So no matter what you read, what you listen to, you probably have heard max out your 401K. Put away money into retirement accounts. Max out maybe even your Roth IRA contributions.

That’s all good advice, if you take it completely blind. But how many times have we taken advice blind, only to find after the fact that we really hurt ourselves?

My goal in this video is really to talk about the Roth IRA contributions. And how you can follow that guidance blindly, and actually end up hurting yourself.

So there’s different accounts that you can contribute to.

401K

401K, that’s just coming out of your paycheck. There’s no limit on how much you make. The only limit is you can put away a certain amount and that’s capped for 2019. That’s capped at $19,000, or $25,000 if you’re over age 50.

Traditional IRA

For Traditional IRA, let me add it right now –the other Roth IRA– those are based on couple different rules. Of the IRAs in general, you can only contribute to if you have earned income.

So earned income, what is it and what isn’t it?

First of all, it isn’t investment income, so interest or dividends. It’s not rental income. It’s not retirement income. So it is things like salary and wages. And if you have that, you can make a contribution up to the limit.

Your max was $ 5,500 per an individual in 2018 and today it is $6,000 per individual in 2019.

If you’re overage 50, you can put away more.

Roth

Now with a Roth account, the difference here is it’s all after tax. So any money in this account is growing tax free. So naturally, the government won’t have future tax revenue. So they’re going to limit how much you can put in. They’re going to limit it based on how much you make. And if you make too much, they’re going to limit how much you can even put in then.

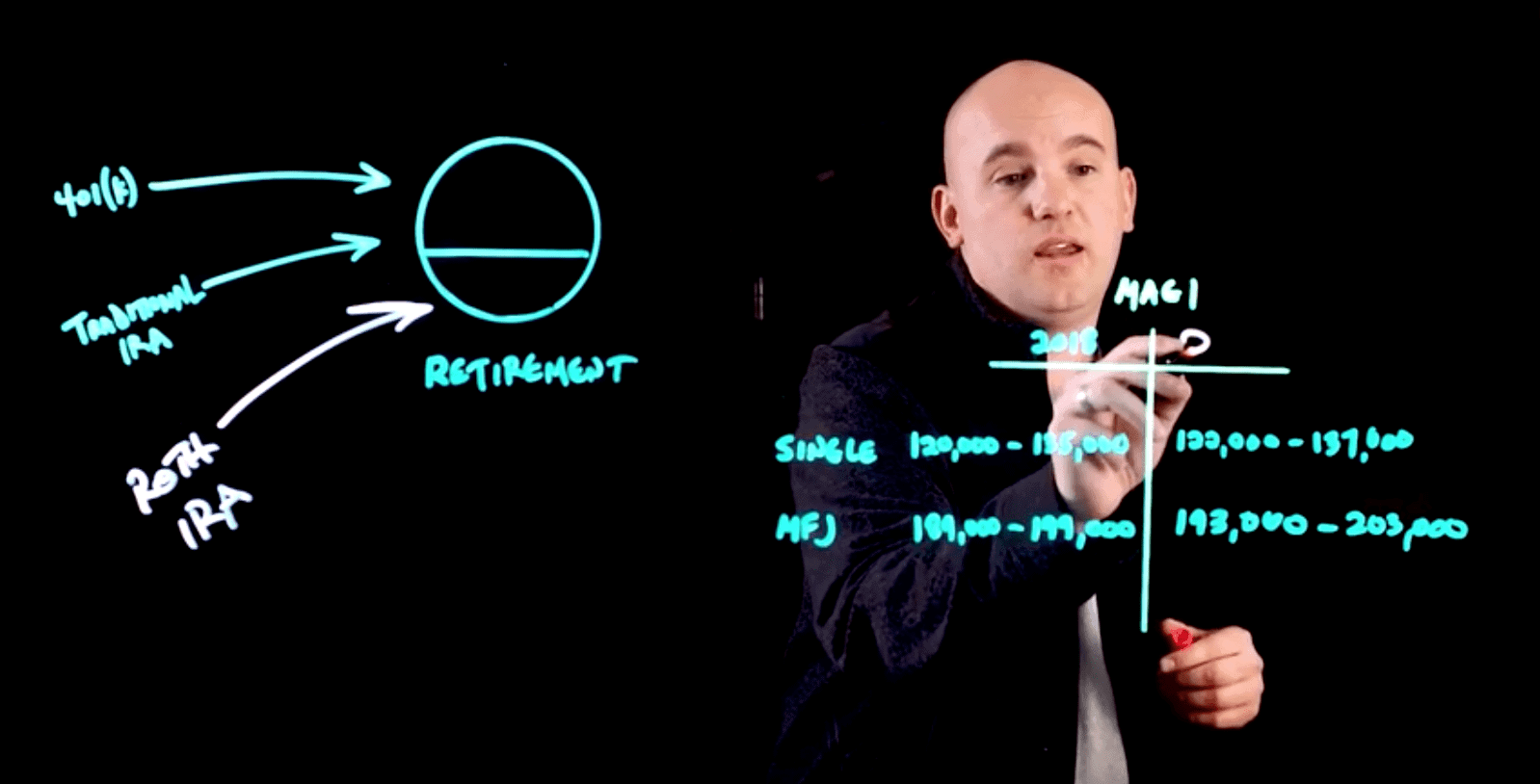

Shown in the video are some tables that’s based on your income.

Now a modified adjusted gross income. So for 2018, 2019 here are some rules. At 50 years old, you may have put in $6,000 for 2019. But when you actually finalize your return, you look at your income. Whether you’re single or married, and if your income is below these amounts, shown in the video, you’re fine.

If it’s between these amounts, maybe a portion of it isn’t allowed. And if it’s over these amounts shown in the video, it’s in excess or ineligible to make those contributions.

So here’s an example of over contributing:

You put in $6,000. You find that at the end of the year you’ve made $210,000, you and your spouse together. That means you’ve over contributed.

So none of this is able to be contributed, or put in. It’s all what’s called in excess or ineligible contribution. See at that time that you find that you’ve put into too much, that’s not eligible, that’s in excess, you have three options.

The first one, is to take that money back out. That would be step number one. Step number two, is to apply it to another year. Meaning move it to a future year. And the third option, is to re-characterize it.

Essentially make it, or move it, from the Roth account to the Traditional account. Because with the Traditional account, you can never not contribute. It just may not be tax deductible. With the Roth account, you are limited in what you can put in.

So all that to say this:

1. If you want to put money into a Roth account, first realize what your income is going to be.

2. Make sure that the amount that you’re putting in is eligible, that it’s not in excess.

3. And if you’ve found that it’s in excess, work with a professional.

Make sure that you know what needs to come out or what you need to do. Because any contributions that are in excess are penalized.

We are financial advisors in Deer Park and Barrington, IL.

A team with a passion for helping others design a path to financial success — whatever success means for you. Each of our unique insights fit together to create broad expertise, complete roadmaps, and creative solutions.

We have seen the power of having a financial plan, and adjusting that plan to life. The result? Freedom from worrying about the future so you can enjoy today.