Federal Student Loan Repayments are Resuming

by Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer / June 21, 2023

It’s been over three years since COVID washed ashore in the U.S. Since then, there have been significant changes to the federal student loan program. One of the first policy moves by the government was putting all federal student loan repayments on “pause.” The government extended these pauses several times but are finally ending thanks to the recent debt ceiling agreement reached by President Biden and Congress. How will this impact the over 40 million student loan borrowers? This week’s blog covers everything borrowers need to know about federal student loan repayments resuming.

How Big is the Student Loan Problem?

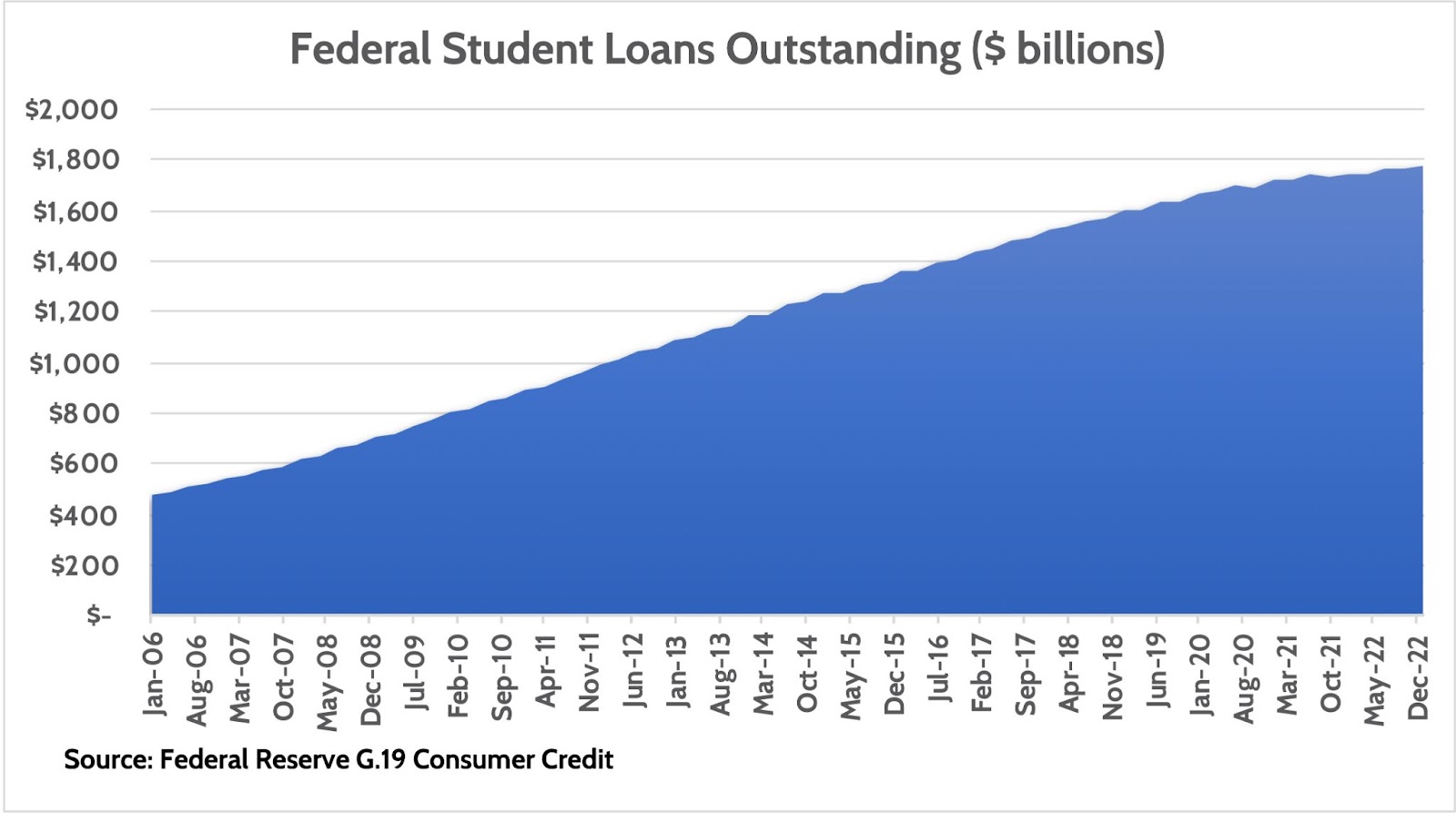

Many readers of this blog might not have student loans and think the issue doesn’t affect them. But it does! Like it or not, our government has extended a huge subsidy to both borrowers and (expensive) colleges alike. As of early 2023, total federal student loans outstanding were $1.7 trillion. Compare that to $26.5 trillion of total economic output of the United States each year, and it’s a big number!

