What’s Next for Stocks and Bonds in 2025?

by Financial Design Studio, Inc. / December 16, 2024

2024 had been a pretty good year for investors. Stocks have posted another strong year of above-average returns. Bonds haven’t done as well but are at least eking out a small gain after generating historically poor returns from 2022 to mid-2023. The question is what’s next for Stocks and Bonds in 2025? The US elections brought some policy clarity to the outlook, but the market has already discounted much of this positive news. This quarter’s newsletter will explain everything we are currently looking at and what we think it means for investors in 2025.

Strong Stock Market Returns in 2024

Anyone opening up their 401k statements or online brokerage accounts is likely pleasantly surprised by how much the value of their investments have gone up this year. It’s been an exceptional year! While the largest stocks – often called the Magnificent 7 of Apple, Amazon, Google, Meta, Microsoft, Nvidia, and Tesla – have once again been the stars of the show, other parts of the market have contributed strong returns.

On a long-term basis, stocks have averaged returns of 9-10% per year while bonds generate returns of 4-5% per year. Other than Developed Markets Stocks (mainly European stocks), returns for stocks are well-above the average. Bonds have been weaker, but High Yield bonds have posted strong returns.

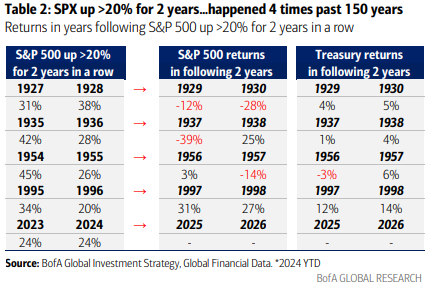

At the risk of spoiling the party, I should note that it’s rare for the S&P 500 to be as strong as it has been the last two years. In fact, 2023 and 2024 mark only the fifth time ever that the S&P 500 has generated 20%+ returns for two consecutive years. The chart below from Bank of America shows how the markets did in Years 3 & 4 after two straight years of 20%+ returns.

Two of those instances happened during the Roaring 20s and the Great Depression. Putting those aside, we can look at the 1950s and 1990s as guideposts. The 1950s had two strong years followed by two years of muted stock returns. However, the 1990s saw strong returns followed by more strong returns to close out the Millennium. Maybe the current Artificial Intelligence (“AI”) boom is more like the 1990s than the 1950s? Time will tell. The stock market returns of the last two years are historically unique.

What’s Causing Stocks to Increase so Much?

Over the last decade there has been a vigorous debate about what has been driving stock prices and concentration in major indices, such as the S&P 500. There’s no doubt that the pool of stocks driving markets higher has dwindled. Over ⅓ of the S&P 500 index comprises just 10 stocks, the highest level of concentration since the early 1970s.

What’s driving this? There’s a strong view amongst pundits that the increase in passive index investing is driving market concentration. ‘Passive investing’ means that you own a fund that owns the same stocks at the same percentage weights as the referenced stock index. There’s no stock picking going on. When you invest $100 into an S&P 500 index fund, $7 of that goes into Nvidia, $7 into Apple, $6 into Microsoft, and so on. It turns into a “winner take all” dynamic.

Fundamental stock investors can only stand by and wring their hands as the stocks of smaller, undervalued companies are being ignored because the biggest companies get all the investment dollars from passive investors! The situation for these fundamental investors has gotten so bad that a funny meme has emerged, showing someone throwing a copy of Benjamin Graham’s Intelligent Investor book into the garbage. This book is the “bible” of fundamental stock investing.

But is the story of the stock market really about passive investing?

Strong Earnings Drive Strong Stock Performance

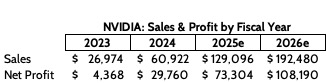

Lazy fundamental investors want to blame passive investing for the market’s concentrated returns. But as a fundamental investor myself, I think the story is much simpler – and logical. This answer helps us understand what to expect for stocks and bonds in 2025. Let’s look at the poster child of the AI Boom, Nvidia. They are the major supplier of chips that run AI models. As recently as the end of 2022, Nvidia wasn’t even in the top 10 constituents of the S&P 500. Now it’s the largest stock in the index with a weight over 7%! What happened?

The answer is quite simple: Nvidia’s sales and net profits have exploded on the AI build-out. The growth is quite remarkable, actually. In the last two years, sales have increased by 375% and profits have increased by over 16 times. It’s one of the greatest fundamental stories ever and is why the stock is now the largest in the world. Other Mag7 stocks have seen significant earnings growth as well.

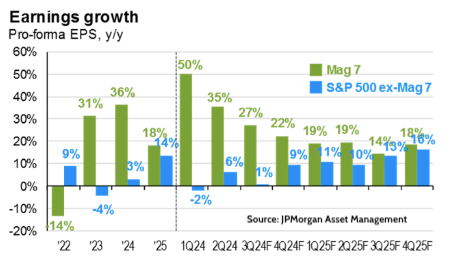

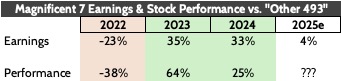

The message here is that the strong performance of Mag7 stocks is directly tied to their relative earnings strength. For example, in 2022, Magnificent 7 earnings “growth” was 23% worse than the other 493 stocks in the S&P 500 index. Not surprisingly, Mag7 stocks underperformed the Other 493 stocks by -38% (red shaded, below).

