What are the Latest Inherited IRA rules?

by Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer / August 16, 2023

The passage of the SECURE Act in late 2019 and SECURE Act 2.0 in late 2022 upended the rules for Inherited IRAs. Gone are the days when a beneficiary could simply “stretch” Inherited IRA withdrawals over the rest of their lifetime. Now, a beneficiary has to run through a maze of new – and still incomplete – rules about how much they’re supposed to take out of an Inherited IRA and when they’re supposed to do it. In this post we answer the question that everyone is asking, “What are the Latest Inherited IRA rules?”

Who’s the Beneficiary of Your IRA?

The key to understanding Inherited IRA rules is to first understand the different types of IRA beneficiaries. Whenever you open a new IRA, you’re going to be asked to designate a primary beneficiary. For married couples, their spouse is usually the beneficiary. And often, those same married spouses will name any children they have as contingent beneficiaries. Meaning, if someone’s spouse passed away before they did, then the IRA would go to the children.

You’re not limited to whom you can name as the beneficiary of your IRA. It could be a close friend, a neighbor, or grandchildren. You can also name a charitable organization as your beneficiary. The key to understanding Inherited IRA rules is to understand what TYPE of beneficiary you are, as that guides the maze of rules.

This blog will focus on the most common types of beneficiaries shown in the yellow box above.

What is a Required Begin Date?

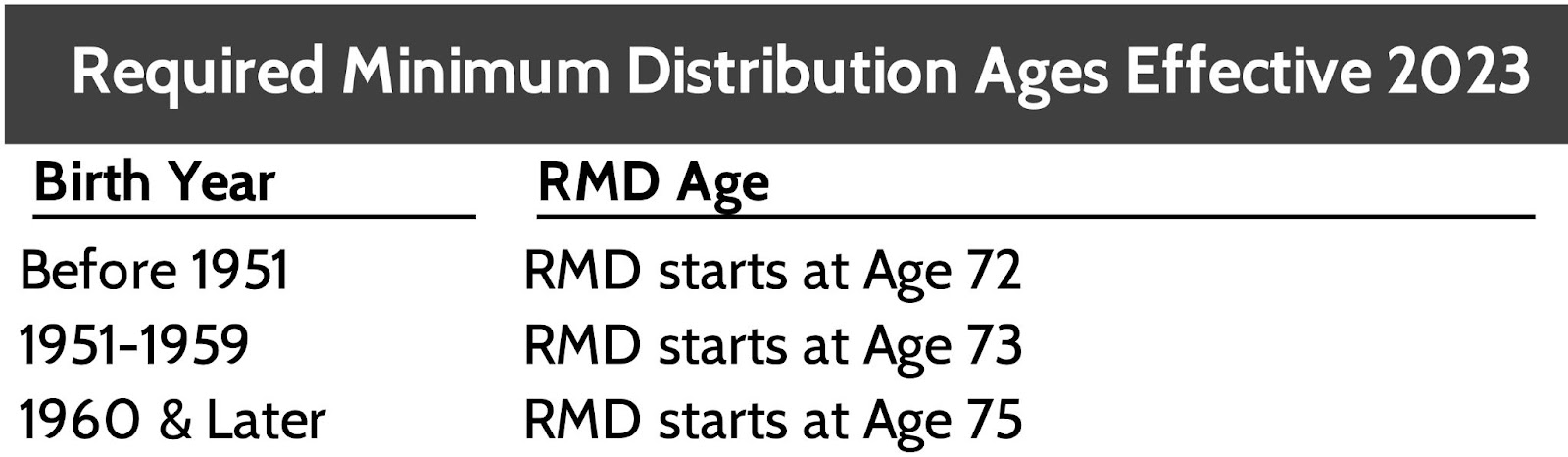

We also need to understand something important about Required Minimum Distributions: the Required Begin Date. This is the date by which someone is required to take Required Minimum Distributions (“RMDs”) from their Traditional IRAs and 401(k)s.

The Required Begin Date is April 1st of the year FOLLOWING the year in which someone reaches their RMD age. Recent law changes raised the RMD age twice, which has created confusion. We have a video explaining how these rules impact people who inherited an IRA after the January 1, 2020 and the SECURE Act 2.0.

The table below shows when RMDs start for people based on what year they were born.

For example, if someone was born in 1952, they turn Age 73 in 2025. Their required begin date would be April 1, 2026.

