Are AI Stocks In A Bubble?

by Financial Design Studio, Inc. / December 5, 2025

Two years ago, OpenAI launched ChatGPT, ushering in the age of artificial intelligence (“AI”.) Since then, the technology companies that supply the build-out of AI infrastructure have seen their stocks surge, carrying major stock indexes higher. However, investors are asking questions about the sustainability of the AI build-out and whether leading tech stocks – sometimes referred to as the ‘Magnificent 7’ (“Mag7”) – can continue to lead the market. We normally don’t like to opine on how markets will perform as we are long-term investors. But the financial news media is writing more “Are AI Stocks in a Bubble?” articles, so we wanted to share our perspective on where we are in the AI cycle.

Nvidia’s Historic Rise

No company captures the excitement of AI more than Nvidia. The company has been around a long time. For some of my fellow Gen X’ers out there, Nvidia’s graphics cards powered our gaming PCs back in the 1990s. Over time, Nvidia also developed chips that are particularly suited for processing the Large Language Models (“LLMs”) that AI companies are developing. In fact, Nvidia’s chips are essentially the only game in town for anyone who wants to run AI.

Investors have rewarded Nvidia stock, rising over 1,000% in the last three years. At its current market value of $4.5 trillion, Nvidia is worth more than every stock market in the world outside of the United States, China, and Japan. All the stocks traded in the United Kingdom are worth a combined, $3.1 trillion, for example.

Strong fundamentals have backed Nvidia’s rally, as revenues have increased 5-fold since 2022 while net profit has increased 7-fold. Put another way, the stock has rightly responded to exceptionally strong fundamentals.

Despite this, the value of Nvidia has gotten so high that it invites comparisons that call into the question the sanity of its value. For example, this chart by Crescat Capital shows that the value of Nvidia is 3x higher than that of the entire energy sector in the United States, despite that fact that total energy cash flows are 20% higher than Nvidia.

This doesn’t mean the energy sector is undervalued; it’s a slow-growth sector compared to the torrid growth prospects of Nvidia. But anecdotes like this become more common in bubbles. The most famous example we can remember was at the height of Japan’s stock market bubble in the late 1980s, when the value of the land under Tokyo’s Imperial Palace was (for a brief time) worth more than all the real estate in California!

AI Data Centers are Energy and Water-Intensive

AI companies need large data centers to power their language models. As AI companies compete to be a first mover in the AI race, they are building data centers as quickly as they can. For example, Amazon built an $11 billion data center – called Project Rainier – deploying more than one million AI chips on 1,200 acres in Indiana.

However, there has been increasing pushback from residents who live near a proposed data center. Their concerns are two-fold: 1) they worry that the energy needs of the data center will drive up residential electricity prices, and 2) they’re concerned about the impact of the data center’s water usage.

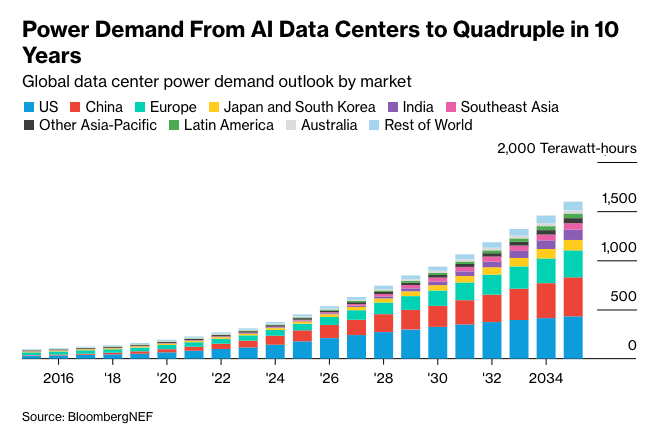

Using Amazon’s Project Rainier as an example, people expect it to consume 2.2 million gigawatts of electricity a year. That is enough electricity to power 1.6 million residential homes each year. And based on our (extremely) rough estimate, their data center will need 760 million gallons of cooling water per year, which is the same usage as 7,000 homes.