Another point to understand about federal student loans is that they can hardly be called “loans” anymore. As 99% of us understand “loans,” you take out a loan intending to pay it back. However, the Education Department has made so many changes to student loan repayment rules – all in the name of making loans “affordable” – that hardly anyone takes out a student loan these days expecting they’ll have to pay all the money back. Hence, this crisis is here to stay.

Given all the changes in student loans since COVID, this article will take on a Q&A format to get through as many questions as possible.

When Do Federal Student Loan Payments Resume?

Student loan payments – on pause since March 2020 – will resume September 1, 2023. This is the date that was agreed to between President Biden and Congress as they wrangled over the debt ceiling a month ago.

Prior to the deal there was speculation the government would “pause” repayments once again. But the debt deal agreement put an end to that speculation. Payments will restart for real in September.

How Much Will Payments Be?

From what we’ve learned, federal student loan repayments will resume just as before the pause. Each borrower’s payment will depend on the repayment plan they signed up for before COVID, unless they’ve changed (or change) repayment plans before September.

The good news is that the government didn’t keep accruing interest on loans over the last three years. So current loan balances are the same as what they were three years ago.

Unless a borrower has changed repayment plans, had loans forgiven, or taken out new student loans since 2019, their payment should be very similar to what it was before the pause.

What About the Newly Proposed RE-REPAYE Repayment Plan?

