Should I Count on Social Security in Retirement?

by Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer / April 15, 2021

One of the favorite American pastimes is making light of the government. Whether that’s joking about the ogre known as the IRS or slow mail delivery from the Post Office, we’ve all had an interaction or two with government that was less than stellar. Social Security is also an easy punching bag. Many folks say, “Ain’t no way I’m going to get my Social Security the way things are going!” But sitting behind joking statements like this lies a real life, unspoken question. Namely, “Should I count on Social Security in Retirement?”

Social Security is an incredibly complex topic. There’s no way to cover all the complexities in a blog post. Instead, the goal with this week’s post is to highlight two things: 1) how important Social Security is to your retirement plan, and 2) what happens if the Trust Fund runs out.

What is Social Security Designed to Do?

The Social Security Act was passed in 1935 during the presidency of Franklin Roosevelt. America was five years into a crippling Great Depression and on the cusp of entering World War II. The purpose behind it was simple, as stated in the first sentence of the Act:

“AN ACT to provide for the general welfare by establishing a system of Federal old-age benefits, and by enabling the several States to make more adequate provision for aged persons, blind persons, dependent and crippled children, maternal and child welfare, public health, and the administration of their unemployment compensation laws…”

In short, the Social Security of 1935 and 2021 has the same basic purpose: to provide a social safety net for those unable to work, whether that’s due to age or a disability. The one big difference between then and now is that life expectancies have increased by 20 years. If you turned 65 in 1935, they didn’t expect you to live much longer. Now, people regularly live into their 80s and 90s, making Social Security as much a retirement benefit as an income safety net in old age.

Who Benefits Most from Social Security?

The way they calculate Social Security benefits means that Americans at lower income levels receive more income replacement benefit relative to what high earners get. This is by design and is a real policy goal of the Social Security program.

To see this with real numbers, we’ve created a chart showing potential Social Security benefits for a new retiree at various income levels. Each income level assumes that they had worked at the same relative wage level their entire lives. Living Expense Coverage is calculated as wages less taxes paid, which we peg at 30% all-in for Federal, FICA, State, and Local taxes.

For example, on the left side of the chart we have someone who currently earns $35,000 per year and will retire soon. After taxes, their take-home pay is $24,500 ($35,000 less 30% total taxes). We’ll assume this is the money they live on; their living expenses.

Using Social Security’s Quick Benefits Calculator, we find this person would receive $1,241 per month in Social Security benefits, which comes out to $14,892 per year.

If we compare that benefit to what they normally spend, we find that Social Security will cover just over 60% of their living expense need while in retirement. That’s nothing to sneeze at!

Notice what happens as income levels increase. Someone making $75,000 per year will receive less than 50% coverage of their living expenses from Social Security. All the way to the right we see that the percentage drops to 30% coverage for the $175,000/year earner.

The benefit you ultimately get from Social Security has little to do with what you contributed in the form of Social Security taxes. Quite the opposite, actually. Remember that the original purpose of Social Security was to offer an income safety net to those who needed it most. That’s still true today.

Your Job: Fill the Retirement Spending Gap

Financial media constantly bangs the drum about the “retirement crisis” in America. I sometimes find these claims to be self-serving. Above, we saw that Americans below the median income level (half of America, by definition) will end up getting over 50% of their wages replaced by Social Security. The hurdle to close the retirement spending gap isn’t huge.

