Navigating Economic Paradoxes

by Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer / February 14, 2024

“Anything can happen.” That best sums up the view many have about the economy and markets as 2024 gets underway. Investors know that market performance is (usually) tied to the performance of the economy. That’s why there are so many economists employed by Wall Street banks! The problem is that in 2024 there are more economic paradoxes – conflicting views, indicators, and puts & takes – than I can remember in a very long time. This article reviews key market influences, the Federal Reserve, bond markets, labor markets, corporate debt, US deficit, and the potential for recession. Here’s what you need to know as we try to navigate these economic paradoxes.

The Powell Pivot

One of the biggest influences on stock and bond market performance is the constant game of cat and mouse between the markets and the Federal Reserve. Markets are always anticipating where interest rate policy is going to go. Put simply, “rates higher” is bearish for stocks and bonds while “rates lower” is bullish.

By late Fall 2023, the bond market had anticipated 3-4 quarter-point (0.25%) interest rate cuts by the Fed in 2024. Fed Chair Jerome Powell dutifully walked on stage in early December and reiterated the Fed’s 18-month talking point: interest rates would stay higher for an extended period to fully defeat inflation. The bond market didn’t back off its rate cut expectations.

Fast forward two weeks – in what is known as the “Powell Pivot” – Fed Chair Powell got back on the podium and showed for the first time that up to three interest rate cuts were on the table for 2024. Stocks and bonds surged on the news.

The policy shift was an enormous surprise. Not only because it contradicted what they had said two weeks earlier, but because the economy continues to be quite strong. A robust economy keeps consumer demand high and labor markets tight, two key contributors to the inflation we’ve seen since 2021. Is Powell premature in declaring, “mission accomplished?”

Bonds Versus the Strong Economy

Since the mid-December pivot, we’ve received three key economic data points that suggest the war on inflation is far from over:

- December jobs growth came in much stronger than the market had expected.

- Inflation numbers came in higher than expected, with prices rising +3.4% in the year ending December 2023, well-above the Fed’s 2% inflation target.

- Economic growth in the fourth quarter of 2023 topped expectations, growing +3.3% versus the previous year.

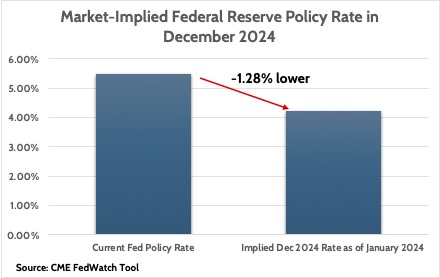

Hot jobs. Hot inflation. And hot economic growth. A year ago, stock and bond markets would’ve received such data poorly, discounting even higher Fed interest rates. But, no longer! The bond market is now pricing in FIVE to SIX quarter-point rate cuts by the end of 2024, taking rates down from 5.50% today to close to 4.00%. More rate cuts than they were pricing in prior to the Pivot.

Markets are not always right. But the divergence between (lower) rates and strong economic data is hard to ignore. I see two potential paths of resolution.

Bond Market and Economic Paradoxes

One possibility is that the bond market is right. If the case for even more rate cuts being priced in by the bond market is correct, then it might suggest that the economy is not nearly as strong as data shows. This isn’t uncommon. Often, right before recessions, the data looks great, but underneath, things aren’t all well with the economy. If this scenario plays out, then the stock market is susceptible to a shift towards negative economic news.

If the bond market is wrong, and the economy continues to defy expectations by staying strong, then the bond market will have to reprice higher rates. The risk of a second wave of inflation would be high. This would likely be a headwind to stocks.

The Bond vs. Economy cross-current is probably the biggest uncertainty in the market today. I favor the first possibility, and that informs our wealth management process. Too many times when I’ve seen markets acting differently to the news than they “should,” it’s for a good reason. This is an economic paradox at its finest.

Is the Labor Market As Strong as it Looks?

