Should I Change My Investments Before Retirement?

by Financial Design Studio, Inc. / October 16, 2025

Executives planning to retire within 10 years should start thinking about de-risking their retirement investments. From the early days of one’s career until 10 years before retirement the most popular recommendation is to invest mainly in stocks to generate long-term growth. But retirement marks when you’ll shift from saving for retirement to relying on those same savings to meet cash flow needs. That major shift requires a rethinking of how you’re invested. Several factors help in determining how to invest as you get close to retirement. Read below to discover what these factors are and how important each one is as we answer the question, “Should I change my investments before retirement?”

How Retirement Investing Changes at Different Ages

We may not realize it, but many of us will spend most of our lives saving and investing for retirement. It starts as early as our 20s. If we’ve saved well, we’ll have some savings to pass on to our loved ones after we’re gone. So it’s good to understand how to invest those savings throughout your life!

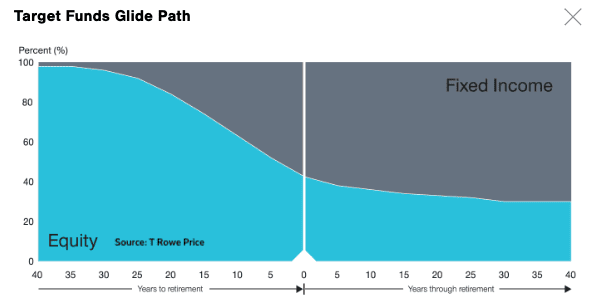

The simple way to think about investing retirement savings is to invest aggressively in stocks in the early and middle years of your career. But as you get close to retirement, investing more conservatively. By “invest conservatively” we mean reducing exposure to stocks and increasing the proportion of less volatile bonds in your portfolio. Stocks provide growth in early years, while bonds provide stability in later years. The investment industry has come up with a product called Target Date Funds that automatically changes your investments as you get older. The graphic below from T Rowe Price shows the typical allocation between stocks and bonds in the years before and after retirement.

Target date funds invest most savings in stocks in the early years of working, to generate growth. Starting 10-15 years before retirement, they steadily reduce exposure to stocks while increasing allocations to bonds. Once the investor is retired, target date funds invest over 50% of the investor’s savings in bonds.

While the target date fund “glide path” is a useful starting point to understand how to invest for retirement, it’s just a “cookie cutter” approach. Your circumstances may warrant a much different investment strategy than what a target date fund would suggest.

Major Factors that Affect Retirement Investment Strategies

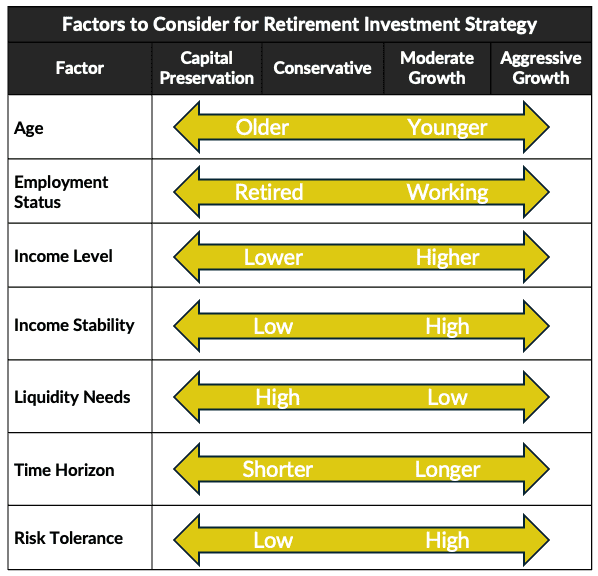

When we meet with clients, there are some demographic factors we initially look at when we consider making an investment recommendation. Most of the factors are objective. Based on the answers to those factors, we can find a good starting point for how a client should invest for retirement.

Here is how each of the factors listed above can influence how you invest for retirement:

- Age: The younger you are, the more time you have to stay in stocks. You can persevere through the ups and downs of stock market cycles. Once you’re older, you’re more susceptible to having a bear market in stocks hurt your plan.

- Employment Status: When you’re working and still saving for retirement, you have time to make up for any down markets. If you retire, you don’t have that luxury.

- Income Level: Higher income households can tolerate more investment risk as they have more dollars to save.