The chart above from Bloomberg News shows the scale of energy needs to power AI data centers. Currently, these data centers consume about 4% of the electricity generated in the U.S. Analysts project that number to grow to 12% of total consumption by 2030. Simple supply/demand economics points to higher electricity prices for everyone if utilities don’t increase electric generating capacity significantly. The problem is that it’s really hard to build new power plants in the U.S. Nuclear power is the most obvious solution to AI’s energy needs, but there have only been two nuclear plants built in the United States since the Three Mile Island disaster in 1979. Do we really expect citizens to wave new nuclear plants into their backyards?

Artificial Intelligence is Capital Intensive

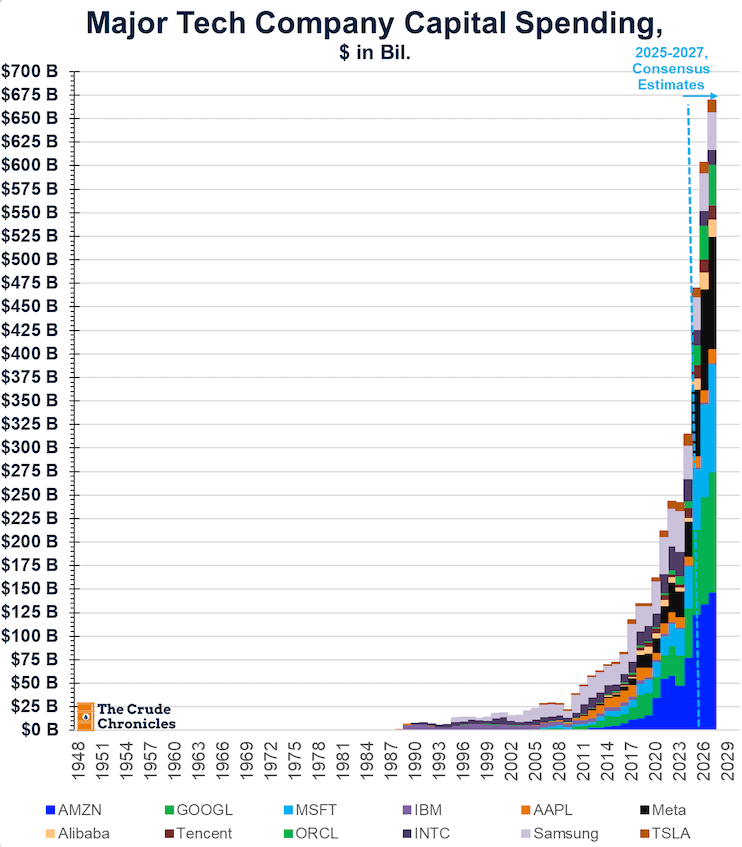

Besides the water and electricity needed to run AI data centers, building them is very expensive. The Mag7 technology companies that are at the forefront of the AI capital spending boom are plowing enormous amounts of money into building out data centers and other AI technologies. As this tally from Substack publisher The Crude Chronicles shows, close to $500 billion dollars will be spent in 2025 on the AI build-out. And that will grow further with another $2.5 trillion of spending from 2026 to 2028.

Up to recently, large tech companies could fund these capital expenditures out of the cash flows generated by their core businesses. Funding capital expenditures out of cash flow is a “safe” way for companies to invest for growth. That, however, is changing.

Capital expenditure growth is so fast that it is now out-stripping the ability of tech companies to generate cash flows to pay for the build-out. Instead, these companies are turning to bond markets to raise extra capital. In just the last six weeks, these companies have raised $88 billion of debt, which is a significantly higher amount of debt than these same companies have raised in recent years.

Why does it matter that debt is increasingly the funding source for capital expenditures instead of internally generated cash flows? It boils down to the nature of debt investors relative to equity (stock) investors. Equity investors are fine with companies plowing cash flow into capital expenditures if there’s hope that it will generate future growth, regardless of when that growth may come. Debt investors, however, are much more demanding to see future growth because that is the money the company will need to repay the loan. In short, there’s a lot less “hope” with debt investors than equity investors.

Stock Market Impact of AI Capital Spending Binge

We’ve seen that the build-out of AI requires a lot of capital spending, energy, water, and increasingly, debt. Does this matter for the stocks in AI companies? Before tackling that question, I should point out that I’m not an AI “doomer.” The technology is real and I use it myself to do everything from doing research for this article to figuring out how to plant grass at home. The roadside is littered with investors who are permanently bearish on stocks; “permabears,” we call them. I’m not one of those!