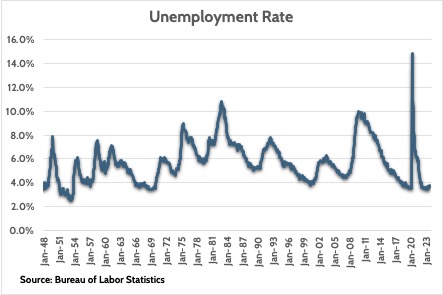

The health of the jobs market is another determinant of the economy’s health and direction of the markets. Again, we see conflicting information about what’s going on with jobs. On the surface, it looks like we have one of the strongest job markets ever, with the unemployment rate hovering near the lowest levels recorded since 1970.

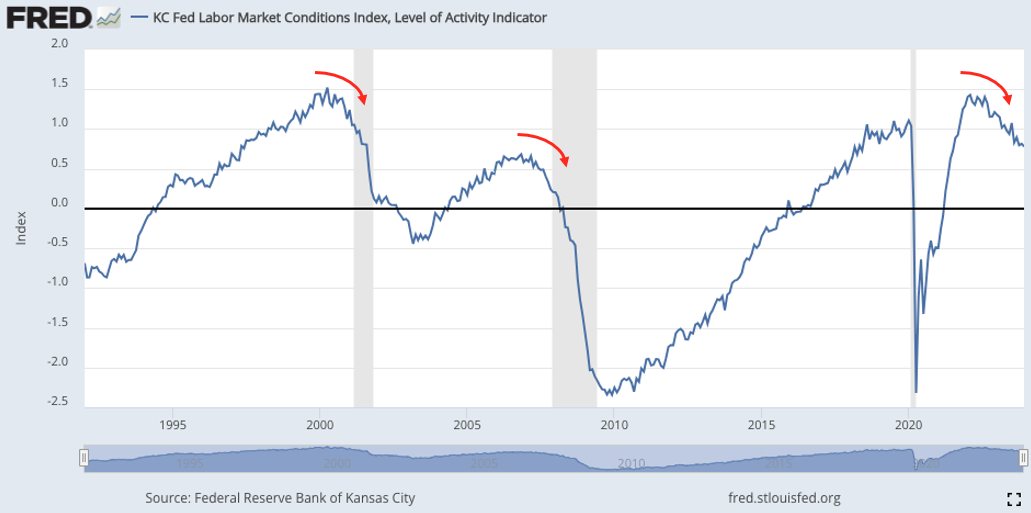

On the flip side, the Kansas City Federal Reserve publishes a labor market conditions index that has an excellent track record of predicting previous jobs downturns. Note how this index started turning downward a year before the 2001 and 2008 recessions (shaded areas.)

The health of the jobs market will be a huge determinant of the Fed’s monetary policy path and its impact on the markets. Right or wrong, many economists blame the inflation wave on the strong wage growth American workers have been able to get the last three years.

The logic of how the Fed would react to changes in the labor market is:

- Labor stays tight → Wage growth remains high → Keeps upward pressure on inflation → Fed rates stay higher for longer

- Labor market softens → Wage growth comes down → Inflation comes down faster and further than expected → Repeat of zero interest rate policy of 2010s?

The Goldilocks scenario is that the labor market softens but not too much. Unemployment rises a little but not enough to cause a full-blown recession. That seems to be what the market is currently banking on. That would be quite a “landing” for the Fed to stick.

I’ve been expecting the economy to weaken for over a year and have been wrong with that view. However, it’s clear that labor markets are not nearly as tight as they were two years ago. There are more layoff announcements and surveys of small businesses suggest it’s easier to hire for open positions.

Weaker Companies, Stronger Bond Performance?

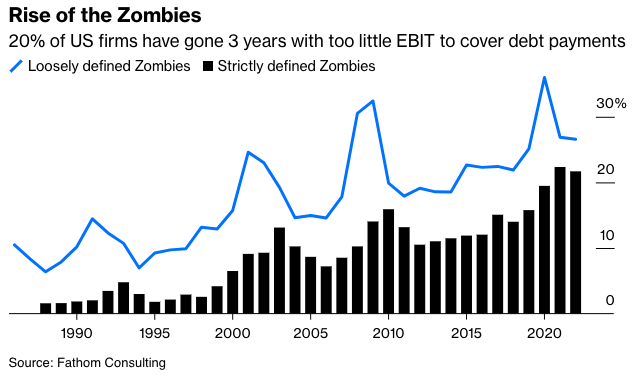

One interesting consequence of the Federal Reserve’s easy money policy from 2000 to 2019 was the rise in the number of “zombie” companies. These are companies whose interest expense on debt isn’t being covered by profits from the business for years at a time.