You’ll see why the Required Begin Date is important as we look at specific examples for Inherited IRA situations.

Scenario: You’ve Inherited an IRA from Your Spouse

The rules are pretty straightforward for spouses that inherit IRAs from their deceased spouse. Importantly, they preserved rules to make sure that spouses aren’t forced to take money out of the Inherited IRA sooner than if their spouse never passed away.

Option #1: Roll Deceased Spouse’s IRA to your own IRA. This is by far the most common scenario. Here, money in the deceased spouse’s IRA moves directly over to your own IRA with no tax consequences. From there, the surviving spouse doesn’t have to take RMDs until their own Required Begin Date.

Option #2: Leave the money in an Inherited IRA. It’s not very common to see a spouse keep money in an Inherited IRA account. If a spouse chooses this option, the rules for when money has to come out are:

- Spouse passed away BEFORE their Required Begin Date: Surviving spouse must take RMDs no later than December 31st of the year their deceased spouse would’ve reached RMD age. If the deceased spouse was young, that means the surviving spouse can delay taking RMDs for years. Once the deceased spouse would have reached RMD age, the surviving spouse calculates the RMD amount based on their remaining life expectancy or that of their deceased spouse, whichever is most beneficial.

- Spouse passed away AFTER their Required Begin Date: In the year of their spouse’s death, they calculate the RMD based on their deceased spouse’s age. After that, the surviving spouse can take RMDs based on their own age.

Planning Tip: Option 2 could be useful to surviving spouses if their spouse died prematurely and the surviving spouse needs money. The law allows the surviving spouse to take money out of an Inherited IRA without paying the 10% early withdrawal penalty, which applies before Age 59-½. If the surviving spouse rolls the IRA to their own IRA (Option 1), they will lose this benefit.

Scenario: You’re a Non-Spouse Eligible Designated Beneficiary and RMDs Weren’t Started Yet

This is where things get confusing, so let’s be clear about who this applies to:

- Minor Children

- Disabled or Chronically Ill

- Any other beneficiary 10 years or younger than the IRA owner who passed away

- The IRA owner who passed away had NOT started their Required Minimum Distributions yet

Prior to passage of the SECURE Act, beneficiaries of Inherited IRAs could “stretch” required distributions over the course of their lifetimes. This gave Inherited IRA beneficiaries a lot of flexibility for income needs and tax planning.

Fortunately, for non-spouse, eligible designated beneficiaries (try saying that 10 times straight!) the rules remain the same post-SECURE Act.

- Money gets moved into an Inherited IRA for the beneficiary

- No distribution due in the year of the original IRA owner’s death

- RMDs must begin by December 31 the year after the IRA owner’s death

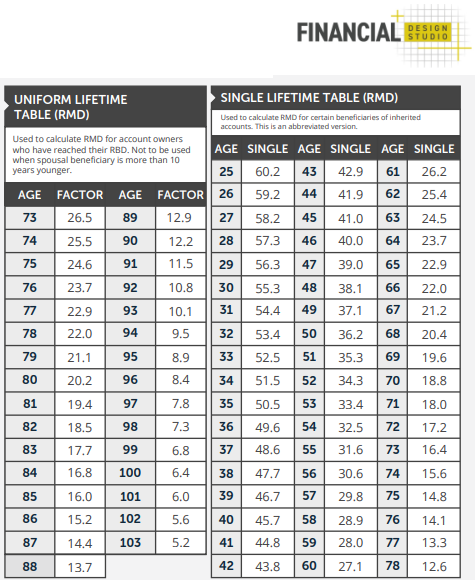

- You calculate the annual RMD using the IRS Single Life Expectancy Table, often referred to as Table 1.

Example: An IRA owner aged 70 passes away, leaving their $100,000 IRA to their brother, 62 years old (less than 10 years younger.) The IRA’s custodian opens an Inherited IRA in the brother’s name and deposits the owner’s IRA money into the Inherited IRA. In the year of the IRA owner’s death, no RMD is required.

However, next year the brother will be 63 years old and will have to take RMDs from the Inherited IRA. Based on the Single Life Expectancy table, the calculated RMD will be $100,000 / 24.5 = $4,081.63.

