did in 2008. So if we just look at this example here of the market, I’ve drawn here just the S &P 500 starting really in 2007, 2008, and just a handful of years after that.

So let’s think about our first strategy. No one knows what tomorrow will bring. You never know if a market drop is coming or what stocks it will impact. Which is why you want to ensure your portfolio is ALWAYS diversified. You can read our article on the proven success of diversified investing here!

Diversification is especially important if you have company stock. We work with a lot of business leaders with large positions in company stock. They’re not quite sure how much they should hold or how much to diversify. But when the market drops, those individual company stocks can be hit much harder than a diversified portfolio.

We can see it took three years for the market to actually come back to where we were. So 2011 to 2010, this is where we kind of saw how long it takes for the stock market to come back. Now, we’re only looking at an example of the stock market. That whole time, bonds continued to stay steady and maintain their value!

Thinking back to our example, when our client needs to withdraw $180,000, they would take that from bonds. But then once the market starts to recover in this 2011-13 as it just continues to go up, now we can start to stocks again.

During a Drop: Don’t Sell!

Then during this market drop, you might remember to 2008, one of the instincts that you might feel is to panic sell everything that you own. No one wants to see that drop in your portfolio. It seems more reasonable to cut your losses before they increase.

But we always remind clients that we have seen historically the market comes back. If you sell, you lock in your losses and miss out on the growth that is coming.

And again, if we have a diversified portfolio, we can allow the market to come back because we already have cash on hand, thanks to our diversified portfolio.

For our clients, we make sure that they have the cash that they’re going to need already set aside for the year. They can withdraw it whenever they need. It’s really important to us to know our clients, so that we can say, “here’s the cash you’re going to need,” and we make sure it’s set aside.

After the Drop: Rebalance

After the market has seen a big drop here, we want to make sure that we still have a balanced portfolio. Large movements may have shifted your portfolio so you are missing out on important long term growth.

As the market recovers, you want to make sure you are positioned to take advantage of that!

Those are really three things kind of before, during, and after that we want to make sure your portfolio is set up to do. You should feel confident going into retirement.

Opportunities When the Market Drops

Now, something I want to explain is there are strategies like this, there’s also opportunities when the market drops. And let me just touch on a few of those.

Roth Conversions

And the first one that we think of is Roth conversions. This could be for anyone who’s in retirement and has low income. There are periods where we could actually convert money from your IRA to a Roth IRA. Let’s say your IRA value dropped. If we take that value here at the bottom and we move that into your Roth IRA, now when the market comes up, that value is in your Roth. And it grows tax free as the market recovers!

Harvest Capital Losses

Another thing you can do is potentially harvest capital losses. When the market’s down, maybe you have holdings that you just don’t want to hold this anymore. Or maybe you have a lot of gains and you actually need some losses to net against those gains for a tax impact. So you can say, “let’s go ahead and sell something at a loss now and then we can net that against the gains now or later.”

Keep Investing!

And then finally, one of the biggest things for anyone is really just to continue to invest. Continue to put money into your IRAs and 401(K)s! When you keep adding money, especially at these points when the market drops before your retirement, when the market goes that up, your contribution grows as fast as the market recovers! When you continue with your good financial habits, you get potential opportunities to grow your wealth even more.

Your Next Steps

And if you want a team of financial advisors to support your retirement plan, this is what we do best. Our team specializes in tax efficient retirement planning for individuals with executive compensation. So you stay on track all year, every year, reach out to our team at to schedule a 30 minute consultation.

We’ll see you there or in the next video!

Bonus: Our Free Retirement Planning Guide!

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

Should I Retire Early? The Pros, Cons, and Hidden Costs [Video]

In this video, we explore the financial pros and costs, as well as the hidden costs we see as financial advisors when clients retire early.

How to Use My Severance Package for Retirement [Video]

In this video we cover what to expect in a package, the option to negotiate, and how you can use your severance package for retirement.

Financial Design Studio, Inc.

We are financial advisors in Deer Park and Barrington, IL. A team with a passion for helping others design a path to financial success — whatever success means for you. Each of our unique insights fit together to create broad expertise, complete roadmaps, and creative solutions. We have seen the power of having a financial plan, and adjusting that plan to life. The result? Freedom from worrying about the future so you can enjoy today.