- Income Stability: An executive with job security and predictable salary and bonus levels likely has more capacity to invest aggressively. Workers with less stable income (e.g. real estate agents) may not be comfortable with too much investment risk given the volatility of their income.

- Liquidity Needs: If you’re actively using retirement savings in retirement, your primary concern is that the money will be there when you need it. This would naturally lead to investing conservatively.

- Time Horizon: Savers with long time horizons have time to make up the ups and downs of the stock market. But that doesn’t mean the saver is young. Even someone at Age 65 may have a long investment time horizon.

- Risk Tolerance: This is the intangible reaction of how an investor responds to market volatility. An investor with a low tolerance for risk may be susceptible to selling stocks when they’re down, which we normally don’t recommend.

These factors are a good place to start. But a detailed retirement financial plan helps hone in on your retirement investment strategy. Much of how you should invest in retirement depends on your unique circumstances. What are your expected income sources in retirement? Social Security? Pensions? How much of your yearly cash flow needs will these income sources cover? How much of your portfolio are you expected to need each year?

This is the heart of what we do at Financial Design Studio. Client-specific factors can sometimes lead to investment recommendations different from how someone might “score” on the factors above. For our ongoing financial planning clients, we run annual projections of income sources and cash flow needs. As we do this year-by-year, we can hone in on the most appropriate investment strategy for retirement. Want this kind of confidence for your retirement? Schedule a retirement review with our team! Otherwise, keep reading to see some examples of what we look at.

How Do Social Security and Pensions Affect Retirement Investments?

Future Social Security and pension income can significantly influence a retirement investment strategy. I think the constant media headlines about Social Security’s shaky state have led many people to write it off as a future income source. But there are good reasons not to write Social Security off. In fact, you may be surprised at what percentage of your future cash flow needs will eventually be covered by Social Security.

When we refer to “cash flow needs” we refer to the annual amount of money you need. This should cover all your living expenses, mortgage payments, vacations, and everything else. This is real money that has to come from somewhere, whether it’s Social Security, cash savings, or your retirement accounts.

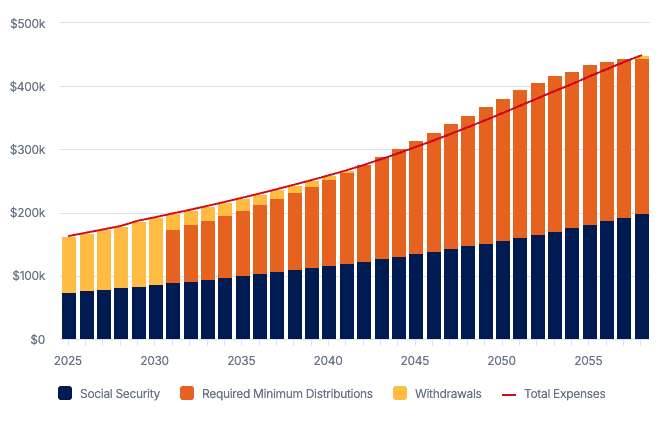

Here is a common example: Married couple, both with long careers as executives. Their goal is to spend $150,000 a year in retirement, with 3% inflation each year. They each have $37,500 in Social Security benefits, and they have $2,000,000 in combined retirement savings. Using this information, we can create long-term projections of their cash flow needs and where that money will come from.

In the first few years of retirement, we see this couple will get about 50% of their cash flow needs from Social Security income (dark blue bars) while supplementing the rest of their cash flow needs with withdrawals from their IRAs (yellow bars). Starting in 2031, they reach the age where they begin Required Minimum Distributions (“RMDs”) from their IRAs (dark orange bars). But all along, we can see that while their cash flow needs increase each year with inflation, so does their Social Security income.

A client that has a high percentage of their annual cash flow needs covered by Social Security and pensions can likely tolerate more investment risk. Meaning, instead of investing in a “typical” retirement portfolio of 60% Stocks and 40% Bonds, maybe they can invest 70% in Stocks and 30% in Bonds. This also works the other way for those whose Social Security covers a low percentage of their cash flow needs; they would want to invest conservatively.