Scenario: You’re a Non-Spouse Eligible Designated Beneficiary and RMDs Were Already Started

Similar to the scenario above, this situation applies to:

- Minor Children

- Disabled or Chronically Ill

- Any other beneficiary 10 years or younger than the IRA owner who passed away

- The IRA owner who passed away had already started taking his or her RMD

The rules for beneficiaries in this situation are:

- Money gets moved into an Inherited IRA for the beneficiary

- They take an RMD in the year of death using the original IRA owner’s life expectancy from the IRS Uniform Life Table.

- The following year, they can calculate RMDs based on the original IRA owner’s life expectancy, or that of the beneficiary, whichever is longer.

Example: An IRA owner aged 80 passes away, leaving their $100,000 IRA to their brother, 72 years old (less than 10 years younger.) The IRA’s custodian opens an Inherited IRA in the brother’s name and deposits the owner’s IRA money into the Inherited IRA.

The IRA owner had already started taking RMDs, so this is what happens:

- Year of Death: The RMD is $4,950.50 using the original IRA owner’s age at death (80) and the IRS Uniform Life Table ($100,000 / 20.2)

- Next Year: Brother is now 73 years old and let’s assume the account was still $100,000. Based on the IRS Single Life Expectancy Table, the brother’s RMD for the Inherited IRA would be $6,097.56 ($100,000 / 16.4)

The scenarios we’ve looked at to this point applied to Eligible Designated Beneficiaries: Spouses, Non-spouses who inherited an IRA before the original owner took RMDs, and Non-spouses who inherited an IRA after the original owner started taking RMDs.

Now, we are going to look at the two scenarios that apply to Non-eligible Designated Beneficiaries: Adult children and beneficiaries over 10 years younger than the original IRA owner, such as nieces, nephews, and younger siblings.

Scenario: Non-eligible Designated Beneficiary Inherits and IRA Before RMDs Were Started

Who this applies to:

- Adult children

- Any other beneficiary over 10 years or younger than the original IRA owner

Prior to the SECURE Act, non-eligible designated beneficiaries could “stretch” RMDs on Inherited IRAs over the rest of their lives. The SECURE Act eliminated the “stretch” and instead imposed a 10-year window whereby all Inherited IRA assets have to be distributed. This is often referred to as the “10-year Rule.”

If the original IRA owner had not yet started taking RMDs, a non-eligible designated beneficiary inheriting an IRA will have to fully distribute the IRA’s proceeds within 10 years. Importantly, no RMDs are necessary because the original IRA owner had not yet started their own RMDs!

Example: A 60-year-old IRA owner passes away and leaves the IRA to their daughter, who’s 30 years younger. Since the IRA owner had not yet reached their Required Begin Date, they weren’t required to take RMDs.

The IRA owner’s custodian will transfer the IRA into an Inherited IRA in the daughter’s name. She now has to fully distribute the IRA’s proceeds within 10 years.

While no RMD is required by the daughter, she’s free to take money out of the Inherited IRA as she sees fit, as long as it’s all distributed by Year 10. Like all IRA distributions, they will tax the money she takes out of the Inherited IRA at ordinary income tax rates.

Planning Tip: For high-income earners that inherit IRAs, it’s important to get good tax planning advice for how best to distribute Inherited IRA assets. Otherwise, you might find yourself in a higher tax bracket than you expected.

Scenario: Non-eligible Designated Beneficiary Inherits and IRA After RMDs Were Started

Who this applies to:

- Adult children

- Any other beneficiary more than 10 years younger than the original IRA owner

This scenario is the one causing much confusion with financial planners and Inherited IRA owners. I won’t bore you with all the confusing IRS language, but it’s important to know what’s going on.

When Congress passed the SECURE Act in late 2019, everyone’s interpretation of the new “10-year rule” was that yes, they’d have to take all money out of an Inherited IRA within 10 years. But no, they wouldn’t be required to take RMDs. However, in February 2022, the IRS released a surprising proposed regulation that said they would require RMDs for these types of beneficiaries if the original IRA owner had already started RMDs.

This threw the tax and financial planning community for a loop, with everyone scrambling to figure out whether they should advise clients in this situation to take RMDs. Remember, this is a proposed regulation, not a final ruling. So there’s still a question whether it will be a final ruling or not.

Instead of resolving the issue once and for all, the IRS has exempted these beneficiaries from having to take RMDs from Inherited IRAs for the 2021, 2022, and most recently, the 2023 tax year.