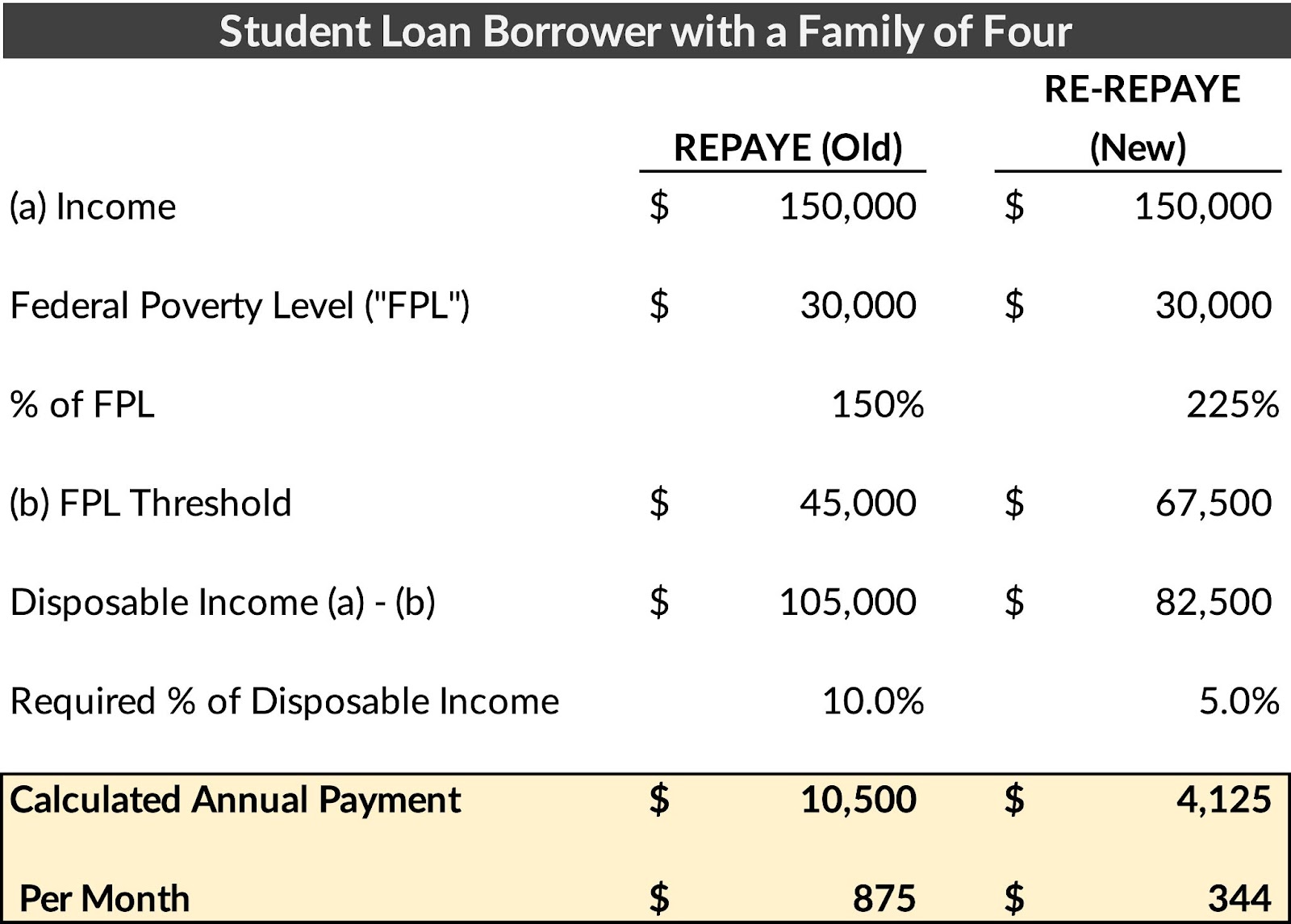

In January 2023, the Biden Administration proposed another income-driven repayment plan (“IDR”) which would change the current Revised Pay As You Earn plan, known as “REPAYE” for short. This new plan is being referred to as the RE-REPAYE plan.

The new repayment plan would lead to a dramatic reduction in required loan payments. It would:

– Increase the income threshold required before having to make any payment, from 150% to 225% of the Federal Poverty level. This means that a single individual making less than $32,805/year wouldn’t have to make any payment towards their student loans. Effectively, their “payment” – which would still count as a payment – would be $0/month.

– Lower the percentage of disposable income that would be required to be used towards student loan repayments. Borrowers with undergraduate loans would be required to use 5% of their disposable income towards student loan repayments while graduate loan borrowers would be required to use 10%. The current standards required 10% and 15% of disposable income, respectively.

– Stop the practice of adding unpaid interest to the borrower’s loan balance, called “negative amortization.” Because the calculated payments on IDR plans are often less than the required interest to be paid each month, the difference was added to the borrower’s loan balance. This led to a ballooning of loan balances for people enrolled in IDR plans. Interestingly, Congress made this practice illegal for credit card companies and mortgages a decade ago, but allowed the practice with student loans.

– Reducing the number of payments required towards eventual loan forgiveness.

This new plan would be hugely beneficial to many borrowers. We compare the required student loan payment under the old REPAYE plan and the new REPAYE plan below.

Unfortunately, this new plan won’t be available to borrowers when repayments start in September 2023. The effective date isn’t until early 2024.

What’s the Status of the $10,000 Student Debt Relief Program?

In 2022, President Biden’s Education Department rolled out a student debt relief (loan forgiveness) program that would cancel up to $10,000 of loans for many low-income borrowers. That amount could be as high as $20,000 for Pell Grant recipients.

Many states moved to block the program, eventually sending the case to the Supreme Court. As we’re writing this article (June 2023) rumors swirl they will make a ruling on the case in the next week.

If approved, a single borrower that made less than $125,000 in 2020 or 2021 ($250,000 for married borrowers) can apply to have loans canceled. Loans that are forgiven would not be taxable at the Federal level, as is often the case. However, some states might tax the amount forgiven.

If the Supreme Court shoots the case down, then the program won’t move forward.

Have Student Loan Forgiveness Programs Gotten Easier?

In 2021 and 2022, the Education Department changed the rules of the popular Public Service Loan Forgiveness program. “PSLF,” as it’s known, allows borrowers who work in certain government and nonprofit organizations to have student loans fully forgiven after 10 years of repayment.

An April 2022 ruling relaxed PSLF rules and allowed many borrowers to achieve loan forgiveness. As of March 2023, borrowers have had $34 billion of loans forgiven and discharged under the PSLF program.

Borrowers who work in the private sector and don’t qualify for PSLF aren’t out of luck. Under existing rules, the government will forgive student loans on any remaining loan balance after 20 years (25 years for graduate school loans). The problem is that the rules are stringent. You have to have the right type of loan and be on the right type of repayment plan and make the right payments. It’s very confusing.