How Portfolio Withdrawal Rate Affects Retirement Investment Strategy

In the example above, we see that Social Security covers half of the couple’s expense needs. That’s an important piece to help determine their retirement investment strategy. But we can’t stop there without considering the other side of their cash flow needs: what percentage of their portfolio they’re going to withdraw each year to cover the other half of expenses that Social Security doesn’t cover. In the financial planning world, we call this the portfolio’s “withdrawal rate.”

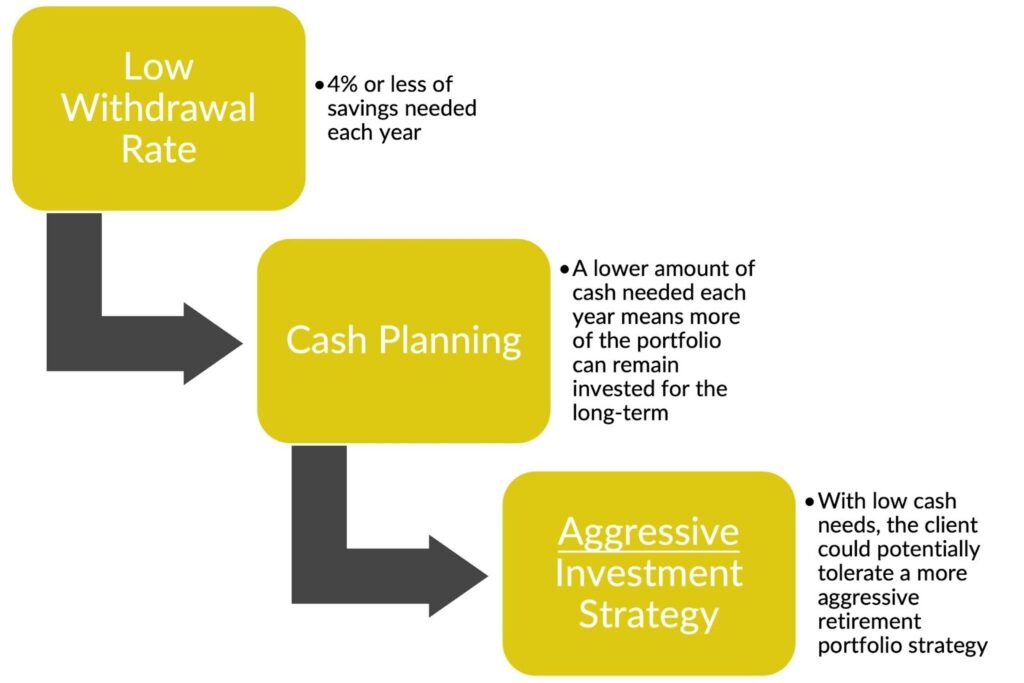

You may have come across a retirement planning concept called the 4% Rule. The rule states that if you withdraw 4% of your portfolio or less each year, you should have enough retirement savings to last for the rest of your life. While this rule is a good starting point, like most financial “rules of thumb,” there are a lot of caveats that don’t make it foolproof.