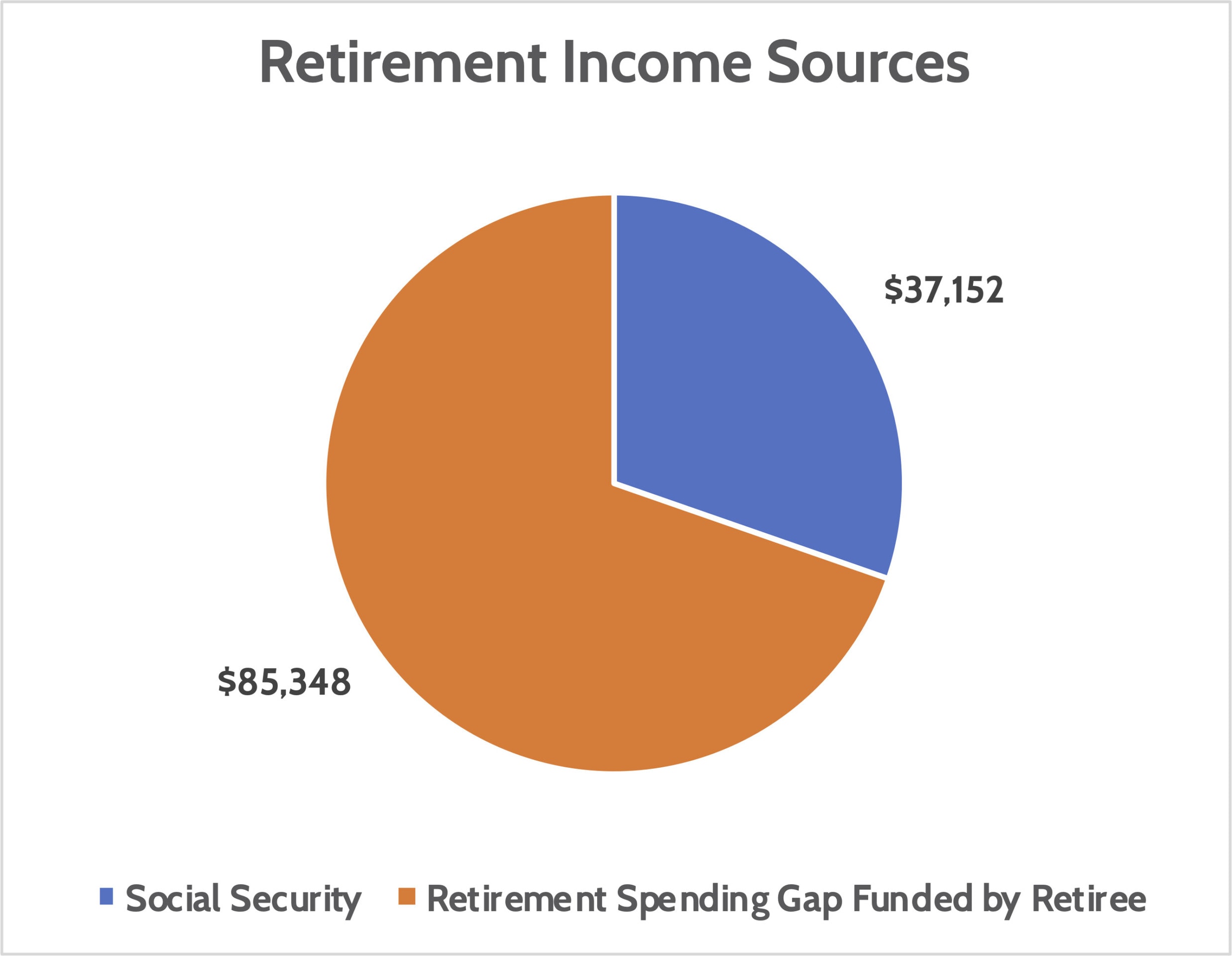

For higher income earners, the story is different. Using the $175,000/year earner above, Social Security will cover 30% of their $122,500 annual spending needs. But that means it’s up to the retiree to cover the other 70%.

Putting this in simple terms: you’re responsible for the orange part of the chart if you want to maintain your current spending patterns into retirement. Assuming investment returns of 6.0% and living expense inflation of 3.0%, this retiree would need $1,500,000 in savings on Day 1 of their retirement to fund their portion of retirement spending for 25 years.

This shows the challenge for high income earners. The higher your annual income, the less Social Security will “replace” your income.

Will Social Security Benefits Keep Up With Inflation?

We’ve seen how important Social Security income can be for your retirement spending needs. Yet we all know that living expense costs go up each year because of inflation.

