Estate Planning Documents: What are they?

by Michelle Smalenberger, CFP® / May 16, 2017Michelle Smalenberger, CFP®

Do not hesitate to have your estate plan created! Your family is depending on it. Even a single individual or married couple with no children or assets should have an estate plan so they choose who will make their healthcare and financial decisions.

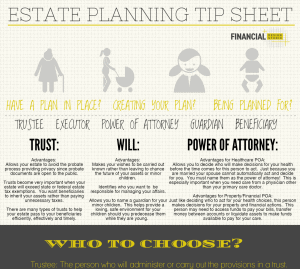

Will: A legal document that allows your assets to seamlessly be transferred to those people or organizations that you have selected. You also should name a guardian for the care of any minor children. This document allows for the management of your affairs while you are no longer living.

You avoid the probate process by having a will created, signed and in place to facilitate the necessary transfer of assets. The probate process is costly since it involves getting supervision from the court to gather your assets, pay debts and taxes, and then distribute the remaining assets to beneficiaries

Power of Attorney for Healthcare: A document that names the individual you want to make health care decisions when you cannot do so for yourself. This document is valid while you are still alive. Typically people will name their spouse first and then someone else if their spouse predeceases them.

There are a few items to think about when choosing this person:

Can they act in a time of high emotional stress or pressure?

Do they know your wishes should they have to make a critical decision?

Does this person have experience or knowledge in the medical field?

Subscribe to Our

Blog to get this

Free Resource

Power of Attorney for Property: Like the power of attorney for healthcare, this document deals with decisions for your property and/or finances. This person may need to transfer funds between financial accounts, liquidate assets to pay bills, and access your finances to pay expenses for your care.

This document is effective while you are still alive but cannot act for yourself. For example, it may be necessary if you were unconscious or mentally unstable for long periods of time. It would be beneficial to consider people who have experience handling finances or affairs of others.

Trust: A trust document has many advantages and helps to accomplish a wide variety of goals. You can provide specific instructions for minor children or grandchildren to inherit assets at specific ages since they are too young now.

A very important reason to use a trust is when you have assets that exceed the state or federal estate tax exemption limit. This can provide for a way to pass assets to others and avoid unnecessary taxes being paid, instead of those hard-earned assets going to your beneficiaries.

An estate plan that is well drafted will tell your beneficiaries and those responsible for carrying out your wishes that you have thoughtfully and carefully chosen them to be a part of your legacy. With thoughtful planning, you can teach your beneficiaries to think carefully about how they spend or use the assets they inherit from you.

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

Strategies to Lower Your Estate Taxes [Video]

In this video, we discuss different strategies to lower your estate taxes and utilize estate documents for all kinds of assets.

Podcast Episode 28: Organizing Your Possessions (or Your Parents!) with Ashley Rapp

In this episode, Ashley Rapp, a professional home organizer, shares how she helps her clients organize their possessions before transitions.

Michelle Smalenberger, CFP®

I have a passion for helping others develop a path to financial success! Through different lenses on your financial picture, I want to help create solutions with you that are thoughtful of today and the future. I have seen in my life the power of having a financial plan while making slight changes of direction from time to time. I believe you can experience freedom from anxiety and even excitement when you know your finances are on track.