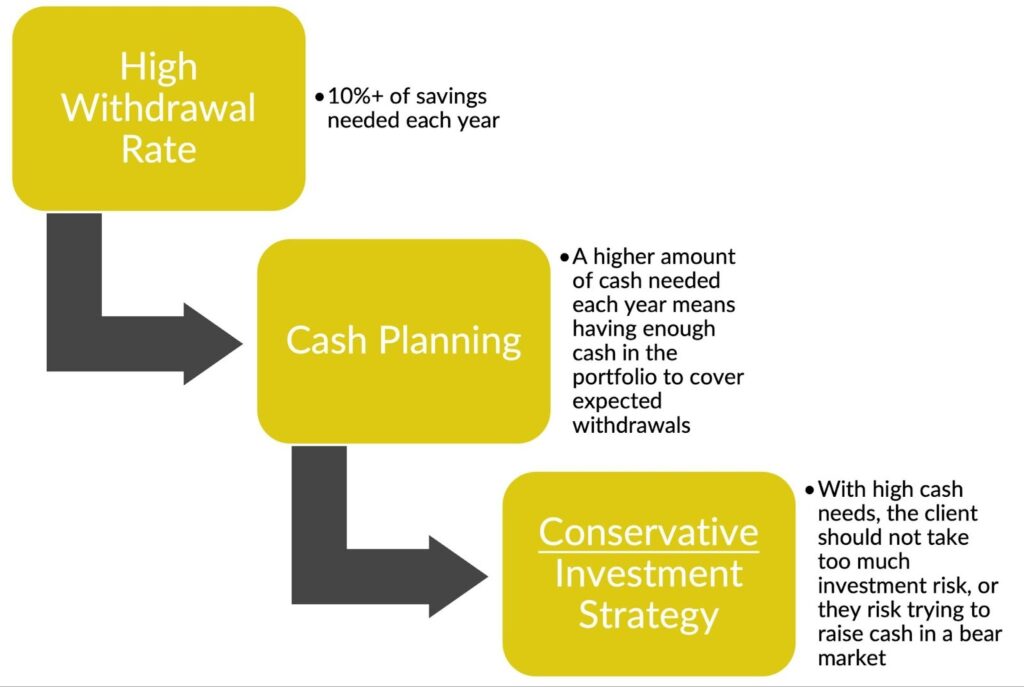

Still, looking at a client’s projected portfolio withdrawal rates in retirement can provide valuable information about how aggressively (or not) to invest. Here is how high and low portfolio withdrawal rates may inform how a client could invest.

Portfolio “withdrawal rate” refers to real cash that has to be taken out of a retiree’s portfolio. The problem is that the stock market is volatile. Over the last 100 years, the S&P 500 index has generated negative annual returns 25% of the time. Imagine needing to withdraw a large amount of cash from an aggressively invested portfolio. But stocks just declined by 20%. They would have to sell stocks at the “bottom” to raise that cash.

That would not be a problem for a retiree who only needs 2% of their portfolio to cover cash flow needs. In theory, they have more capacity to take investment risk by investing more aggressively.

Should I Change My Investments Before Retirement?

The best time to think about changing investments is about 10 years before retirement. Those are the transition years between peak saving years and a more conservative investment strategy for retirement.

We have seen how demographic factors – age, income levels, liquidity needs – can be a good first step towards possibly changing investments. The problem is that they don’t consider your specific circumstances that may allow for “exceptions” from basic rules of thumb.

The best way to determine an investment strategy as you head into retirement is to get a full retirement plan with projections of future income and cash flow needs. Financial Design Studio provides clients with these kinds of detailed projections. It’s this clarity that can help answer a lot of questions about how to invest for the future.

Your Next Steps for Your Retirement Portfolio

We always remind clients that when we provide retirement projections, they’re good for today. But we know that life changes and sometimes there are significant, unexpected things that can happen, such as death or disability.

Ongoing clients that we work with year-to-year are not immune from life’s uncertainties. But as those things happen, we are reacting quickly. For example, clients that are forced to reckon with an unexpected death of a spouse, can focus on grieving the loss of their life partner. We are handling major financial issues in the background.

Key benefits of getting retirement projections from a financial advisor:

- Getting organized: Knowing how well you are prepared for retirement before you retire.

- Identifying Goals: Answering the important question of, “What do we want to do in retirement?” Travel? Fund educational accounts for grandkids?

- Understanding income sources: What will your Social Security be? Is it best to take Social Security early or wait until Age 70?

- Cash flow planning: If we plan to spend $X per year in retirement, where will that money come from? How often do we want to have money transferred to our bank account?

- Saving on taxes: What is the best portfolio withdrawal strategy to minimize taxes? Can Roth Conversions help save us taxes?

- Investment strategy: Knowing all the above, what’s the best way to invest our retirement savings? Aggressive? Conservative?

Remember, “How should I be investing?” is just one of the major questions to ask as you head into retirement. Financial Design Studio helps you answer all the questions you have. But we also answer all the questions you didn’t know you had! Schedule a free 30 minute retirement review with our team by clicking “get started“!

Bonus: Retirement Planning Guide!

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

Should I Retire Early? The Pros, Cons, and Hidden Costs [Video]

In this video, we explore the financial pros and costs, as well as the hidden costs we see as financial advisors when clients retire early.

Financial Design Studio, Inc.

We are financial advisors in Deer Park and Barrington, IL. A team with a passion for helping others design a path to financial success — whatever success means for you. Each of our unique insights fit together to create broad expertise, complete roadmaps, and creative solutions. We have seen the power of having a financial plan, and adjusting that plan to life. The result? Freedom from worrying about the future so you can enjoy today.