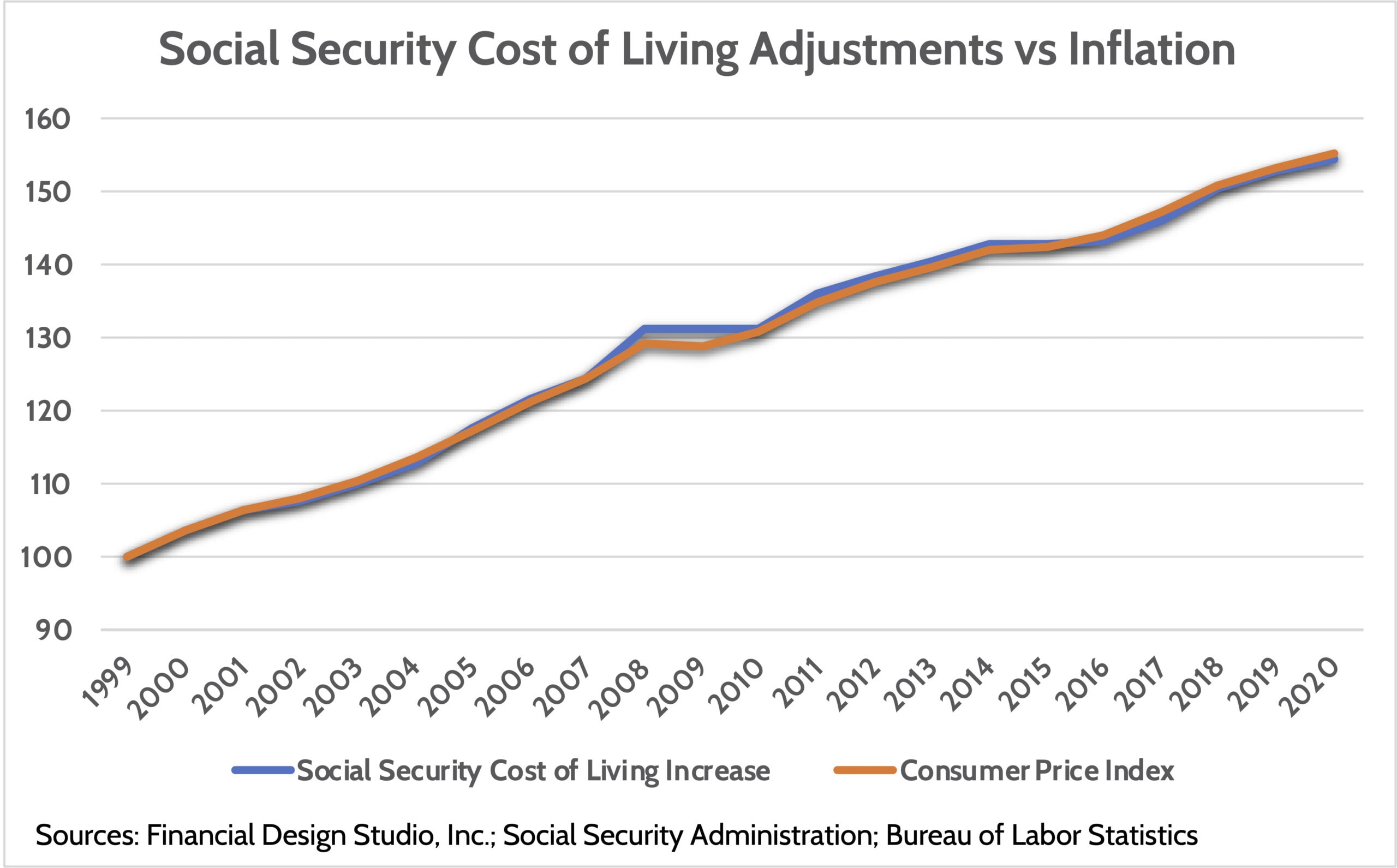

Most company pensions and insurance annuities will ‘guarantee’ a flat monthly payment for as long as you live. Social Security takes this feature one step further by giving you a cost-of-living adjustment each year. These adjustments – often called a “COLA” – maintain the real purchasing power of your Social Security income.

Officially, COLA adjustments have been doing their job. Since 1999, total Social Security COLAs have almost perfectly matched the officially reported inflation rate.

Regular readers of our blogs and newsletters will know that we’re skeptical of how the government calculates inflation. Seniors certainly understand this. For example, Medicare Part B premiums have more than tripled since 1999, rising almost 6% per year.

But let’s not be quick to discount the value of these COLA adjustments. They are a real, truly guaranteed benefit that only Social Security offers. A client’s Social Security income is the foundation upon which they built the rest of their retirement income plan.

Can I Count on Getting Social Security in Retirement?

Every year, the Social Security Trustees come out with a report detailing the financial health of the Social Security system. And every year, news sites are filled with headlines about how Social Security will go bankrupt in XYZ year.

I’m not going to get into the nitty gritty of the Social Security Trust and how it works because, frankly, I’m not an actuary. But here’s what’s happening. Since its inception, Social Security has taken in more payroll taxes than they paid out in benefits. They put these extra dollars into a “trust” to make the accounting work. Think of the trust as a savings account.

Recently, the level of paid Social Security benefits exceeded the amount of payroll taxes coming in the door. To keep everyone’s benefits stable, the Social Security Administration (SSA) has to dip into the pot of money set aside in the trust.