But like the PSLF program changes made two years ago, the Education Department has proposed a relaxation of the rules to make it easier for borrowers to get loans forgiven, including:

– Counting payments made under any repayment plan, not just the ones they previously required borrowers to be on;

– Allowing missed or underpaid “payments” to count as payments towards forgiveness

Similar rules changes significantly increased the number of people that got forgiveness under PSLF. It’s likely that loan forgiveness under non-PSLF programs will increase because of these rules changes, even if eventual forgiveness is still many years away.

How Will Resumption of Student Loan Repayments Affect the Economy?

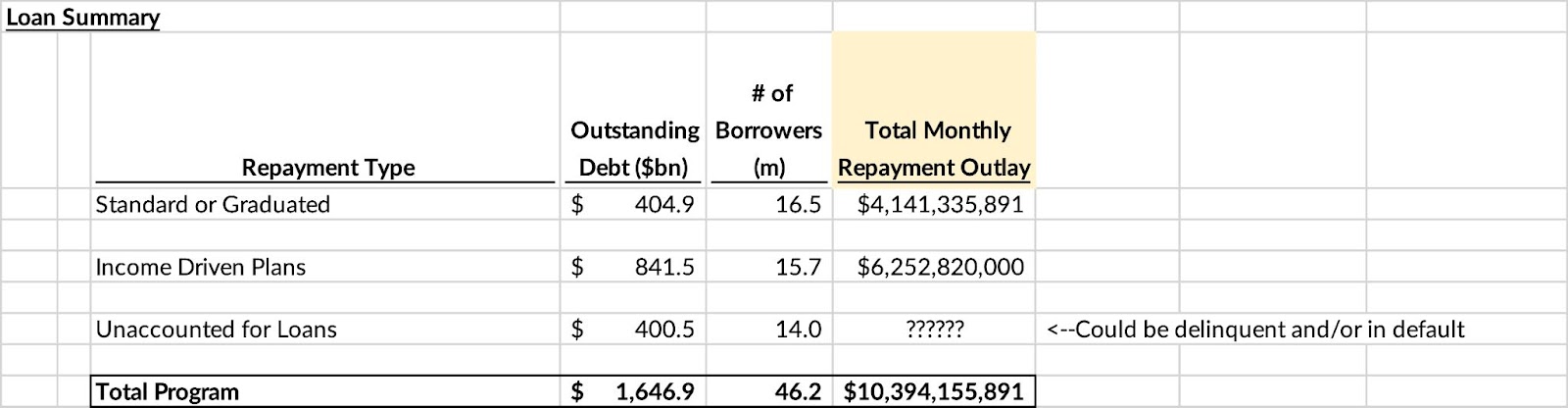

As Federal student loan repayments begin again, a natural question is how much money borrowers actually pay towards their loans each month. My research of this question revealed a disheartening lack of clarity. Shockingly, there’s no official estimate of this published by the Education Department; they’re not even required to disclose this! So much for government transparency.

What we know is there are 46 million Federal student loan borrowers. There’s scattershot disclosures by the government regarding how many borrowers are on different kinds of repayment plans.

Our best guess digging through the data is that the cost will be over $10 billion a month.

Many economists worry that the resumption of student loan repayment will prove too costly for many people. It certainly will in some cases. $10 billion isn’t a huge amount in a $27 trillion economy. But coupled with rising interest rates and softening job markets, it’s yet another headwind for the consumer to deal with.

Conclusion: The Federal Student Loan System is Broken

If all the changes and proposals you just read are making your head spin, you’re not alone. The federal student loan system is completely broken. It’s confusing for borrowers, whose “fate” continually hangs in the balance with politicians.