Abnormally low interest rates have allowed many companies to keep going when they would’ve normally gone bust in previous cycles. The Fed even took the extraordinary step of buying corporate debt in the early days of the pandemic!

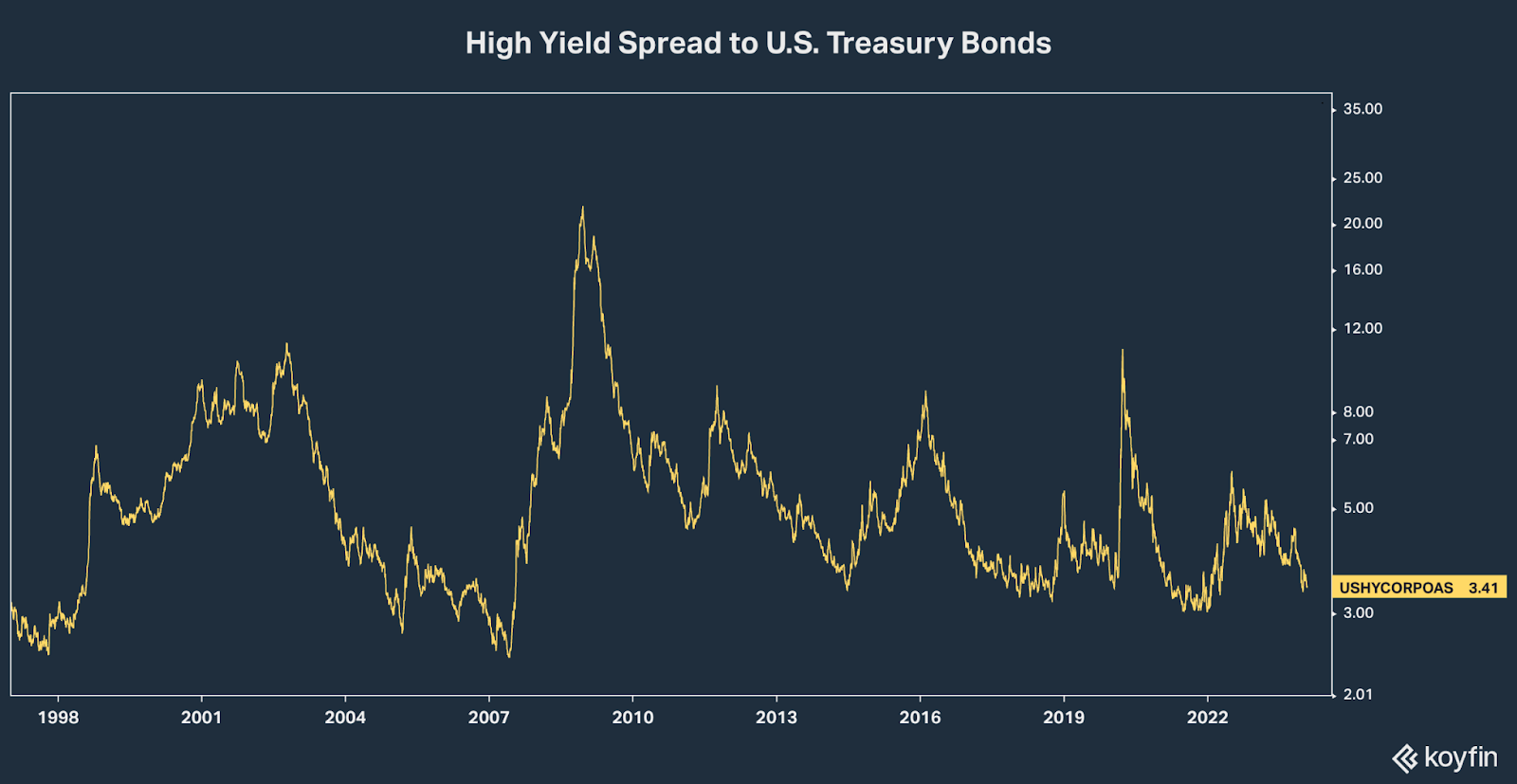

Despite the rise in zombie companies, bond yields of high yield (“junk”) companies are at some of the tightest levels relative to the yields on risk-free government bonds. That doesn’t make much sense, talk about economic paradoxes! Investors should be demanding higher interest rates from weaker companies, not less!