How Non-Eligible Designated Beneficiaries Inherited IRAs

As it stands today, if you inherited an IRA as a non-eligible designated beneficiary in 2020 or later, you do NOT have to take RMDs. However, the 10-year rule still applies, meaning you have to fully distribute all Inherited IRA assets within 10 years of the original IRA owner’s death.

Example: An 80-year-old IRA owner passes away and leaves the IRA to their daughter, who’s 30 years younger. The IRA owner had been taking RMDs as required for several years.

The daughter is required to withdraw all Inherited IRA assets within 10 years. However:

- For 2021, 2022, and 2023 they require NO RMDs

- For 2024 and beyond, there’s risk that RMDs will be required unless the IRS grants another waiver

As financial advisors, it’s our job to monitor these situations and advise clients about the best course of action as the rules change. The Inherited IRA rules are a prime example of that!

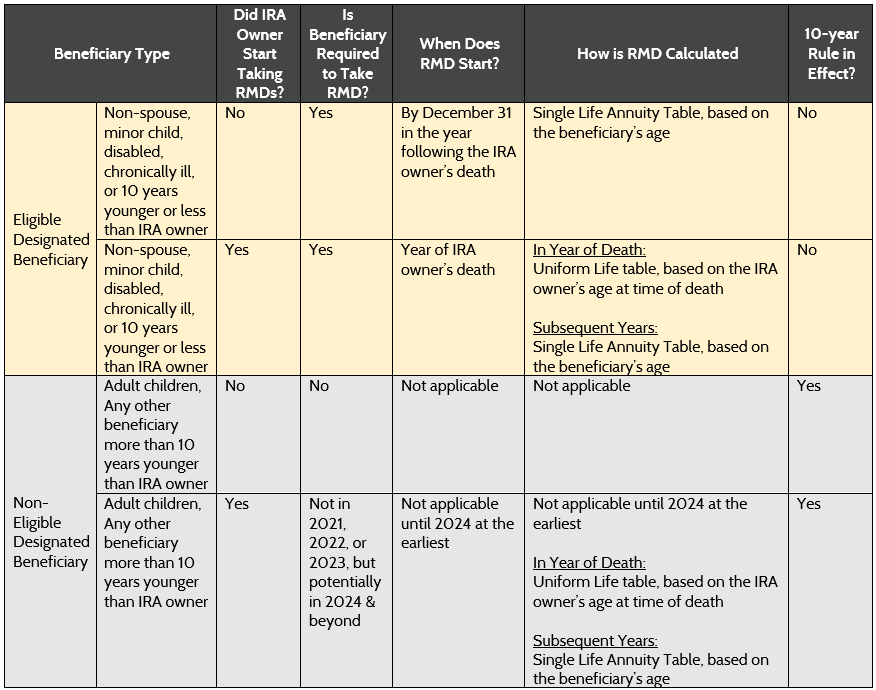

Summarizing Inherited IRA Rules

The tables below summarize the Inherited IRA rules depending on what type of beneficiary you are.

The Latest Inherited IRA Rules are Complicated!

This is one of those financial planning topics that even gives Certified Financial Planners headaches. Not only are the rules unnecessarily complicated, but they’re not even completed.

Our Near Retiree clients are grappling with Inherited IRA rules more and more as older parents pass on. This can complicate the client’s financial planning, especially if they’re still working. This makes tax planning even more important, which we do in house at FDS.

The Inherited IRA rules are a great example of what we’ve been seeing in recent years. Laws regarding retirement rules are changing frequently. These rule changes often create important shifts in retirement planning strategies.

We help clients cut through all the confusion, continually optimizing financial plans for the latest rules. Our goal is that you fully understand every aspect of your financial plan and how law changes affect you. We find that clients who are empowered with information feel more confident about their future. And that’s what we want: confident clients!

Bonus: Our Free Retirement Planning Guide

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

Should I Retire Early? The Pros, Cons, and Hidden Costs [Video]

In this video, we explore the financial pros and costs, as well as the hidden costs we see as financial advisors when clients retire early.

How to Use My Severance Package for Retirement [Video]

In this video we cover what to expect in a package, the option to negotiate, and how you can use your severance package for retirement.

Rob Stoll, CFP®, CFA, Financial Advisor & Chief Investment Officer

Rob has over 20 years of experience in the financial services industry. Prior to joining Financial Design Studio in Deer Park, he spent nearly 20 years as an investment analyst serving large institutional clients, such as pension funds and endowments. He had also started his own financial planning firm in Barrington which was eventually merged into FDS.