Heading into 2025, earnings growth is expected to converge for the Mag7 and “Other 493” stocks. Does this mean a broadening out in performance?

Valuation of Stocks and Bonds in 2025

My view is that valuation is going to matter for stocks and bonds heading into 2025. Investors dispense with stock valuations when there’s a major growth story taking place, as has been the case with AI. But the AI story is becoming well known and is coinciding with better earnings prospects for other companies.

The valuation most investors focus on is called the “price-earnings ratio.” It compares the value of the company to the earnings it generates. Taking the Nvidia example above, analysts expect the company to earn $2.95/share in profits this year. At the current stock price of $142, Nvidia’s price-earnings ratio is 48x.

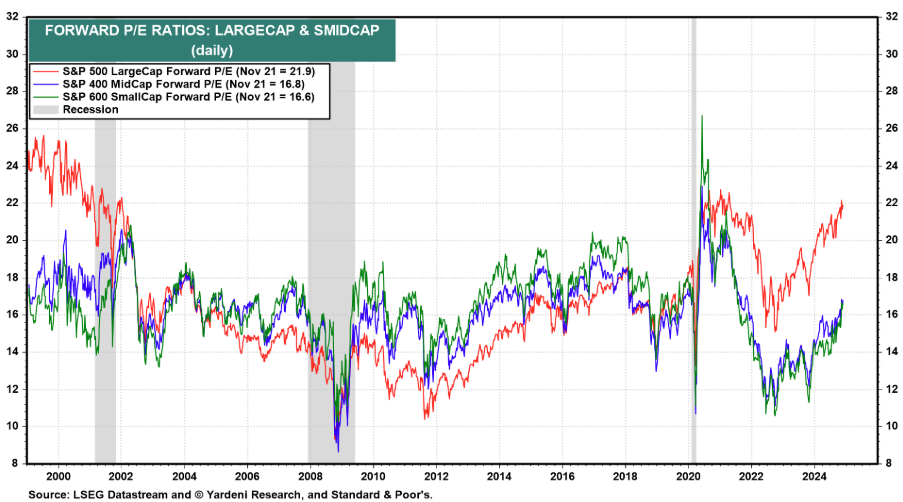

We monitor the valuation of several parts of the stock market. For example, we can look at the valuation for Large-cap stocks, represented by the S&P 500 (red line, below); Mid-sized companies (blue line) and Small-cap stocks (green line.) The chart below is from Ed Yardeni Research and goes back to the late 1990s. If we took this chart at face value, we’d say that large-cap stocks are expensive, while mid and small-cap stocks are fairly valued.

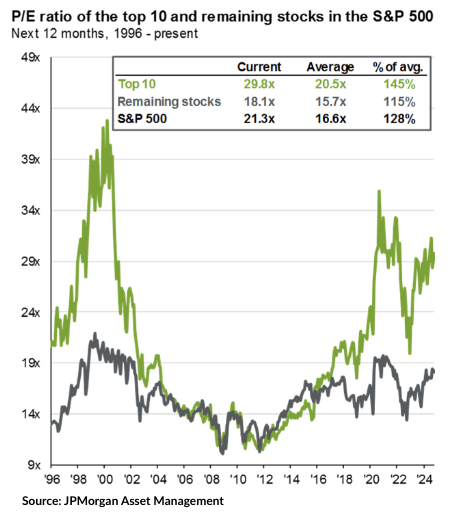

Indeed, large cap stocks haven’t been this expensive since the late 1990s bull market and for a brief period after COVID. But there’s more to the story than that. If you strip out the valuation of the top 10 stocks in the large-cap S&P 500 index and compare that with the remaining stocks in the index, you find that the top 10 stocks are very expensive while other stocks show good valuation.

Understanding the Valuation of the Stock Market

There are two concepts I’d like for you to take away from these valuation charts.

First, when a company’s stock is expensive, the stock is in “prove it” mode. Investors have rewarded your stock with a high valuation because of expectations of above-normal sales & earnings growth. The company must maintain (or do better) than those growth expectations to keep that high valuation. Any hint that growth is slowing or not playing out as expected will cause a lower valuation and lower stock price. In my view, 2025 is a major “prove it” year for AI stocks. The market has so far driven these stocks higher on hope for AI-related revenue growth, but there must be more visibility of that happening outside of Nvidia.

Second, we can see that for the rest of the market, valuations are quite reasonable. Whether we look at the “Other 490” or mid-sized stocks or small-sized stocks, the picture is the same: valuations are close to long-term averages. With earnings prospects for these companies picking up for 2025, it’s possible that these stocks will have a “catch-up” year.

That would be welcome news for diversified investors.