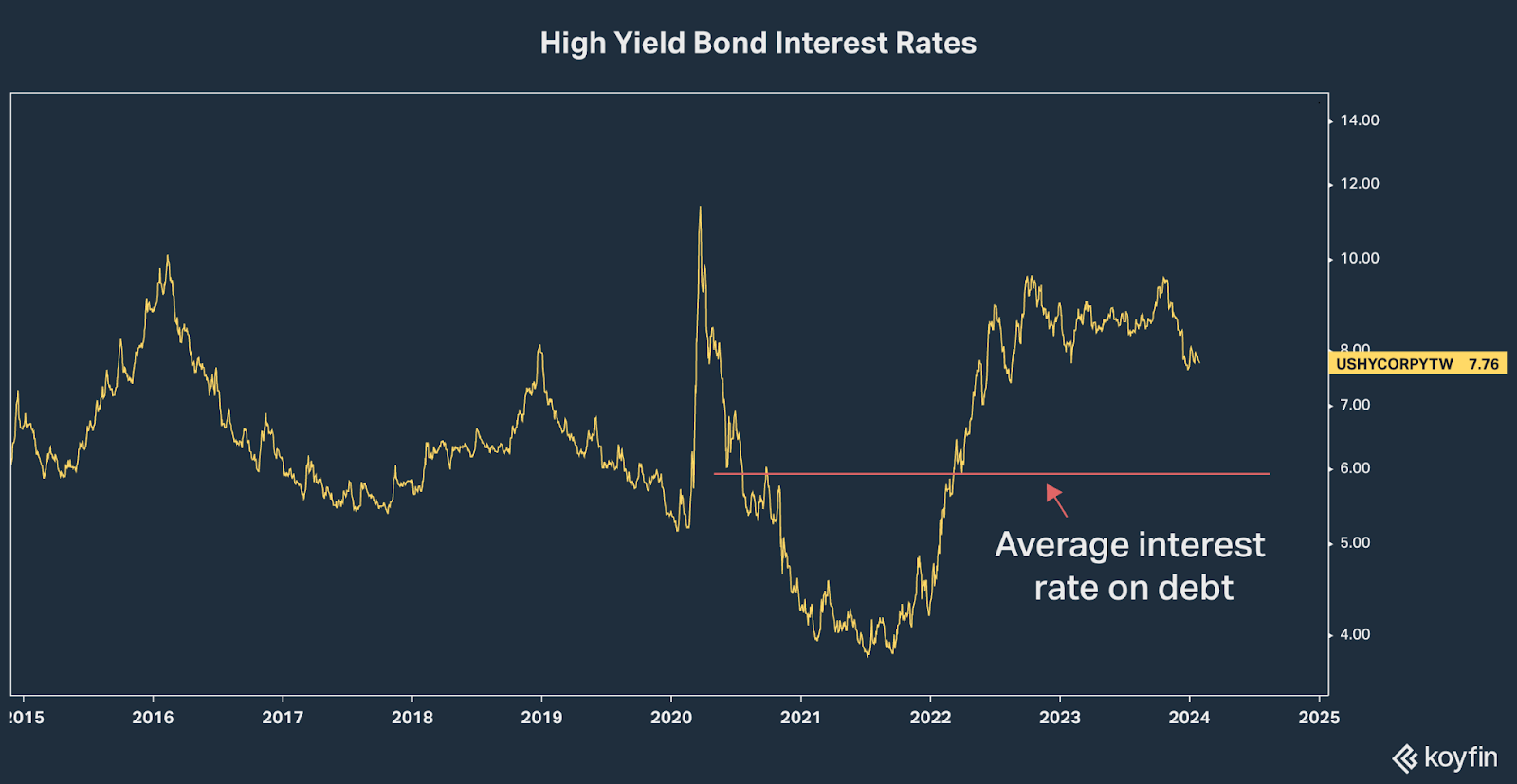

Adding to this oddity is the fact that these same companies are going to have to refinance debt at much higher interest rates than the debt that’s maturing. Currently, the average rate on high-yield bonds is 5.96%. Just like homeowners who refinanced their mortgage at low rates in 2020 & 2021, companies did the same. However, these companies will have to “roll” this debt over in the next few years. At current levels, companies would face a 2% jump in their interest rate on new debt.

There’s little logic in seeing the bond yields of structurally weaker companies facing higher debt costs being this low. Could an economic paradoxes like this be a signal that the economy is in fact much stronger than what people think? Possibly. But going back to what we talked about regarding the bond market’s expectations for interest rate cuts, that thesis is based on a weaker economy, not a stronger one. It’s another puzzling “cross-current.”

How Sustainable is the U.S. Budget Deficit?

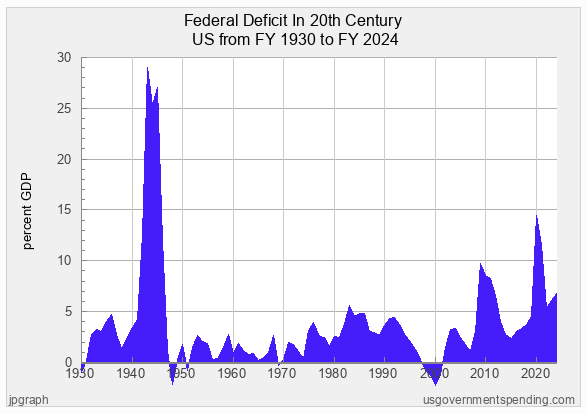