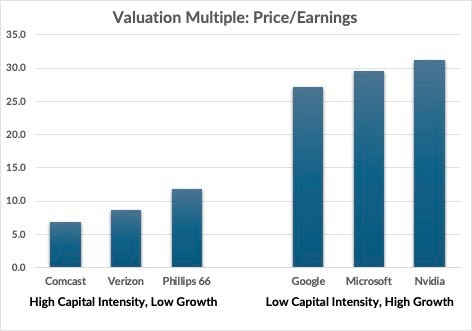

Over the last 15 years or so, technology companies have commanded a greater share of investor attention and higher valuations. The basic argument (which I’ve agreed with) is that these companies are “capital-lite” growth companies that deserve higher valuations. “Capital-lite” means they don’t need to invest a lot of money to grow, hence investors can pay more for the growth they generate.

Compare that to old economy industries like oil & gas or telecom companies, which need to invest a lot of money to build and maintain property, plant & equipment but they grow little. Capital intensive businesses that don’t grow get low valuation multiples.

The most popular valuation measure in finance is to compare the value of a company relative to how much it earns. We call this the “price/earnings ratio,” which takes the price of the stock divided by its expected earnings per share. The chart below compares three “old economy” stock valuations to three popular technology companies. It shows how investors favor high-growth companies with low capital intensity.

To this point, technology stock investors have ignored the surging capital expenditure needs of AI. The thinking is that future AI revenue growth will be massive, and hey, “they’re funding it out of their cash flows.”

But this is changing. The sheer size of capital expenditures, plus the fact it is being funded from debt issuance, points to a lot more capital intensity for these “capital-lite” companies. In our opinion, AI revenues will have to come soon and in size to stave off a compression in tech company valuations.

Lessons from Historical Capital Spending Binges

The last point to make on the AI boom is how it relates to previous booms in capital spending. Just in the last 30 years, we’ve seen two industries experience a surge in capital spending, only to be followed by a bust.

The technology sector of the late 1990s was capital intensive. As the internet was rolled out, there was an insatiable need for fiber optic cable, data switches, and capacity expansions by cable and phone companies. Cable and phone companies tripled their capital spending from 1996 to 2000. Eventually, the gap between capital spending and the expected revenue payoff of new technologies proved too long, and many companies suffered.

A similar event happened in the late 2000s through 2015. Oil & gas companies discovered new ways to extract oil & gas through “fracking.” The Shale Revolution ultimately led to a massive increase in capital spending, peaking at $660 billion in the early 2010s. Eventually, so much oil & gas was being produced that it caused prices to collapse, wiping out many players.

Is the AI spending boom setting up for the same bust? I don’t know. But there’s no doubt we are in an historic capital spending binge. Further, this spending looks increasingly circular in nature. Meaning, one company’s investment in AI infrastructure depends on their customers doing the same.

Portfolio Response to AI Spending Boom

I will fully admit the size and speed of the rally in AI tech stocks has been more than I had expected. While we have exposure to a growth fund that’s geared towards large technology stocks, the weight to that part of the market in the portfolio is less than what you’d find in the benchmark S&P 500 index.