As more people retire and start taking Social Security, this dynamic (more money going out than coming in) will worsen. By 2034, the SSA expects the trust fund to be fully depleted. News organizations spin this to mean that Social Security will be “bankrupt.”

Let me be clear: Social Security will NOT go bankrupt in the sense that the news wants us to believe. When people hear “bankrupt” they naturally assume that their Social Security benefit would go to zero. That will not happen.

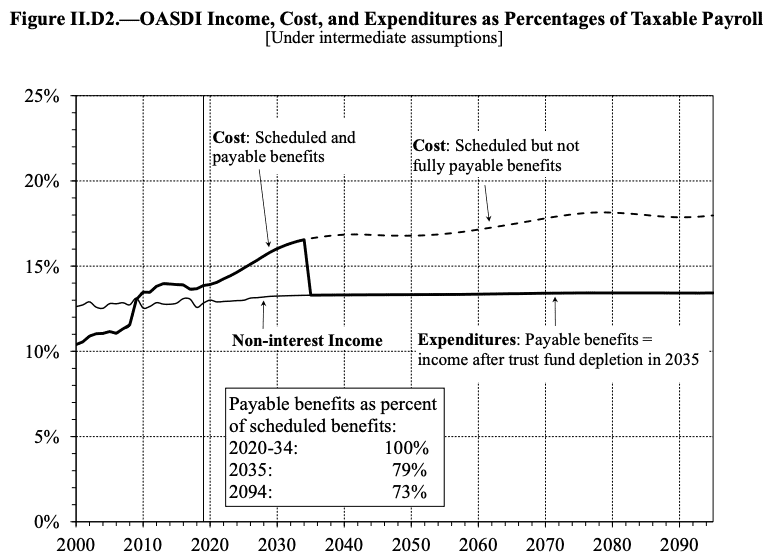

So what’s going to happen if the Trust fund is depleted? They would cut benefits to the level of Social Security taxes coming in the door. Put another way, Social Security would become a pay-as-you-go program. We can see how “bad” this outcome would be in the chart below provided by the SSA.

The worst-case scenario for Social Security is that the trust fund is depleted and Congress does nothing to fix it. In that case, monthly benefits would fall about 20-25%. A retiree getting a $1,000 monthly check would get a $790 check instead.

Don’t get me wrong. That would be a terrible outcome for people who depend on Social Security to survive. But it’s not the “zero” the media would have us believe.

Will Social Security Get Fixed?

The million dollar question is whether Congress will fix Social Security, and if so, when. I have very strong conviction about when it’ll get fixed: At 11:59p.m. the day before Social Security goes bust. This isn’t a cynical prediction, just a realistic one based on the last 30 years of American politics. Just watch.

Fortunately, the fixes for Social Security aren’t difficult. They can raise payroll taxes by a percent or two. Or they can raise the Social Security wage limit – currently at $142,800 – so higher-income folks pay more Social Security tax. They can also raise the full retirement age from 67 to something higher.

Therefore we have very high conviction that Social Security benefits will be preserved, both for current retirees and future ones. The societal costs of not fixing it are too high, and the solutions are manageable.

Building Your Retirement Income Plan Around Social Security

As you think about retirement, start with Social Security. You can go to the Social Security website and get your benefits statement online. This will give you your expected monthly benefit in today’s dollars.

Compare that figure to the amount you normally spend each month. The gap between what you’re spending and what Social Security would provide is what you need to save for.

While your income will stop on the day you retire, your living expenses won’t. That’s why it’s important to have a plan in place to replace that lost income.

When we work with clients nearing retirement, we’re looking at their entire financial picture to build a retirement plan they can have confidence in. We guide people on when to take Social Security and which types of investment accounts they should draw upon to fill remaining gaps to their spending needs. And we do this with an eye towards taxes, so you’re not paying more tax than you need to.

If you’re wondering how your retirement income plan might look, please reach out to us. We’ll ask for a Social Security statement and go from there!

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

Should I Retire Early? The Pros, Cons, and Hidden Costs [Video]

In this video, we explore the financial pros and costs, as well as the hidden costs we see as financial advisors when clients retire early.

Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer

Rob has over 20 years of experience in the financial services industry. Prior to joining Financial Design Studio in Deer Park, he spent nearly 20 years as an investment analyst serving large institutional clients, such as pension funds and endowments. He had also started his own financial planning firm in Barrington which was eventually merged into FDS.