Don’t Ignore the Warren Buffett Factor

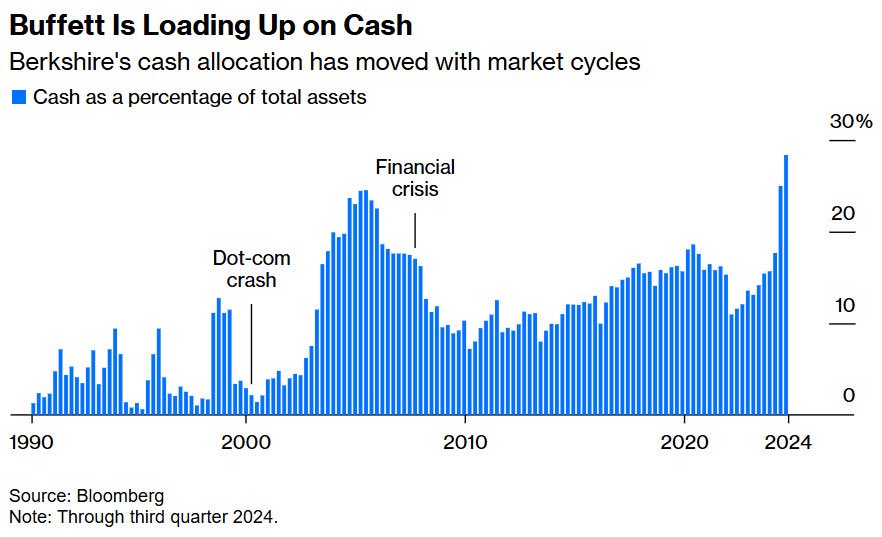

There’s one last thing I’d like to talk about before closing this last newsletter of 2024. Even at Age 94, investors closely watch what Warren Buffett is doing with Stocks and Bonds in 2025. This chart shows how much cash Buffett is holding at Berkshire Hathaway relative to the size of his investment portfolio. Somewhat amazingly, the cash level today – almost 30% of total investments – is the highest it has been since 1990.

We can look back to previous periods where Buffett was significantly raising cash (i.e. selling stocks.) The first was in the late 1990s, just ahead of the Internet bubble bursting in 2000. The second instance was in 2005-2006, just ahead of the Great Financial Crisis of 2008 & 2009. In both these cases, Buffett was “early” in making these calls, but was eventually proven right.

I bring this up because for at least the 10th time during my career, some other high-profile investor is being touted as the “new Warren Buffett.” Today’s investment superhero is Michael Saylor, Chairman of a company called MicroStrategy. He has been aggressively issuing debt to buy Bitcoin. So far, that’s worked great, as Bitcoin prices have surged towards $100,000.

But the investment roadside is littered with “next Warren Buffett” types. These folks made a big bet on whatever investment was in a bubble, only to blow up spectacularly after that asset dropped. As Bitcoin has surged to new highs, commentators have once again brought out the “Buffett is too old to understand” headlines. Time will tell if markets will vindicate Warren Buffett will once again.

What’s Next for Stocks and Bonds in 2025?

As we saw at the outset of this newsletter, stocks have posted rare back-to-back 20% return years. The post-election vibes are nothing but bullish for the economy and stocks and bonds in 2025. Whenever consensus becomes this convinced of a narrative, it’s a great time for level-headed investors to see where they may be wrong.

We’ve established that earnings prospects are improving and valuations are reasonable for most of the thousands of stocks that trade in the United States, large and small, alike. This provides hope that they will perform well if the economy continues its strong pace of growth.

But if the economy runs into trouble, the “good” news is that most U.S. stocks are NOT priced for perfection. That provides valuation support to those companies. The same might not be said for AI-related stocks that are priced for strong growth to continue several more years.

Finally, I have mentioned little about bonds, but my view is that interest rates will head lower in 2025. Some investors are worried about inflation making a comeback. I don’t share that concern, yet. The ingredients just aren’t there, with monetary policy currently tight.

Your Next Steps

Our strategy for owning well-diversified portfolios for clients remains in place. We know there are periods where returns don’t keep up with the headlines. But this strategy also means that when markets have off years – as they will – client portfolios are insulated from having too many eggs in the wrong basket.

Financial plans are based on long-term projections of income, expenses, inflation, and investment returns. And we all know that life is totally unpredictable. Having a well-structured, disciplined, investment process is critical to providing some predictability to something that’s unpredictable by nature. That’s how we serve you, the client, and we are grateful for your support!

If you don’t have an investment strategy that you know you can depend on in the ups and downs, reach out! Our team’s goal here at FDS, it’s that our clients feel confident about their future. We would love to bring this confidence to your family’s finances.

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

Outlook for Interest Rates and the Budget Deficit

Explore the link between interest rates and the U.S. budget deficit, and how the Iran War and the Fed are impacting stock and bond markets

Leaving a Legacy by Thinking Two Generations Deep

With your finances, you have the opportunity to impact generations after you. In this article, we discuss the strategies for leaving a legacy!

Financial Design Studio, Inc.

We are financial advisors in Deer Park and Barrington, IL. A team with a passion for helping others design a path to financial success — whatever success means for you. Each of our unique insights fit together to create broad expertise, complete roadmaps, and creative solutions. We have seen the power of having a financial plan, and adjusting that plan to life. The result? Freedom from worrying about the future so you can enjoy today.