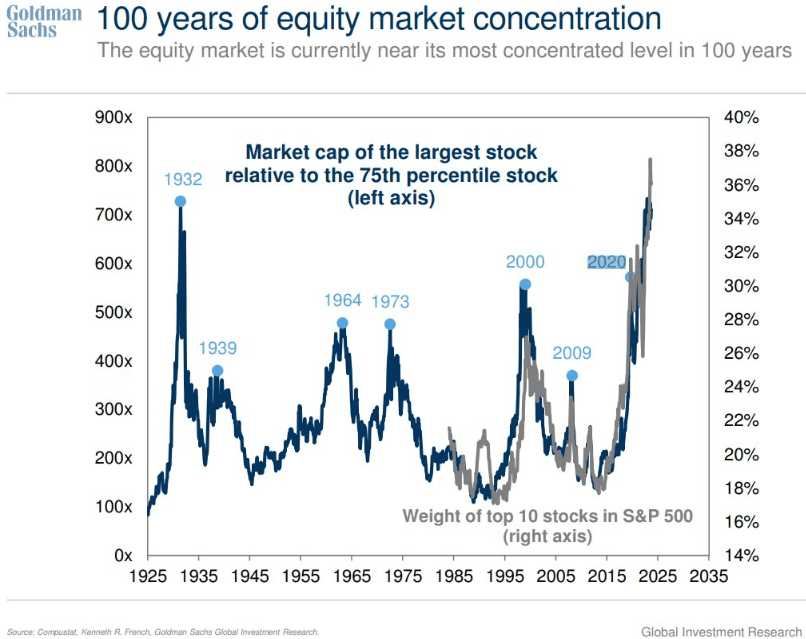

The concentration of the S&P 500 index is a genuine issue, with nearly 40% of the index of 500 stocks concentrated in just the top 10 most valuable companies. Meaning, if you put $100 in an S&P 500 index fund, you get $40 of the top 10 stocks, and $60 in the other 490 stocks.

How does this level of concentration compare to history? Goldman Sachs compiled a nice chart looking at market concentration going back 100 years. Other than the 1930s, the market has never been this heavily tilted towards the top 10 stocks.

What draws my attention is this chart is the historical peaks. The year 2000 marked the top of the tech bubble, followed by a lost decade of returns where the S&P 500 generated cumulative returns of 0% for the following 10 years. 1973 marked the peak of the Nifty Fifty bull market, followed by a lost decade of returns. 1964 was a “false signal,” as that didn’t mark a top in the market, but the 1930s was a much different story.

To control for this index concentration, we have built a portfolio of large cap U.S. stocks that replicates the S&P 500 index but with significantly less concentration in the top 10 names. Instead of accounting for 40% of client exposure in large-cap stocks, our portfolio has about 23% in those same names, which is in line with historical levels of concentration.

To be clear, being underweight the top 10 Mag7 has hurt performance the last 2+ years. But in our view, the current level of market concentration presents too much potential downside risk. With the structure we have in place, upside growth won’t keep up with the S&P 500 index, but we’d expect client portfolios to outperform the index if there’s a correction in the market. We aim to generate the long-term returns built into client financial plans with as little volatility as can be expected from investing in volatile investments.

Are AI Stocks in a Bubble?

Based on the spike in capital spending, increasing levels of debt issuance to fund this spending, and the valuations of AI stocks, we’d say there is an elevated risk of correction in these stocks. But that doesn’t mean stocks have to go down a lot. Several highly valued stocks from the late 1990s kept their stock prices relatively stable post-bubble, but it took a decade for their earnings to catch up to the stock price, leading to near-0% stock returns for years.

We also remind clients that their portfolios are well-diversified, with exposures to several types of stocks and bonds. A properly constructed, diversified portfolio will always have parts of the portfolio doing well and other parts lagging. That’s by design, because history shows that as one part of the market loses favor, another part of the market that was out of favor gains investor attention. We need look no further than international stocks, which haven’t been good performers in recent years but are +25% or more in 2025.

Investing portfolios is a very important part of the implementation phase of your financial plans. Advisors can do great work on financial projections, but if the investment strategy gets fouled up, clients can’t rely on the projections, which hurts confidence. Our #1 job is to help you, the client, feel confident about your financial projections so you can go about living the life you want. Markets will do what they will do, but we can at least “control the controllables” as best we can.

If you don’t have confidence like this for your retirement, and you know you want a team to support you, click “get started” to schedule a free consultation with our team!

Bonus: Retirement Planning Guide!

Ready to take the next step?

Schedule a quick call with our financial advisors.

Recommended Reading

Should I Retire Early? The Pros, Cons, and Hidden Costs [Video]

In this video, we explore the financial pros and costs, as well as the hidden costs we see as financial advisors when clients retire early.

Financial Design Studio, Inc.

We are financial advisors in Deer Park and Barrington, IL. A team with a passion for helping others design a path to financial success — whatever success means for you. Each of our unique insights fit together to create broad expertise, complete roadmaps, and creative solutions. We have seen the power of having a financial plan, and adjusting that plan to life. The result? Freedom from worrying about the future so you can enjoy today.