The fiscal situation of the United States is arguably the biggest wild card in the world. More investors (and voters) are asking how much debt we can pile on before something in our economy breaks. The scale of the debt being taken on shouldn’t be ignored. The U.S. is now issuing more debt relative to the economy’s size than at any point outside of major war periods or recessions.

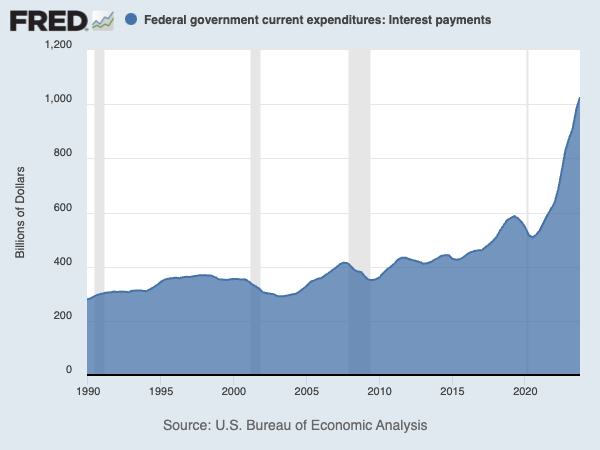

The rapid rise in U.S. government debt has been an ongoing talking point for at least three decades. We’ve seen one Congressional debt ceiling fight after another result in just one thing: more debt. The collapse in interest rates from 1980 to 2020 allowed the government to pile on more debt with little incremental cost to the budget. In fact, it cost the government roughly $300-$500 billion per year in debt interest from 1990 to 2020, an amazing fact when we think about how much higher the debt became.

Now, interest rates are higher, and the cost of servicing government debt is increasing a lot. Just in the last two years, the annual cost of servicing the government’s debt has risen from $600 billion to over $1.02 trillion! To put that number into perspective, interest costs now eat up more of the budget than Medicare spending and defense.