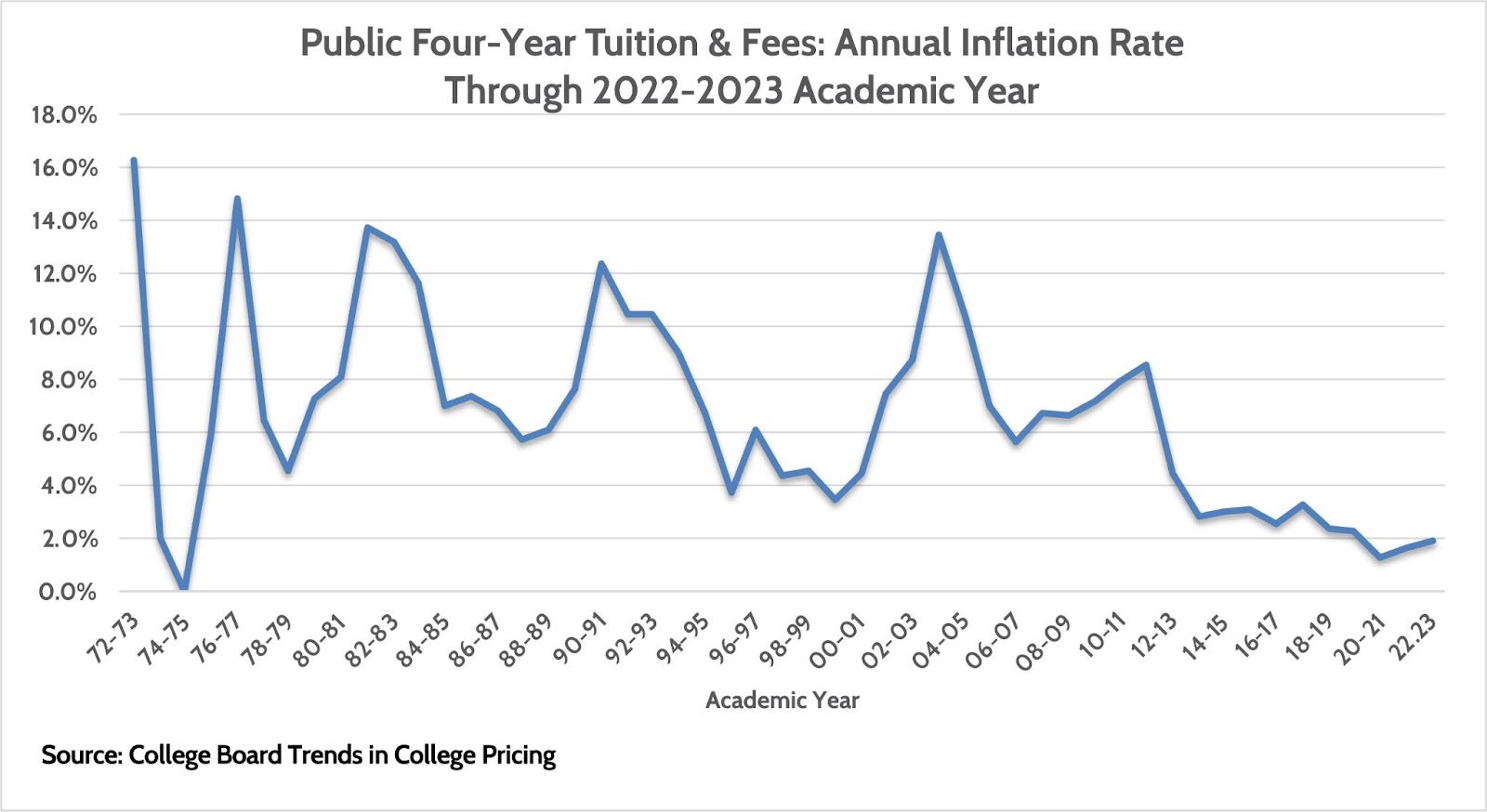

Worse, the proposed changes to make loans more “affordable” will likely dis-incentivize colleges from keeping tuition increases in-check. College has gotten very expensive in the last 30 years, to where potential students were balking at the price tag. This caused a slowdown in tuition inflation in recent years. But with the government doing everything it can to make sure borrowers DON’T have to pay loans back, it’s hard to see why colleges wouldn’t take advantage by hiking tuition rates.

The system isn’t fair to potential students, who fear huge tuition costs and stories of peers “trapped” in student loan problems. Neither is the system fair to taxpayers, who’ve watched a previously functioning student loan system transform into a $1.7 trillion obligation of the taxpayer.

We’ve helped several clients who work in public service find loan forgiveness in the last year, thanks to the relaxation of the rules. Whatever financial issue you may have, we have the expertise to help you wade through your options and pick the one that’s the best for your long-term financial health. Curious about what financial confidence could look like for you? Reach out and schedule a meeting with our team!

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

How to Find College Scholarships [Video]

In this video, we break down how to find college scholarships for athletics, academics, geography, merit, and more!

Podcast Episode 35: The College Funding Challenge

In this episode, parents and grandparents learn about college funding, reducing the cost and saving up with the updated FAFSA and 529 plans.

Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer

Rob has over 20 years of experience in the financial services industry. Prior to joining Financial Design Studio in Deer Park, he spent nearly 20 years as an investment analyst serving large institutional clients, such as pension funds and endowments. He had also started his own financial planning firm in Barrington which was eventually merged into FDS.