Inflation and Recession

All the way back in 2020 I wrote about a new economic theory – Modern Monetary Theory (“MMT”) – that was becoming popular with policy wonks. In a nutshell, this theory contends that the government can spend as much as it wants since they print the money that’s spent. It’s an awesome theory, isn’t it? All we need to do is print and spend more money and everyone will be rich!

In fact, the Achilles heel of this theory is that higher spending creates supply/demand imbalances, which leads to inflation. That’s exactly one of the economic paradoxes we’ve seen happen the last three years.

The key issue I see is that there’s no one on either side of the political aisle arguing for fiscal discipline anymore. Republicans chucked their fiscal conservatism aside during the pandemic, and Democrats have been more than happy to go along with it the last three years.

But what happens if we have a recession? Look at the deficit chart above. Spending surged in 2008 and 2020 in response to economic downturns. Are we to believe that politicians won’t open the spending spigot in the next downturn? How high will deficits be? How much higher can interest costs go before they overwhelm the budget?

To me, these are the most critical unanswered questions facing the markets today.

Navigating Economic Paradoxes

I know that was a lot to digest, so let’s summarize the economic paradoxes we’re watching:

- The bond market is predicting several interest rate cuts by the Federal Reserve even though the economy is strong and inflation is still high.

- The jobs market remains historically strong even as leading employment indicators have declined.

- Corporate credit spreads remain very bullish even though company balance sheets are weaker than they’ve been in the past.

- Interest rates on U.S. government debt remain historically low even though budget deficits have exploded higher.

Two things make the present-day situation so unique. One is that each situation seems to have a 50/50 chance of happening. Maybe things will turn out well, but there are an equal number of arguments that support things ‘breaking bad.’

Second, the consequences if things break the wrong way are profound. If we get a recession, that not only affects weak corporate balance sheets, but could lead to a budget blow-out for the government. Would bond investors revolt, sending U.S. government debt yields higher to compensate for this increased risk?

FDS Client Portfolios in Economic Paradoxes

I continue to believe that a recession is more probable than not, despite being wrong on that front for a year. As such, we’ve “tilted” client portfolios towards owning stocks and bonds of higher quality companies. For stocks, favoring funds that invest in companies with strong balance sheets and cash flows. For bonds, owning more A-rated corporate debt than the debt of companies rated lower than that.

If we get a recession, there will probably be opportunities to buy riskier stocks and bonds. We’re not wedded to a single view. When the facts change, we’ll change our view accordingly.

This is one of the key values of getting ongoing investment management through a financial advisor. We watch the economy and markets every day. Sure, young people in their 20s and early 30s can “set-and-forget” a simple passive portfolio and be fine. But as you get closer to retirement, you really don’t want to risk making an investment mistake. There are fewer years of income available to make things up if there is a mistake.

Ongoing management through FDS gets you a tax-efficient, low-cost portfolio that’s tuned into your unique goals. We educate and communicate with clients regularly, like this article on navigating this economic paradoxes. This is so you’re knowledgeable about what’s going on and how that affects your portfolio. All while we actively monitor and manage investment risks for you. If you are interested, learn more about our process!

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

How Will DOGE Impact the Market and Economy?

The Department of Government Efficiency “DOGE” is expected to have a significant impact on markets and the economy. For starters, it’s possible that a significant cut-back in spending will create a recession. We explore this possibility, along with other ways that DOGE could impact the U.S. budget deficit, Social Security, future tax rates, and more....

Do I Own Too Much Company Stock?

Do I own too much company stock? Corporate executives have lots of opportunities to accumulate stock in their company. Stock-based compensation and employee share purchase plans are some of the ways an executive can build wealth in their employer. But how much company stock is too much? This post helps you assess exactly how much...

Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer

Rob has over 20 years of experience in the financial services industry. Prior to joining Financial Design Studio in Deer Park, he spent nearly 20 years as an investment analyst serving large institutional clients, such as pension funds and endowments. He had also started his own financial planning firm in Barrington which was eventually merged into FDS.